Timmins Gold: Anatomy of a Gold Stock Valuation

I’ve talked before about my “rule” to average down when a stock gets underwater by 20%. This 20% threshold is not so much a firm line in the sand as it is an alarm bell to remind me to review my position and clarify exactly what it is I am doing. While in most cases at the end of it all I do decide to reduce my position or exit it entirely, there are also cases where my review leads me to become more confident in my position, and where I do not reduce but instead even add to it.

The 20% threshold was recently broken with Timmins Gold. The stock dropped past $1.10 (it has since recovered to $1.20 and, to give away the ending, I did buy more at $1.10 so I am now down about 10%). I bought both Timmins and Argonaut Gold back in October (I wrote about the positions here) as a way to trade my expectation of higher gold prices in the near term. Obviously that thesis did not play out the way I had hoped, at least not yet.

As I wrote at the time, my research into both names was not exhaustive and I ended up taking the analysis of a few brokerage shops with more faith than I usually might. Well that was my first mistake. It turned out that the original brokerage analysis was quite flawed and two of the firms have since downgraded their estimates and the stock significantly, after the release of an updated mine plan for the San Francisco mine. In the case of BMO, the downgrade was from $2.75 to $1.50!

With the stock down significantly, it was time to take a closer look and either admit that I had made a mistake, or that this was an opportunity in the making. My process consisted of getting my hands on the reports that were, at least in large part, responsible for the decline in the stock and then reviewing them in detail.

I wanted to answer the following questions:

- How did they get their numbers?

- Did I agree with them?

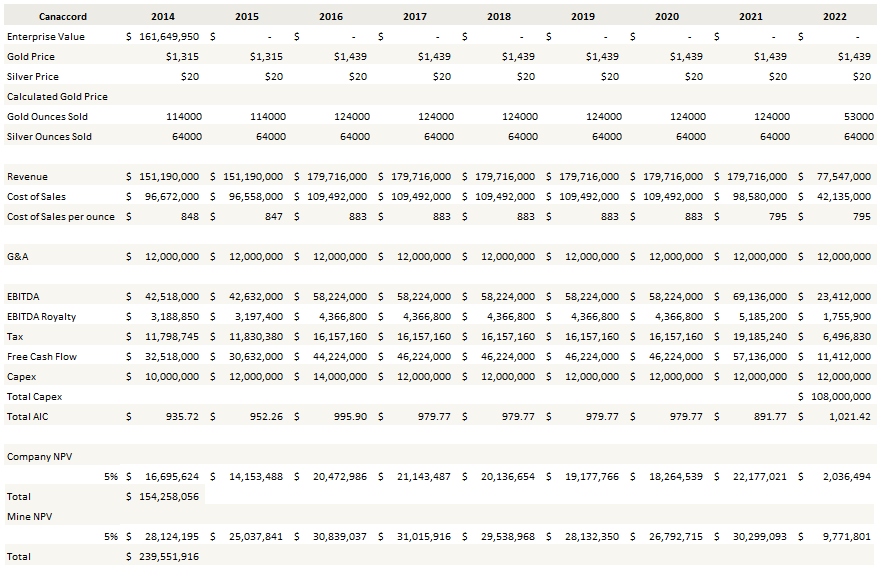

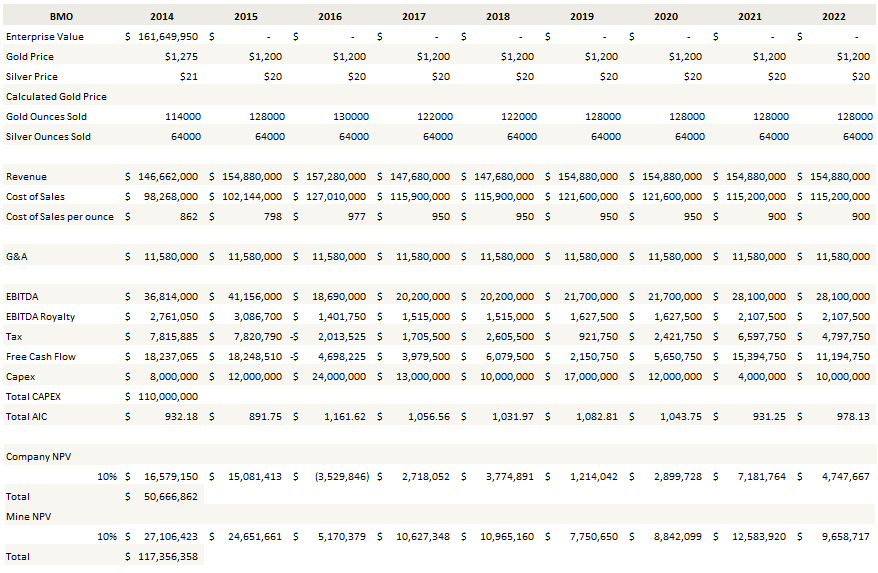

To determine how they got their numbers, I had to recreate them. I was able to come up with NPV estimates within a couple of percent of the published from each firm, while using all of the inputs they provided. Below is a comparison between my own and the published NPV’s for the San Francisco mine (not to be confused with the corporate estimates, which are significantly lower and result in the NPV’s I stated earlier).

Below are snapshots of the spreadsheets I created to replicate the results.

