Some Cheap Canadian Stocks (Part II)

As the second part of my post about Canadian stocks I have been adding to recently I want to discuss 3 oil related businesses, Entrec Corporation (ENT.v), Palliser Oil and Gas (PXL.v) and Tesla Exploration (TXL.to)

Entrec Corp (ENT.v)

Another company of which I took a position in the last week is Entrec. Entrec provides oversized hauling, crane services and rigging services in Northern Alberta and the British Columbia. The company was a part of Flint Services until April 2011 when they sold the business to EIS Capital. At the same time EIS acquired a whole bunch of oilfield and transportation services companies (see the 2011 news releases for the past list) amalgamated the companies with Entrec and renamed the consolidated entity to Entrec.

Entrec has been on an acquisition spree since that time. It looks like they’ve acquired 10 different companies, most of which are small, trucking and hauling entities. According to Canaccord (a report which I googled and is available here ) Entrec’s acquisitions between July 2011 and the end of December have averaged 3.44x EBITDA. The latest, GT Crane and Transportation Services, was acquired for 3.5x EBITDA.

Entrec is only a little bit more expensive than its acquisitions. After acquiring GT Crane, the enterprise value is around $300 million. The company generated $26 million of EBITDA in the first half of the year and GT Crane had EBITDA of $14 million in the trailing twelve months. Extrapolating those numbers gives EBITDA of about $66 million, and a multiple of about 4.5x.

While the companies capital expenditures are expected to be significant ($53 million for 2013) most of that is growth expenditures. Entrec estimated maintenance expenditures at $7 million for the year. That means that free cash flow generation is over $40 million. On a per share basis that means at the current share price the company trades at around 4x free cash flow.

The thesis for the idea, beyond just being cheap, is that Entrec stands to benefit from LNG and oil sands development in Northern Alberta and British Columbia. Some of the impetus for putting together the acquisitions that they have has been to achieve a critical size able to bid and win some of the larger contracts. I think we’ll continue to see growth in the oil sands and from LNG projects shipping gas to Asia. Entrec should be able to participate in that growth.

Palliser Oil and Gas (PXL.v)

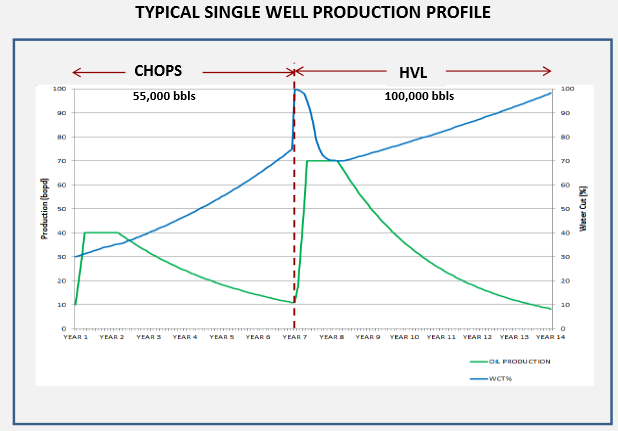

These guys are kind of like the vultures of the oil business. The company has land in three areas around Lloydminster (Edam, Manitou Lake and Lloydminster itself). They produce oil from a number of fairly shallow (400-700m) formations. The oil they produce is heavy (11-15 degree API) and the wells are generally low productivity.

What’s made the company successful has been their operational technique. They produce their wells on cold flow for the first 6-7 years (called cold flow heavy oil production with sand, or CHOPS). At that point the water cut on the well usually spikes catastrophically, making further production uneconomic. Typically the well would be shut-in. What Palliser has been doing has been adding infrastructure for increased water disposal and (presumably) opening the choke to allow for higher flow rates (called high volume lift, or HVL). This seems to be working; at the higher rates the water cut is reduced (albeit still high) and the oil rate increased to an economic level. They’ve been producing oil this way for 4 years now, so while there was a lot of skepticism in the industry about the techniques, they are mostly proven out now. See the decline curve below:

Palliser produced 2,700 boe/d in the second quarter. They generated cash flow from operations of $6 million. The company has about 62 million shares outstanding and $39 million in debt, which puts the enterprise value at a little over $75 million. It’s a similar multiple to a stock I discussed previously, Rock Energy, at 3x EV/EBITDA. They don’t have a huge land position (35,000 acres) but with heavy oil spacing at 40 acres, there is room for a lot more wells on that land than would be the case for a conventional producer.

As a heavy oil producer, Palliser is susceptible to swings in the price of heavy oil due to pipeline constraints. But the company seems to have managed this fairly well; they noted in their second quarter that they currently ship 45% of their oil by rail to the southern US, and expect that number to break 50% by year end. At a recent conference they said that if heavy oil differentials widened materially they could increase their shipments by rail substantially.

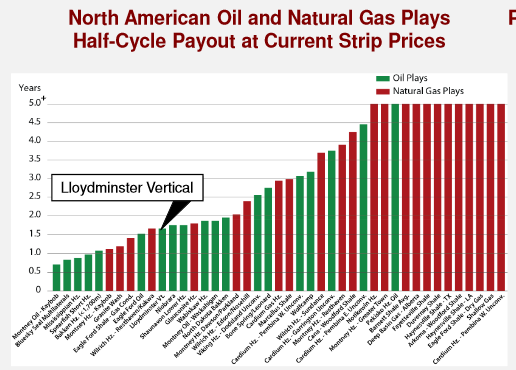

Its not a flashy story. But the half cycle payouts on Palliser’s wells are more than decent (see table below), the company has enough undeveloped acreage to continue its growth trajectory, and its selling at a significant discount to other oil juniors. I think its worth a position at these levels.

