Thoughts about my investment in New Residential’s and a look at their MSR Pools

New Residential has performed poorly over the last few weeks. Pretty much since the release of their 3rd quarter results, the stock has tumbled. As I mentioned in my previous post, I think that this move in unwarranted, and I have added to my position significantly at and below $6.

I suspect that the market is lumping in New Residential with all the other mREITs. They are being compared on standard book value metrics and New Residential trades at a significant premium to its book value (20%) while most other REITs trade at a discount to it.

I wouldn’t be surprised if there are algorithms picking up on the book value discrepancy and automatically shorting the higher price to book companies against longs on the lower ones. It would seem like a natural trade – short what is expensive, go long what is cheap, and look for opportunities where the dividend of the long exceeds that of the short.

How will the New Residential / Nationstar Relationship Evolve?

While I am not very concerned about the book value, I am somewhat nervous about what Nationstar evolves into. My biggest concern with New Residential is that Fortress spins apart Nationstar in such a way that there is competition to New Residential and/or New Residential gets left out of that structure for future deals.

I’ve listened to both the Nationstar and New Residential Q3 conference calls a few times. It’s clear that there is something in the works. Nationstar recognizes that holding MSR’s in their corporate tax structure is inefficient. They said they are evaluating alternatives. New Residential (We Edens) said that they are hoping to have some interesting news announced in this regard shortly, with the implication that New Residential will be part of that news.

I feel like New Residential is a bet on Fortress management right now. It’s a bet on their ability to create value for all their constituent companies. They’ve done this in the past. I’ve made a ton of money on Newcastle, on Nationstar, and some on Fortress themselves. So I hold onto New Residential with the expectation that they will be able to creatively add value once again.

Looking at the MSR’s

The drop in the stock and the significant increase in my position has led me to revisit the excess mortgage servicing portfolio that New Residential holds. I looked at a few things.

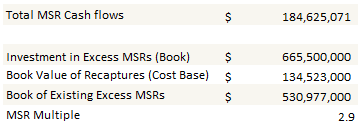

First, I looked at the cash flows generated by the portfolio and put a multiple on the book value New Residential carries it at. This cash flow multiple is how I have typically seen MSR’s talked about. To calculate the multiple I took the current unpaid principle balance, subtracted the current delinquency rate and calculated what the annual servicing fee to New Residential would be. For 3 of the pools the servicing fee is paid irrespective of delinquencies, so I ignored the delinquency rate in those cases.

In order to come up with an estimate that is consistent with typical MSR valuations, I had to subtract out a value associated with the recapture agreements that New Residential has. Nationstar has been able to recapture anywhere from 20% to 55% of the refinanced loans, and those recaptures continue to generate servicing revenue to New Residential. I thought it was reasonably conservative to hold the recapture agreements at the cost New Residential has them on the balance sheet at, with the understanding that they are likely worth more (maybe much more) because Nationstar has been exceeding the baseline recapture rates in most cases.

Below is my estimate:

I think that a 2.9x multiple is fair (PHH has their MSRs capitalized at 3.4x if you include delinquencies in the same way I did), but there is plenty of additional upside for that multiple as rates rise. I am reminded of the Lykken on Lending broadcast from last year, of which I wrote the following:

I think that a 2.9x multiple is fair (PHH has their MSRs capitalized at 3.4x if you include delinquencies in the same way I did), but there is plenty of additional upside for that multiple as rates rise. I am reminded of the Lykken on Lending broadcast from last year, of which I wrote the following:

A little over a month ago I wrote about a great discussion on the Lykken on Lending mortgage banking podcast. Lykken had Austin Tilghman and David Stephens, CEO & CFO respectfully of United Capital Markets, on the program for an interview. These fellows are industry experts in the mortgage servicing market. The discussion begins about a half hour into the podcast. Here is a particularly relevant comment from Stephens on the current state of the SRP market:

Prior to the meltdown the price paid for an SRP [servicing release premium] was generally 5x or more of the [mortgage] service fee. That multiple dropped to 4x a few years ago and we are hearing that its dropped to 0x in some cases today.

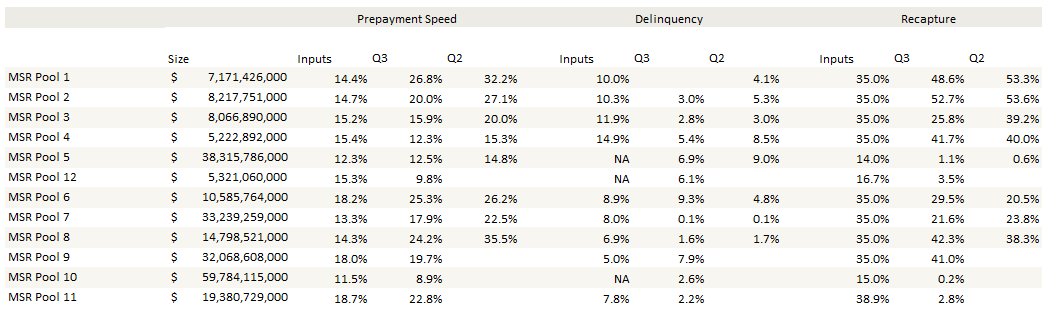

I also did some work to determine if New Residentials pools are performing up to expectations. Below are the second and third quarter numbers for total prepayments (CPR), delinquencies (CDR) and recapture rates. Keep in mind that a number of the pools were added in the first quarter or third quarter and so the recapture rates have yet to have the full impact of Nationstar servicing. In these cases it is more indicative to look at the quarter to quarter trend. The inputs columns are the baseline New Residential uses to value the MSR’s.

