Week 123: Lot’s of Volatility

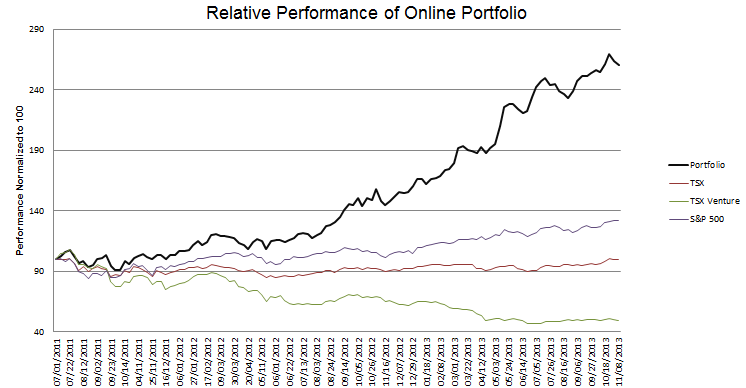

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

The third quarter earnings season is shaping up a lot like the second. Lots of volatility, lots of disappointment, and dramatic falls followed by recoveries.

I think its a symptom of our malaise. Things just aren’t that good. Yet stocks are juiced by all the money sloshing around. So you get this dynamic during earnings where numbers come out and aren’t that good, which leads to a steep sell-off in the stock because the current price can’t be justified based on the earnings and outlook. But then the liquidity effect kicks in, arresting the decline, changing the momentum on its head, and sending the stock back up.

Needless to say, this isn’t a healthy dynamic.

Its a test of your nerve. Digital Generation, for example, moved down from $12.35 to under $11 in the day and a half after earnings, only to recover most of that on late Friday morning and into the afternoon. Gastar ran all the way down to $4 before recovering to $4.40 and finishing the week over $4.50. I was able to initiate a new position in Alaska Communications after it dropped from $2.80 to $2 in a little over a day after earnings were released.

But that is the world we live in at the moment. No sense in complaining about it. One can only do their best to navigate it.

I wrote about a lot of my portfolio moves in the prior posts I did a couple of weeks ago. I won’t spend any time reviewing those moves again. But I did make a few changes since that time.

Alaska Communications Systems Group (ALKS)

The first was the aforementioned position in Alaska Communications Systems Group (ACS). The stock has been on my radar for a while, and when it got into the low $2’s I felt compelled to take a position. The company runs a wireless and wireline telecommunication service provider business in Alaska. They have a heavy debt load of about $400 million, and a market capitalization of about $100 million (calculated at a share price of $2.10, which is where I bought the stock). On an EV/EBITDA basis they are trading at about 5x, and they have, in the past, been able to generate a decent level of free cash flow. They expect free cash flow to be $20-$25 million this year.

The catalyst that caused the stock to reach almost $4 in August was a deal they made with another Alaska service provider, GCI. ACS and GCI combined their wireless businesses into a separate entity, Alaska Wireless Network (AWN). GCI took a larger stake in the business (67%), while ACS got a $100 million cash infusion and preferred distributions from AWN of $50 million in the first two years of operation, followed by $45 million in the second two years.

I’m not entirely sure why the stock sold off so sharply after the third quarter earnings release. Reconciling GAAP numbers with all the one-time items is certainly confusing, so maybe that played a role. The third quarter is typically a high CAPEX quarter (this was stated by the company in the earnings release and I verified it by looking at Capex over the last few years) so the free cash flow generation in Q3, even after considering the one-time effects and a delayed payment from AWN, was minimal, so that might have had an effect as well. Whatever the reason was, it appears to me that the longer term story is intact. That story is, quite simply, deleveraging of the balance sheet with free cash put against debt and hopefully a subsequent repricing of the equity to reflect this.

Adding to New Residential (NRZ)

The second add was an old favorite, New Residential. It seems like pretty much any time the REITs get hit, New Residential gets hit as hard or harder than the rest. This last round of beatings was no exception, as the stock broke the $6 mark at one point on Friday morning.

