The other VoIP Play I added: magicJack (CALL)

While I was investigating Vonage I was introduced to their competitor magicJack by an acquaintance on twitter. Interestingly, in the process of talking me into magicJack he talked himself out of his own position. Let this serve as foreshadowing that this is not an investment without its warts.

The Positives

magicJack, like Vonage, provides voice over IP for telephone services for consumers. magicJack sells a little dongle like device that plugs into the USB port of your computer. You plug in the device, plug in your phone to the other end, and are off to the races. The company is best known for the incessent commercials they have pummeled at people for years. They also have a mobile app available on Android and the iPhone that allows you to make free long-distance and international calls as long as you are connected to Wifi.

magicJack has an enterprise value of about $250 million, comprised entirely of its market capitalization less $45 million of cash. In the first 6 months of the year the company generated a little over $21 million of cash, which puts the stock at an attractive 6x Enterprise Value to Free Cash Flow. If you step back to prior years, free cash flow generation as per the balance sheet was even stronger. The company has also been able to grow its customer base over the last few years, though this growth has tapered off some in the first half of 2013. A new device was launched in June that should provide a boost to growth, with the extent of that boost likely determining the stocks price in the short run.

Now the Negatives

On a free cash flow basis, magicJack is cheaper than Vonage. As I already noted they have also been growing their subscriber base, while Vonage has been flattish to down. So why did I decide to take positions in both companies, and make my position in Vonage the larger of the two?

The first thing is that MagicJack just feels, for lack of a better word, a bit cheezy. Take a look at their website. Its like something you’d expect to see from Ron Popeil. Now Ron Popeil also delivered highly profitable products for a number of years, so take that with a grain of salt. But try to find pricing on the page. Its not easy. Compare that to Vonage. Clean, concise and with the information I want (and that they want me to know) right in front of me.

Similarly, while I haven’t used the MagicJack mobile app myself, I have been told that it feels a little amateurish and again the app provided by Vonage is a much cleaner, slicker interface.

Second, there are questions about the company’s past behavior. In January, Copperfield research put out a short thesis on the company. The full piece is available here, and if you want a short summary there is a Bloomberg article that discusses it here.

Most of Copperfields case revolves around the former CEO and the practices that took place under his watch. Copperfield points to a number of misleading accounting techniques, most of which have to do with supplying different information in press releases than what is in the SEC filings. They also highlight a lawsuit that has since been dropped, make a number of allegations about the character of the former CEO, point to the new CEO’s previous association with the former CEO, and to actions made by the former CEO that they think were intended to manipulate the stock price.

Of all the claims made in the piece (and there are a lot of claims; its a 45 page report), there are two that gives me pause. First Copperfield points out that magicJack’s center of innovation is this building, which I have to admit is a bit strange. There really is a laundromat across the street. It seems like an unlikely location for innovation. Combined with what does seem to be extremely low research and development costs, there seems to be a flag waving in the wind.

Second, the lawsuit that Copperfield references was with respect to 911 fees that telecom providers are supposed to pay to counties in return for the 911 service. magicJack had not been paying these fees. While the lawsuit has since been dismissed, it did get me digging further. In the past magicJack has gotten around the 911 charge by structuring their operations as two distinct businesses, one that sells the device and handles incoming calling, and another that handles outgoing calls. This structure allows magicJack to get around being labeled “an interconnected VoIP” service, which in turn technically makes them exempt from the fees. This SeekingAlpha article (which is itself another short thesis) does a good job describing the structure and its implications.

My worry here is not so much the 911 fees; in fact it appears that magicJack has since started collecting fees in at least some counties it operates in. My worry is more of a “what else is out there” nature? I know enough about the telecom landscape to know that I don’t have a hope in hell of understanding all the FCC rules, how they are going to change, and what this company might be doing to get around them. One of my first investments was a company named Covad, that appeared to have a bright future until it was blindsided by an FCC rule change. That has always stuck with me and made me wary of all things telecom.

magicJack operates in what appears to be a fuzzy area, and it scares me a little to think what might happen to the stock if the FCC tries to make it clearer. Its a worry for me, but not a show-stopper. Its a reason why, as I have stated repeatedly, my position in magicJack remains much smaller than Vonage and will continue to stay that way.

The magicJack Business Model

I am also given some pause by the revenue model, though this concern has been mitigated as I’ve looked at the company more closely. The company generates a good chunk of its revenues and margins when a customer first signs up for a device. They buy the magicJack dongle, which is about $40 for the original magicJack or $50 for the new magicJack Plus, and then, after getting the first year of service for free, every additional year is $30 per year. So the service is quite cheap, especially compared to Vonage, but the upfront device commitment is more expensive.

Depending on how you allocate expenses and depending on the quarter, device margins are somewhere between 60% and 70%.

