Week 168: Cutting my gains

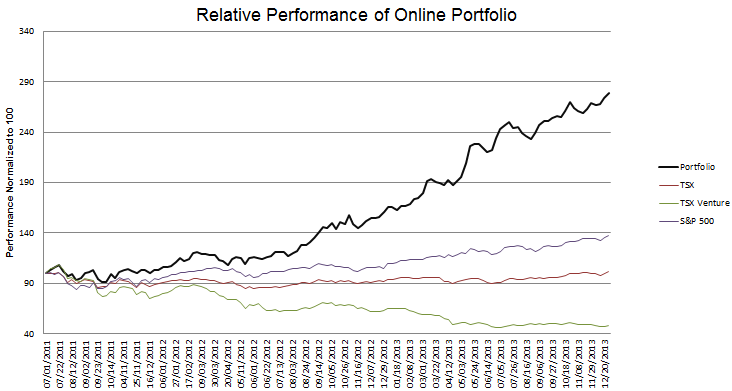

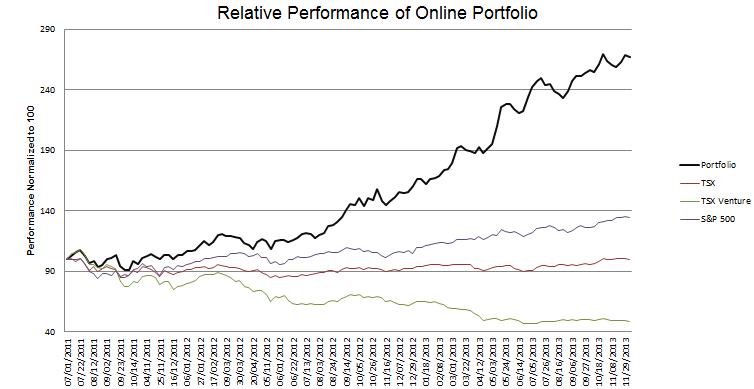

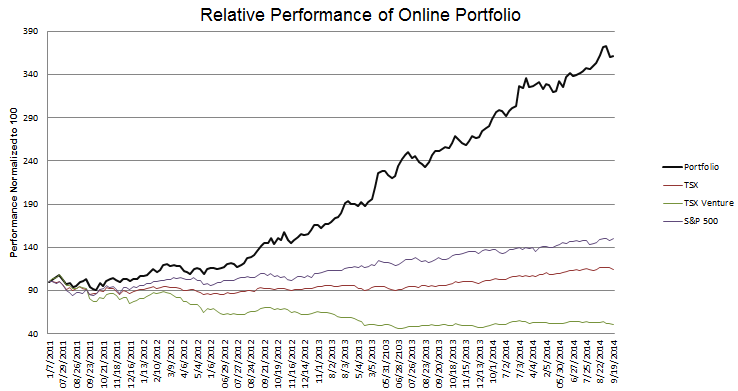

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

I don’t know if the chart of performance really does justice to the volatility my portfolio has had over the last couple of weeks. It feels like much more of a roller coaster than that little blip in the trend that you see on the screen.

I sold out of the rest of Pacific Ethanol and Rex American Resources in the first half of this week. I hemmed and hawed through the weekend, even briefly added to my position to Pacific Ethanol on Monday (at the same time I was reducing my position in Rex American), but the volatility of the stocks, the declining price of ethanol, and specific to Pacific Ethanol, my uncertainty with respect to their corn basis (I concluded tentatively it is actually quite a bit higher than Q2) led me to capitulate on many of my shares on Tuesday. I followed that up by selling the rest on Wednesday in the minutes that followed a very bearish EIA inventory report (+800,000bbl!). I tweeted on my sales at the time.

My caution turned out to be fortuitous as the stocks continued to fall the rest of the week. I was even able to catch a few dollars of profit on the way down; always remembering the old classic to which this blog takes its namesake, I took the lesson that if a stock is to be sold it is likely just as well sold short, and so I took a small short position in Rex American and a few $18 puts on Pacific Ethanol. The puts were sold Friday and my short position has been cut more than in half, so these were merely short term trades taking advantage of a clearly bearish dynamic. Read more