Below are snapshots of the spreadsheets I created to replicate the results.

Canaccord

BMO

In both cases, but particularly in the case of Canaccord, only some of their assumptions were provided in the reports. In both cases I had to fill in a number of the details based on estimates from Timmins or historical results. So no guarantee that this is an exact replica of their methodology.

Anyways, that’s what the analysts think and how they got there. If I were to describe each report in a nutshell, the Canaccord estimate is low because they are expecting 6% lower near term production then the mine plan and about $100/oz higher costs. The BMO estimate is also expecting lower near term production but the bigger effect is that they are calculating their NPV with a 10% discount and at $1200 gold.

Next I decided I should look at Timmins own estimate. Again I controlled my results against the published baseline; in this case Timmins published an NPV5, before tax, mine only estimate of $381 million and if I recreate a similar estimate in the spreadsheet I get $374 million, so pretty close. The spreadsheet is included below (note that the mine only estimate in the spreadsheet is after tax, which I think is more relevant though of course, not as big of a number):

I did the calculations at $1350/oz gold but (hopefully) you can go in there and change the numbers as you see fit (it should not save, at least according to the app instructions).

A few points about these forecasts.

- There is a significant gap between the value of the mine and the value of the company. Timmins G&A reduces NPV5 by 32%. If that kind of takeaway can be made for other single mine companies, it certainly makes an argument for consolidation.

- Timmins, and I suspect most gold producers, have share prices that fully reflect current gold prices if the valuation metric used is net asset value. It doesn’t look cheap at $1250 gold.

- The company’s valuation is extremely sensitive to discount rate and to the price of gold, both of which are “stick a thumb in the air” forecasts

- The published pre-tax mine NPV ($381mm from the news release) is a far different number than the corporate NPV, which includes corporate G&A and accounts for taxes

Most interesting though are the different stories told by the different valuation techniques. Take, on one hand, the corporate NPV calculation, which was done using the mine plan and assuming $1350 gold. On that basis the company is trading at about its net asset value discounted at 5%, or roughly at fair value if one is to assume some moderate upside to the gold price. But if we look at things another way, the company’s EBITDA in 2014 is $59 million. So on and EV/EBITDA basis the company is trading at 2.7x. Looking at it yet another way, at $1350 gold the company will generate free cash flow of $33 million in 2014, so the free cash flow yield is about 20% at the current price.

The difference, I think, comes down to an assumption of what is going to happen to the cash. Is that cash is going to sit on the balance sheet and accumulate, as is assumed when you value strictly on net asset value? Or will it be used for further productive growth, making it a sustainable cash generator. which is kind of what you are assuming when you stick an EBITDA or free cash flow multiple on the stock.

Of course gold miners have generally done a poor job with respect to cash allocations. They’ve wasted a lot of money on unproductive assets. So maybe they should not be given the benefit of the doubt. And this is gold after all, so any measure of ‘sustainability’ has to be taken with a grain of salt. I’m equally unconvinced that gold is significantly higher or lower 5 years from now than it is today.

But that is kind of the point. I have done particularly well in cases where there are multiple ways to come up with a wide range of valuations, and where the market is preferring a particularly pessimistic perspective at the moment. I find that even when the pessimism turns out to be warranted, quite a bit can happen between here and there.

So Timmins isn’t a long term hold and it’s not a large position for me. But if gold does not move lower I think there is a reasonable chance Timmins moves higher. The current price is underpinned by its NPV at $1,300 gold, and it would only take some investors to focus on free cash to give the stock some momentum to the upside. On the other hand, if the US economy is really poised to takeoff, QE to be curtailed and gold to fall precipitously, Timmins will do poorly, but I will have many other investments that will more than make up for its performance. So I added at $1.10 and we’ll see how it plays out.

I can’t edit the document automatically. I was able to save the document to my computer and then edit the variables. Thanks for the spreadsheet and the update on Timmins.

I’m not sure if you’re using a 5% discount rate but if you are that seems kind of hard to justify. A small company like this, even at todays interest rates should probably have a WACC of 8%, at the very least. I might be reading your spreadsheet wrong though and in that case I apologize.

I am. You might be right but I also see brokerages using 5%, 7% and 10%. So who is right? And does it matter? Is the stock really going to trend to some “correct” valuation? Especially a gold stock? I’m not sure about that. The point of my post was kinda to say no, that there are lots of ways you can scale the numbers up or down depending on how you want to do your valuation, what metric you want to use, etc and if you have an entry point that is leaning to the pessimistic side that probably isn’t a bad bet.

Hello,

May i ask your thoughts on this video?

thanks.

Love your blog! Recently decided myself to look into some gold miners.

So far the best option found was Pan African Resources (PAF.LON) – great cashflow (even with current gold prices), no debt, minimal forward capex, good dividend and so on. So really tempting.

What ever you decide upon just remember to not have a set price as a line drawn in the sand such as “this can not get any lower or cheaper than at this price”. I think you recall Atna and how it was such a value/growth story not that long ago closer to $1? Can you believe that puppy is now trading for …. TEN CENTS?!!!!

Glad to see how you made a killing on US equities in 2013 and largely avoided the gold space.

Its true. I am wary of having a large position in any gold stock. Timmins is a small position for me. If gold does drop to $1000, which is something many believe will happen, TMM will likely fall further.