Week 119: Getting Back on Track

Portfolio Performance

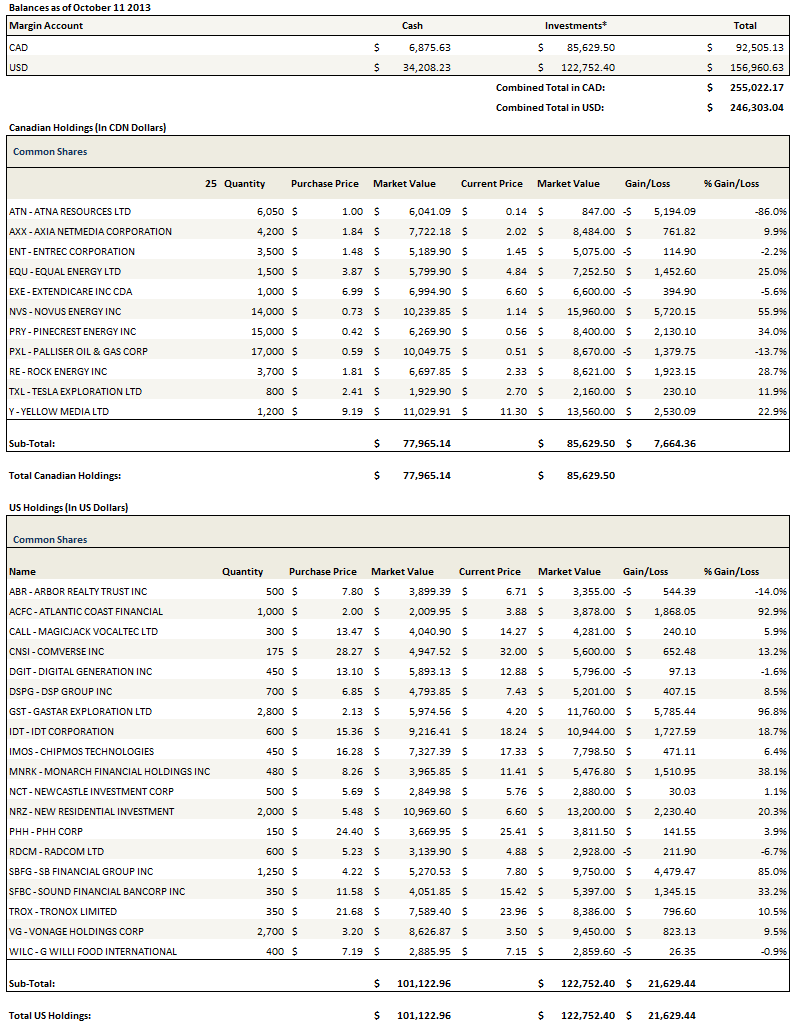

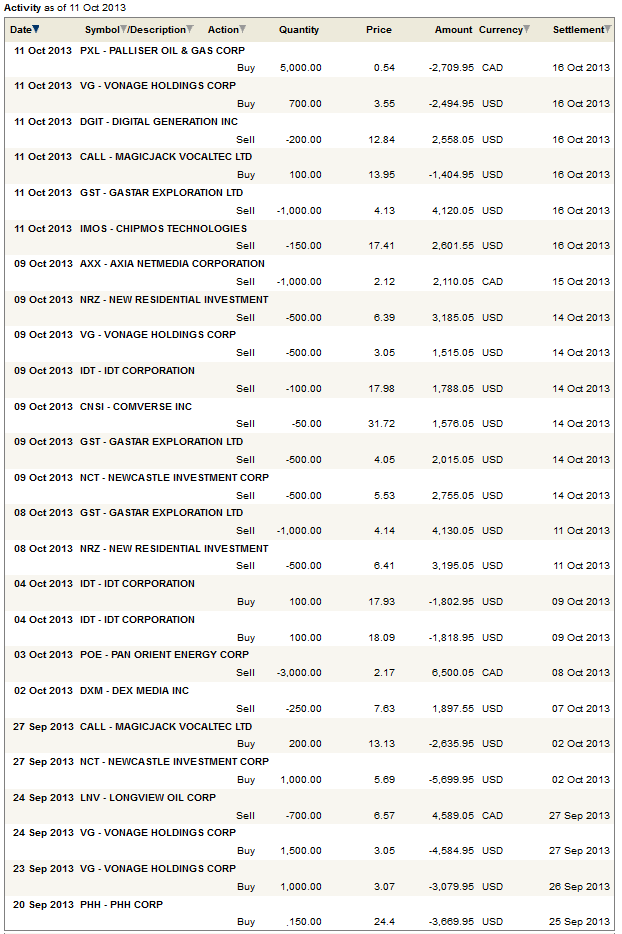

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

I always write words like those in the title with some trepidation. I’m never really sure if things are back on track, or just bouncing on their way to oblivion.

Nevertheless, the tangible evidence is that my portfolio has recovered and made new highs in the last month. I had a blip to the downside in August, and when I look back on that blip, I can attribute it to a few bad decisions. There was Niko Resources, Walker and Dunlop and Dex Media obviously and to a lesser extent Vitran and AMBAC. All of these stocks had flaws that I should have recognized and gave greater consideration to, and none of these stocks deserved to be allocated outsized starter positions, yet in the case of Niko and Dex Media that is exactly what I did.

I’ve gone back to the drawing board since then. I’ve tried to be more careful with my stock selection, tried to spend more time thinking through each idea before adding a position, and tried to work with the attitude that an opportunity passed up is better than one taken and lost on.