I like the management of the New Residential/Newcastle/Fortress consortium; they did a smart thing getting Newcastle into MSR’s and now MSR’s make up about half of the assets of New Residential. They also seemed to have scored a coup with the purchase of a consumer loan portfolio portfolio from HSBC. If you look at slide 16 from their third quarter earnings presentation, based on the performance of the portfolio to date, the company expects levered returns on their consumer loan portfolio of 37%. As the slide shows, if New Residential were to sell that portfolio at a 10% return and under the assumption that the portfolio continued to deliver an 8% consumer default rate, the result would be $200 million (about $0.80 per share) of extra value to New Residential not currently captured in book value.

A similar case could be made for the mortgage servicing portfolio if rates start to rise. The current value of the excess mortgage servicing rights that New Residential holds is based off of the assumption that consumer prepayment speeds average 21% per year. In the third quarter, as rates rose and refinancings tapered off, this decreased to 19%. As prepayment speeds decline, the duration of the servicing asset increases (it generates cash flow for longer) and thus its present value is higher.

On their 3rd quarter conference call, Nationstar had this to say about the increase in value of servicing assets as interest rates rise:

We expect our servicing assets to appreciate in a rising rate environment. During previous of rising rates, servicer valuation multiples have traditionally increased in concert with rising rates. From May 2003 to May 2004 and June 2005 to June 2006, interest rates increased by more than 120 basis points. During each of these periods, the valuation for servicing companies expanded by approximately 4 turns of PE multiple. In the current rate environment — in the current environment, rates have risen by more than 100 basis points, yet the valuation per servicing companies have only increased by approximately 1 turn.

To extend this line of thinking, what happens if the economy improves and if interest rates rise? Surely refinancings will slow further and defaults will continue to fall. What does this do to the book value of New Residential’s mortgage servicing portfolio? Certainly it becomes significantly higher than it is currently.

Things are also afoot at the Fortress complex as they work on ways of improving the tax structure for the mortgage servicing rights held by their group of companies. On their 3rd quarter call Nationstar said they are exploring ways to reduce their tax footprint by changing the holding structure of their servicing portfolio. Similar comments were made on the New Residential 3rd quarter call, with the implication that New Residential may be taking on more of Nationstar’s servicing.

Wes Edens made comments towards the end of the call that the opportunity in mortgage servicing is shifting to one of maximizing the efficiency of the capital structure that holds the servicing right in order to get the most cash out of it. He went on to point out that the REIT structure is a very efficient way of minimizing the tax implications of the servicing right, and alluded to future announcements that may be made in this respect. This was followed up by a question from Henry Coffey where Edens essentially confirmed that some sort of MSR transfer out of Nationstar was in the works. So we will see.

Finally, the company also said on their call that they expect to pay a small top-up dividend at year end to account for the higher GAAP earnings that are being generated (the company earned 24c in Q3). This is in addition to what is a 11.7% return at the $6 price

Between the consumer loan portfolio and the mortgage servicing rights, New Residential has 67% of total assets invested in vehicles that are positively leveraged to improvements in the econony in higher rates. I think that the sell off that occured on Thursday and Friday was a mistake. I loaded up on the stock on Friday morning when it hovered around the $6 mark for most of the first two hours of trading. Its quite a large position by my usual standards. I won’t keep it all for long; I plan to sell it back down to something more reasonable when the stock gets about 10% higher.

Stupid earning moves

I have a tendency to do dumb things heading into the earnings period. It’s a habit that I really have to stop. The only saving grace to this behavior is that I tend to keep these dumb “flyer” picks to extremely small size.

The two stupid moves that I made this quarter were taking small positions in Dex Media and Alon Energy Partners in the days heading into their earnings. In both cases the positions I took were only around 0.5%, so pretty small, but when you have sell-offs like you did in these names after they reported (DXM was down 12% before I sold it the morning after earnings, while Alon was down 10%) its still money lost.

In both cases the research I did ahead of time was cursory and clearly insufficient. With DXM I was almost entirely going off of the company’s assertion on the second quarter conference call that the decline in the on-line segment was due to the loss of a large customer. Third quarter results cleared the air on this; it was not a one time event. With Alon I was thinking that the Permian product would help spreads between the WTS crude that they source and the WTI benchmark. The company announced as part of their press release that this was indeed the case, the WTS/WTI spread had risen to $4.50 post quarter, but the third quarter earnings and current crack spread was bad enough to overshadow that.