Tesla Exploration (TXL.to)

This is probably the cheapest, most illiquid stock that I own. I’m burying it at the end of this post because I’m a little sheepish talking about a stock with as little liquidity as it has. Nevertheless, I added to my position a couple of weeks ago and its now a reasonable (2%) size, and since I’m here to talk about the stocks I own I should discuss it.

Tesla shoots seismic data for customers on a contract basis. This isn’t the same business as a company like Pulse Seismic, who owns a library of seismic data that from which it sells access right to customers. Tesla doesn’t own any of the data; it shoots seismic on a contract basis on behalf of its customers.

To be honest, its such a strange little company. Tesla has a market capitalization of about $60 million (given that it’s about a 10% gap between the bid and ask most days this should be considered approximate), they have about $5 million of debt, and about $23 million in operating leases. The capital expenditures also include operating lease payments, so I believe that if you are going to count them there, the lease amounts outstanding should be left out of the enterprise value, which would mean the EV is around $65 million.

Tesla generated EBITDA in the first half of the year of $21.2 million. The company’s capital expenditures (including the lease payments) look to be significant, $17.3 million in the first half of 2013 and $28.9 million for the full year 2012. But most of those expenditures are for two new seismic recording systems that the company defines as growth capital. In 2012 the company bought a 10,000 station Hawk 3C wireless recording system for $17.8 million and in the second quarter of 2013 they bought a 6,000 station Hawk 3C system for $11.2 million. My understanding of seismic is that once you have the equipment, maintenance does not cost a lot. Ignoring the growth expenditures suggests that maintenance capital is around the $10 million mark.

The company generated cash flow from operations of $30 million in 2012. So far in 2013 they have generated cash flow from operation of $20 million. So free cash flow was around the $20 million mark in 2012, and it will likely exceed that this year. Given that they once again have a healthy backlog in their offshore seismic business, and that activity is strong for both domestic on-shore and international segments, I don’t think they are going to have any trouble eclipsing their cash flow from 2012. It could easily be $40 million for the year.

Albeit its a tough business, there is no “product”, just contracted services to customers. If customers dry up, which would happen if oil prices fell significantly, the company will feel pain. Nevertheless the stock is trading at somewhere between 2x and 4x forward free cash flow, depending on the estimate you want to put on this year’s numbers and whether you think its appropriate to factor in the lease obligations into the enterprise value. It’s cheaper than it should be in my opinion.

But it’s also illiquid. The stock is tightly owned, mostly by Ron Mathison, who is the founder of Calfrac and owns 37% of the stock, and the CEO Richard Habiak, who owns another 10.6% of the shares. It took me a long time to accumulate a position, and I would not recommend chasing it. It is the sort of stock that you could end up having to sit on for a significant amount of time before seeing something happen. But I’m hoping the wait will be worth the trouble.

Hi, I like reading your blog, I was concedering buying Tesla because a newsletter guys, on Stanberrey & associate mentioned that he is looking at a seismic company

”Frank Curzio

P.S. I’m writing my next issue of Small Stock Specialist right now… I’ve discovered a small seismic company that’s trading below book value… Insiders are buying… And the company is expected to grow earnings by more than 50% annually over the next two years.”

Could be Tesla but I don’t think there has been any insider transactions for a while. I bet he’s talking about Pulse Seismic. That seems to be on more people’s radar and there have been insider transactions: http://canadianinsider.com/node/7?menu_tickersearch=Pulse+Seismic+Inc.+|+PSD

Its a nice post. I love to buy tesla after reading your post. Tesla stock is trading to the tune of about $1 billion a day.

This post is hilarious. Great ideas, Lsigurd.

Hey Lsigurd, any opinion on Pulse Seismic? Not familiar with this industry but it seems owning the seismic library is quite beneficial. Recently mentioned at Value Investing Congress and also a Seeking Alpha article.

Its a pretty different business than Tesla because of the library. I’ve never felt super comfortable with Pulse, and I could be totally wrong about this, but here is why: While its always good to have a product to sell, rather than just your services, but owning a seismic library is a very different kind of product. There is generally 1 buyer, the company that owns the leasehold, and whether or not that buyer needs seismic depends on whether they are about to delineate new drilling or not.

So with Pulse you have to be able to get comfortable with their library, and I dont really have any insights into whether they have seismic data that will be desirable in the future, or not. So that has been my hesitation there.

Is the significant ownership by a Calfrac founder actually a significant competitive advantage? Aren’t they essentially locked in as a key service provider for Calfrac?

Have the recent developments at Palliser made you less than less comfortable averaging down? If their NAV estimates are reliable, it looks cheap (so long as they can manage their liquidity).

Yeah I really missed the market with Palliser. As I wrote back in January I sold about 20% but I’ve held the rest the whole way down. big mistake and a good lesson about cutting losses. I wouldn’t average down because I really have no idea if it turns around and whether they can get the cash or the white knight to get through this. Who knows?

This was a lesson for me as well. So much abysmal capital allocation in Cdn wildcat E&P!