The Debt Ceiling and Reducing Risk

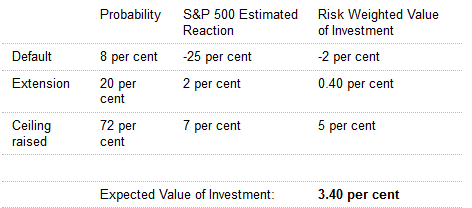

I’ve also tried not to guess what the government might do. I was reading this article in the Globe and Mail a couple of days ago. The article describes using a risk-weighted approach to determine what sort of portfolio adjustments you should make in reaction to risks associated with the debt ceiling. The article assigns a high impact to the scenario that a debt ceiling agreement is not reached (-25% correction in the S&P) and a fairly low probability of that event occurring (8%). The other scenarios, that the debt ceiling is temporarily increased and that a more permanent agreement is reached, are assigned much higher probabilities but lower (positive) impacts. Overall, the impacts and probabilities mostly even out to a little more than 0%, which means that you should do nothing. I’ve reproduced the summary table below:

I don’t buy this kind of thinking. I seems to me like funny math and even if its technically and statistically correct, I reject it. I look at it this way. In the next week or two one of two things is going to happen. The debt ceiling will get hit or it will not. If it does the market will do very poorly and every stock you own will likely go down. While we can try to assign a probabilistic number to that happening, at the end of the day it comes down to the personalities, best interests, biases, and egos of the people involved, and who knows what they are. I don’t think that the factors involved are conducive to being reduced to probabilities. So as an investor, you have to ask yourself if you are willing to take that hit. And if you aren’t, then you have to sell.

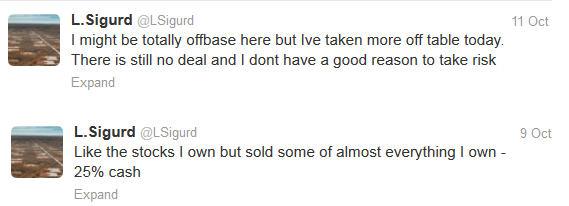

This week I made the following tweets.

In my accounts I go into the weekend with more than 25% cash (I’m a little under that in the practice account I show here, at around 23% including my remaining Novus position, as I didn’t quite keep up with the selling I was doing elsewhere). I should perhaps be at an even higher level, but many of the stocks I own are so obscure and out of the mainstream that I feel some confidence that they will be spared some of the carnage that will occur if the debt ceiling is not raised out of indifference alone. The stocks I trimmed the most were the one’s that have proven most volatile to market swings.

I have absolutely no idea how this thing ends. It makes sense that it will end well and a deal will be reached. Nevertheless I have no confidence in politicians to make sensible decisions. So I have reduced my bet significantly, and will reduce it further on any evidence of deterioration of the negotiations.

My VoIP Plays

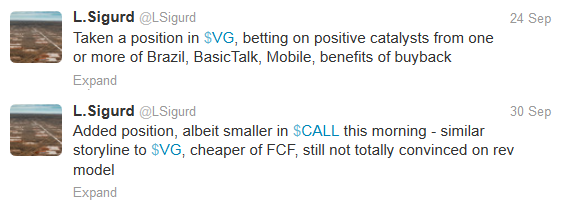

The only two new positions I want to mention quickly are Vonage (VG) and MagicJack (CALL). I bought both stocks in late September. I’m in the process of writing a more detailed post, which I was hoping to have finished by now but there have been a lot of things going on that have limited my writing time of late, so I will leave out most of the details until then. At the time I added the stocks I tweeted the following:

I like both of these names. They are both generating significant free cash flow and from what I have read about the VoIP technology it is greatly improved from its early disappointments. I like Vonage a bit more because they have more immediate catalysts (they recently released BasicTalk, which is a low cost domestic product that will compete directly with what MagicJack offers, and they are in the process of expanding into Brazil), I like their branding more than MagicJack (I find the MagicJack advertising strategy to come off a bit like an infomercial) and because I have some reservations with MagicJack’s revenue model (I will have more to say about that when I publish my full post on the two companies).

Vonage also bought Vocalocity this week, which plants them in the small and medium sized business market. This was responsible for the bump in the stock this week. There is excellent detail on the acquisition in the conference call Vonage hosted to discuss it. I have added to both positions since my initial purchase as the thesis is playing out favorably so far.

A Few Positions Sold

I completely sold out of two positions: Longview Oil and Pan Orient Energy. Both of these were victims of my attempt to really think hard about why I owned something. In both cases, the conclusions I drew were not sufficient to hold on.

With Longview, there’s nothing wrong with the company. The stock is cheap compared to its peer group of dividend paying oil stocks, I like the low decline base, the dividend is still nearly double digits. But for me it came down to there being other names I liked more. I had difficulty justifying Longview over my other oil holdings; over Rock Energy, Pinecrest, Palliser, Gastar and Equal. In particular, with Rock, Pinecrest and Palliser I saw greater upside and lower valuation. Maybe there is more risk, but I’ve looked at each of these names in depth and I’m comfortable with that. So I sold after having already added to my positions in all three. I may revisit at a later date.

As for Pan Orient, it was a tough call but the stock moved up on speculation about its Indonesian acreage and that isn’t really why I owned the stock. They were fortunate that a neighbour (Ramba Energy) has drilled a couple of wells on adjacent land and stumbled on a couple of hits. The discovery may spill over on the Pan Orient’s land and if so they will be allocated a portion of the oil produced from the field. The company is supposed to drill a well early next year to test the prospect on their acreage.

The concern I have is that this put 20% on the stock which is another 20% that it could fall if Sawn Lake doesn’t fly. It’s also a 20% profit that I can scalp without even having to wait if my thesis plays out. I’m not so convinced that Sawn Lake will be a success that I am willing to hold on regardless. So I took the profits and freed up some cash.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}