Time to quit taking flyers and to stick to what I know.

What I’m looking at now

There are a number of stocks that have sold off significantly over the last fews days. Obviously there was Alaska Communications, which I have already added, but in addition there is Cherry Hill Mortgage, Dolan Company, Metalico, Global Telecom and Technology and a few others. But no positions in any of these names yet.

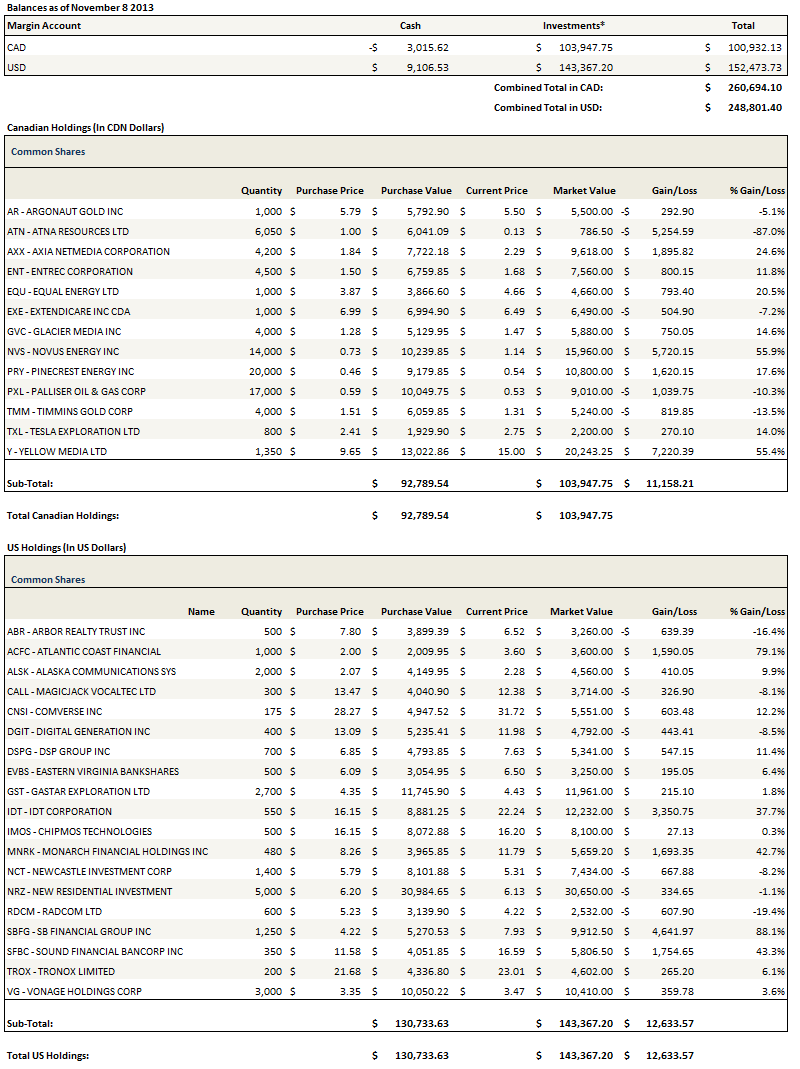

Portfolio Composition

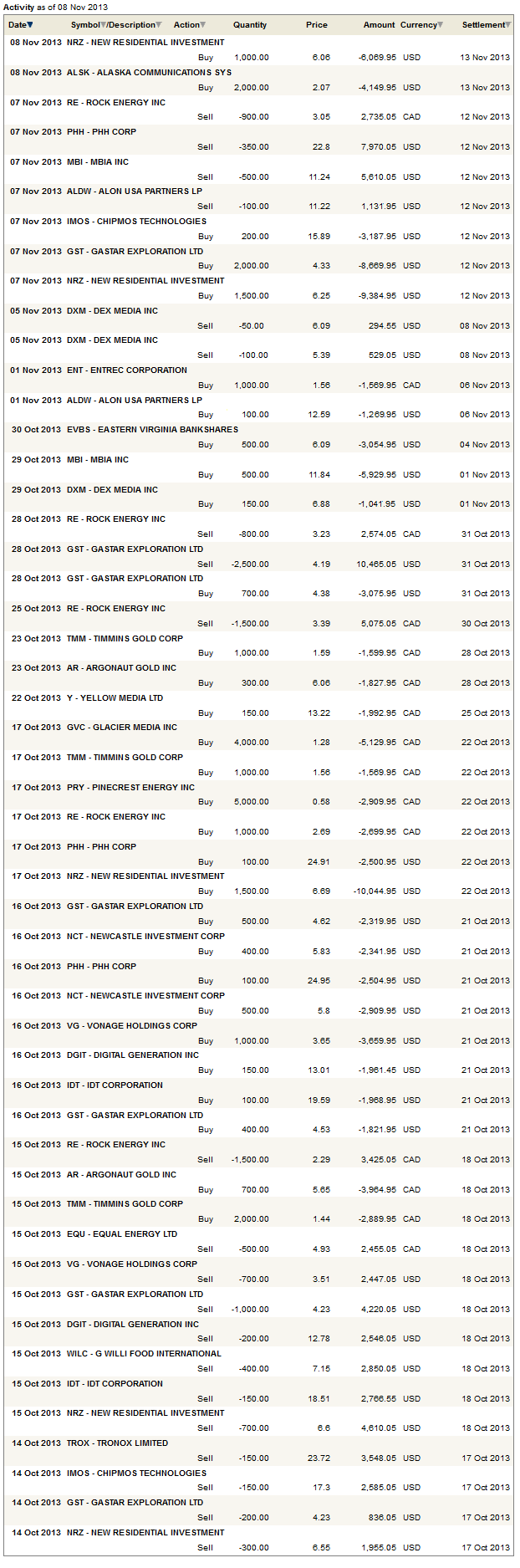

Click here for the last four weeks of trades.

{kind=link}

Have you looked at $XPLT? Substantial growth, profitable, tied to US auto sales. Good VIC writeup. Short & to the point, worth a quick read.

http://www.xpel.com/relations/default.asp

Thanks

Great blog; I always look forward to reading your write-ups every week or so. Any thoughts on the counterparty risk that NRZ has with NSM? I’m overweighted on NRZ and I’m thinking of trimming the position, but I do feel that the current price is a bit of a firesale. The 10-Q talks about the counterparty concentration risk with NSM and that NRZ may not be able to acquire suitable counterparties to acquire Excess MSRs without NSM. With NSM shuttering their non-core wholesale and distributed retail origination channels to Stonegate, do you think NRZ will have trouble getting solid Excess MSRs that can provide the same return in the future?

I dont think that is too much of a worry because I don’t believe NRZ gets msr’s from NSM on a flow basis. They have only participated as a counterparty when the two companies have bought a large portfolio from a 3rd party. As long as NSM keeps the origination biz that attempts to recapture its existing loans.

Hi I was a commenter on DGIT previously. Just curious what your current views are and if you plan to keep holding it. I sold out of my position because the corporate overhead appears a lot higher than I expected. Management said ~25% less than current runrate. Cost structure seems bloated given before they bought DG media (the current online business), it was making ~$10M in profit.

I am still holding it but I understand your concern. I have been waffling myself on whether I should keep DGIT.

Hi – you did well with a highly levered/turnaround theme recently to take advantage of QE. Any thought of reversing this theme to high-quality low leveraged companies should tapering begin? I know it’s not likely any time soon with Yellen but still wondering if it’s in the back of your mind.

That’s a good question. I think there is still opportunity on the leveraged side even once tapering begins because it will still be cheap to refinance. But I will pull in some of my exposure and move to higher quality companies for the simple reason that when we do have another recession the lower quality companies get hit hard

someone’s still holding out hopes for Dex: http://seekingalpha.com/article/1852701-dex-media-inc-a-potential-multi-bagger?source=email_inv_ar_0_0&ifp=0

I read it. Maybe they can turn it around. In retrospect, at $4 it was probably a good bet for some sort of pop but I had been burned twice. But I don’t think I will add back unless there is some evidence that they can turn around their digital business