Returning to PHH Corp

On September 19th I received an email from a friend (hat tip @VermeulenGold) that an activist investor, Orange Capital, had taken a 5% position in PHH and written a letter to management outlining their recommendations on creating shareholder value. I immediately took a position in the stock.

In order to describe why I acted so quickly, let’s go back to why I sold PHH in the spring. There were two reasons. One was my concern that gain on sale margins would compress significantly – a concern that remains valid today (and could still be my undoing with the stock). The other was that there just didn’t seem to be a catalyst to realize the valuation gap that I saw.

Now, with that catalyst having materialized, I want to be along for the ride.

I wrote about PHH over a year ago. I described the company as having Joel Greenblatt type of spin-off potential. The company had two disparate businesses with little in common. There were aspects of the one business that clouded the accounting of the other. And one of those businesses, mortgage origination, had a not well understood but valuable asset in the mortgage servicing rights that were held.

Now that I have had a chance to read the Orange Capital letter in full, I am happy to see them draw similar conclusions. I added to my position in the company on Monday. It’s a 4.5% position.

The Orange Capital Letter

I would recommend reading the letter in full, it is available here, but briefly, these are the four initiatives suggested by Orange Capital:

- Create a captive finance vehicle which would own a significant stake in the Company’s newly originated and existing excess MSRs

- Hire a financial advisor to pursue a tax-efficient sale or IPO of Fleet Management

- Immediately commence a share repurchase program or tender offer for $150 million of the Company’s common stock

- After resolving outstanding repurchase obligations and securing new financing for newly originated MSRs, offer to exchange the 6% convertible notes due 2017 for a combination of cash and common stock

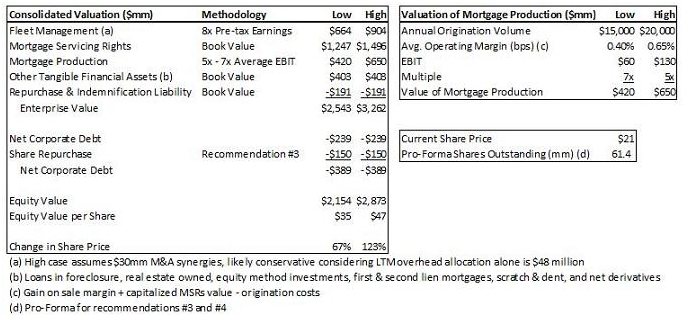

Orange Capital provided the following intrinsic valuation of the company.

Clearly, a realization of anywhere between the $35 to $47 equity value that Orange Capital sees in a reasonable time frame would make PHH a worthwhile investment.

Is the Orange Capital Valuation Realistic?

I would propose that valuing Fleet, which produces a steady stream of free cash flow, at 8x pre-tax earnings is conservative. Below I have reproduced the Fleet segment income statement from the last 8 quarters. Fleet is on pace for a litttle less than $1.20 per share of after-tax earnings.

Given that Fleet earnings have been consistent and growing for years, I believe that a 15x multiple on those earnings would be appropriate. That would give Fleet a valuation of about $1 billion, or slightly above the high end provided by Orange Capital. Note that Fleet’s earnings include corporate overhead allocation, so it is reasonable to assume that they approximate the earnings of a stand-alone entity.

Given that Fleet earnings have been consistent and growing for years, I believe that a 15x multiple on those earnings would be appropriate. That would give Fleet a valuation of about $1 billion, or slightly above the high end provided by Orange Capital. Note that Fleet’s earnings include corporate overhead allocation, so it is reasonable to assume that they approximate the earnings of a stand-alone entity.

Orange Capital is valuing the capitalized servicing book at between 94 and 112 basis points. I’m not sure how Orange Capital is taking into account the subserviced loans, they aren’t broken out elsewhere in the valuation table but if their cash flow stream is included in the MSR estimate then the number they came up with is lower. Assuming that subservicing is not included, Orange Capital is valuing the capitalized servicing book at a 3.2x multiple. I think that multiple could increase to 4x as rates rise and more clarity is gained on the pre-payment and default characteristics of the loan book.

It’s also worth noting that in the Orange Capital letter it was implied that PHH management is sympathetic to the realization of value from its existing mortgage servicing rights book. So we may hear something about that sooner rather than later.