When I first looked at the subscription side of the business (the company calls these access right renewals), I found them to be only marginally profitable on an operating basis. This was a red flag to me. Most companies will give away margins up front if they can make it back from the recurring subscription fees. magicJack seemed to have created an incentive for getting new customers or getting existing customers to upgrade to a new device, rather than on retaining existing customers on their current plan.

However that first take was done using the YE 2012 numbers, and now that I have looked at how the business has evolved in the first few quarters of the 2013, I can see that the company has hit an inflection on their subscription margins where the incremental subscriber is much more accretive than they have been in the past. Take a look at the chart below. I’m showing the Access Right Renewals and the gross margin generated from them. You can see how margins have taken off in the last few quarters.

This is what really sold me on the stock. Once I saw the evidence of a decent margin recurring revenue business, I thought magicJack might be worth the punt.

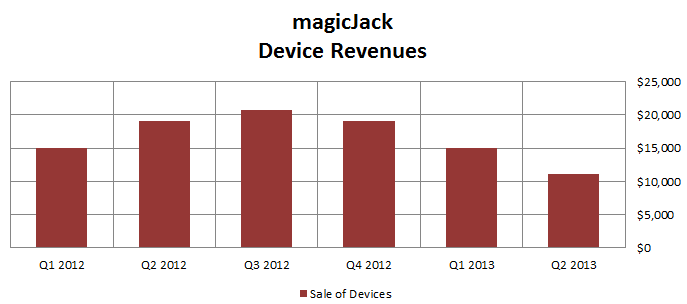

Nevertheless the fact remains that the company makes a lot of its money on the sale of the device. And device sales have been weak. I think that is what has hit the stock over the last 9 months. Take a look at revenue from devices over the last 6 quarters.

The third quarter device sales number is going to be an important one. The company released the new magicJack plus device in June. Overall device sales are expected to improve as some customers upgrade and others are attracted to new features. The company was pretty positive about the early sales numbers on the conference call; they talked about customers replenishing their inventories multiple times already, and how their own internal sales number thus far had exceeded the previous device launches. So we will see. If the device sells like hotcakes, the stock could be set for a squeeze.

The third quarter device sales number is going to be an important one. The company released the new magicJack plus device in June. Overall device sales are expected to improve as some customers upgrade and others are attracted to new features. The company was pretty positive about the early sales numbers on the conference call; they talked about customers replenishing their inventories multiple times already, and how their own internal sales number thus far had exceeded the previous device launches. So we will see. If the device sells like hotcakes, the stock could be set for a squeeze.

Conclusion

I watched magicJack go straight down for a couple weeks straight and I have been torn about whether to add to my position or just wait this one out until it turns around. The awkward revenue model, the somewhat twisted history (the former CEO and founder has had a bit of a checkered past with the stock), and probably the biggest factor, the chance of another short attack.

Nevertheless, when it hit $11.50 I caved and added. Its still not a large position for me (3.5%) but I do like the immediate opportunity that third quarter earnings present (they will be released on Tuesday). The new magicJack device will have had a full quarter of sales and if that leads to an up-tick in overall device sales, I suspect the stock will receive a pop. We’re in a good market for upside surprises right now and there is a large short interest in the stock. I have listened to the first and second quarter conference calls a few times now and I think the new CEO sounds reasonable and direct.

The company is what it is, they provide a device that doesn’t get great reviews for call quality (I looked it up on Consumer Reports and they had given the magicJack Plus, which is the previous version of the device, a couple of the infamous black dots for quality), but does get the job done for a number of consumers for a very cheap price, and does provide a lot of free cash. Its the kind of stock that I like; one where you can focus on the negatives and come up with reasons for a very low stock price, or focus on the positives and come up with reasons for a much higher one. Right now its trading at a level that I think mostly reflects the negative reasons, so with some change in sentiment there is plenty of room for upside.

As a consumer, i decided to go VOIP and looked at Magicjack, Ooma, Vonage and Obi.I went with Ooma, because i thought that Magicjacks and to some extend Obi’s voice quality was too poor, Vonage was too expensive. Ooma is more expensive upfront but reoccurring fees are very low. So far i am satisfied with my choice.

I think Magicjacks marketing is questionable and that seems to relate to the way the company operates as well. Too many questionmarks to out serious money in it, but probably worth a small bet.

I dont disagree. i have spent a fair bit of time researching the options and Ooma seems like the best product for the price. I have considered getting Ooma myself. However I do suspect that Ooma is operating at a loss; they are a private company and so there is very little information available on their financial performance. I don’t really understand how their business is sustainable over the long term when they basically get nothing in recurring revenues but have escalating recurring charges (as more people join and use their service on an ongoing basis).

Obihai might have trouble now that google voice will no longer be able to be used with it.

Any reasons why the CEO sold 14 million worth of stock? at 15$?

Probably part of the deal that had him sever his ties with the company. I think its a good thing that he is no longer involved.