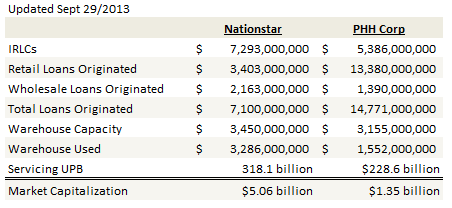

When the servicing segment is taken together with the mortgage origination segment, and compared to what is a fairly similar operation at Nationstar, PHH appears to be valued absurdly low. I did a comparison between Nationstar and PHH last year in this post. Below I’ve updated that comparison using second quarter results.

While I understand that Nationstar has been growing their business at a far faster rate than PHH, I think that the valuation discrepancy between the two companies is out of line. Remember that I am comparing the overall market capitalization of PHH, so not subtracting anything for the value of Fleet. The difference is so stark, I have wondered if I am missing something. Maybe I am, and please tell me if that is the case.

While I understand that Nationstar has been growing their business at a far faster rate than PHH, I think that the valuation discrepancy between the two companies is out of line. Remember that I am comparing the overall market capitalization of PHH, so not subtracting anything for the value of Fleet. The difference is so stark, I have wondered if I am missing something. Maybe I am, and please tell me if that is the case.

Conclusion

I added a position in PHH after the news from Orange Capital, and increased the size of that position on Monday after examining the company more closely over the weekend. On Monday there was also news of a second major shareholder, as Senator Investment Group reported a 7.6% position. There is a brief description of Senator here. I’m not sure if they have activist inclinations or not.

My position is a little bit larger than usual, but that is because I’m comfortable with the liquidity of the stock, and because the nature of the situation is very event-driven; I will hopefully wake up one morning and find news that one or more of the initiatives suggested by Orange Capital is being implemented and the stock will immediately react higher.

As for the risks, one risk is the ongoing performance of the origination business, which is unlikely to produce very good third quarter results, though this will hopefully be balanced by out-performance of the mortgage servicing book. The other big risk is that management ignores the calls for change, which has been done in the past. This could happen, and it would be nice to see more activist investors getting involved.

Like many of my investments, the pieces are all there, and there appears to be a catalyst that can put them together. Now we’ll just have to watch and see how it plays out.

HI Lane, Have you looked at mgmt share ownership/compensation incentives? I’ve not and would love your thoughts on it i fyou have them.

Nice article, it seems as if OCN would apply as a potential investment opportunity also as they are only trading at 10 times 2014 estimated earnings and also have potential and seems intent to initiate a share buyback. They are purely a MSR company and would not have the drag of the origination business. Thoughts?

I dont follow OCN very closely. But MSRs is probably still a good place to be.

I gave up on PHH in disgust when they priced the conv preferred at 1/2 tangible book. If they needed cash that bad WHY DIDN’T THEY SOLD FLEET ALREADY? Really criminal mismanagement to sell shares at that level.

Run away from NationStar stock it is only a matter of time before they are sued for Millions if not Billions. Their Customer Service is non-existent or at least as bad as I have ever seen. The lower level people in customer service can’t escalate to a supervisor. They are told to tell people someone will call them back the next day. That never happens.

Their insurance department is run by complete idiots. Normally your agent faxes the policy and you never hear about it again. In NationStar my agent faxed the policy and they entered it wrong. In January they sent a letter saying your policy was cancelled two months after it opened and I made a onetime annual payment in full. So it didn’t cancel and I checked. I had the agent send it again, now in February NationStar is telling me they are going to buy me a policy for $5700 a year which is more then 6 times what I have paid already. I have a policy and have given it to them three times now. NO BODY IS HOME at NationStar and in the two years I have had more trouble with a paid on time mortgage. We should sack the CEO and let me run the place.

Remember when investing, if a company like this one doesn’t care about its customers they will never ever ever return. Those companies are the ones you read about. Customer Service is a choice and this Company SUCKS and their CEO most be a complete idiot, or maybe he is just in competent. I am refinancing just to get rid of these idiots. I have offered to help with Customer Service since it is so broken and so easy to fix.

I am also buying a single share so I can tell their CEO what an idiot he is.

Shawn