I really don’t see anything in the numbers or in the trends to be concerned about. On the oldest pools Nationstar is far-exceeding the baseline recapture rates. The prepayment speeds are coming down as the portfolios mature. And we have yet to see the real impact of higher interest rates; for many of these pools the weighted average coupon is in the 4-5.5% range so refinancing remains attractive.

With all of that said

As I said, my position in New Residential has become substantial, almost 20% of my portfolio (from about 4% before the post Q3 earnings drop). My cost basis is $5.97. I plan to hold through the dividend and hopefully through some sort of announcement that restructures their relationship with Nationstar. I don’t plan to hold in this size for much longer for the simple reason that it’s a bit stressful. I don’t like having so many eggs in one basket. But at the moment I believe the risk/reward is favorable so we will see if I am right.

20% of portfolio! You must be pretty confident, eh?

Any thoughts on Yellow Media? While the stock has soared I think there’s still upside left. What do you think?

Cheers.

I’m hopeful, but like I said, I am quite over-invested in this stock right now and I don’t plan to stay that way. I’m hoping that I will be able to quickly turn a lot of the position over for a profit before YE, but I will continue to hold the ~5% position until I either am proven right or wrong

Can you shed any light on how you calculate the MSR cash flows? I tried to do it using the segment reporting data (page 8 & 9 of most recent 10Q) and was coming up with a value closer to $120M.

I think we are looking at two different things. I’m not calculating income. I am calculating net MSR receipts, so the cash that comes in from holding those servicing rights. To calculate that you have to look at the UPB of each pool, ignore what is delinquent, and take the rest and calculate the cash that would be shed off from the excess MSR. Then you add up all the pools.

and at $1.5bn market cap, whats the upside?

To me the immediate upside is that I get a 17.5c dividend, maybe another 2-3c YE top-up, and hopefully a move back to the $6.50 level it was at a month ago – and I am hoping I get that in relatively short order, maybe before year end.

If I am right that the realized MSR portfolio value is going to exceed its current book substantially, and if the consumer loan portfolio does achieve the excess $200mm NPV that Edens discussed on the CC, then I think further down the road you are looking at $7-$8 – but there are a lot of ifs between here and there.

Agree… that FIG could create a competing “efficient” structure to run the MSR’s through… But they are already getting a sweet deal from NRZ to the tune of 1.5% of AUM. (which i don’t begrudge them)… Seems to me that FIG is incented to grow AUM over at NRZ. no?

Yes. I had another fellow make the same argument to me today with his inference being that FIG is going to try to play a capital raise out of this to. That might actually be the downfall of my thesis: a poorly priced capital raise. On the other hand if the capital raise is done in conjunction with a large chunk of NSM MSRs, maybe the share price rises. At the end of the day the bet on NRZ right now is on FIG creating value for all parties involved.

The management fee is to the tune of 1.5% of gross equity, calculated and payable monthly in arrears from NRZ to FIG. In addition to the management fee, there is an incentive compensation fee. Take a look at the updated registration statement…I had to read through the terms of the incentive compensation about 15 times to fully grasp what the legal language meant, in terms of the amount of money payable to FIG.

So FIG has two methods to increase fees generated by their management of NRZ: (1) Increase the value of the gross equity; and/or (2) Increase FFO/per share.

With respect to #2, I interpret the incentive compensation agreement to mean that (1) if NRZ’s achieves a return of 10% or less on book value, FIG gets nothing with respect to incentive compensation; and (2) If NRZ achieves a return greater than 10% on book value, FIG is paid 25% of the return in excess of that 10% return on book value.

So all things constant, FIG appears incentivized to increase FFO/share, which would benefit shareholders. To a lesser extent, they are also incentivized to increase the value of gross equity.

However, one of my concerns with this arrangement is the heavy emphasis on achieving a return in excess of 10% of book value. This may incentivize management to take on an inappropriate level of risk. I would rather have seen an incentive compensation agreement with a heavier emphasis on rewarding consistent increases in book value, but this does not appear to the be the case with NRZ.

I have been considering an investment in NRZ, but I am on the fence right now because of FIG’s incentives. Am I reading to much into this?

Everything you wrote is consistent with my understanding. And yeah its true, they are taking on more risk to get the extra returns, and if you think a recession is imminent then its probably not a good idea to put any money into NRZ because the consumer portfolio is going to do poorly and the MSRs are going to suffer on the defaults and the prepays. But I dont think a recession is imminent, at least in the time frame I am looking at, say the next 3m.

I tend to agree with you re NRZ, but doing more work. On the 3Q13 con call, a comment was made about having $96mn of cash – and that if that cash would have been invested at 15% for the full quarter, earnings would have been higher by $4mn or 1 c / share. 15% on $96mn is over $14mn – or closer 5 c / share. Any idea where the missing $10mn is??

I think you annualizing it aren’t you?

One more comment for you – re the multiple of cash flows these MSRs are being valued at. I’m not convinced you should be reducing the MSR carrying value the way you are (related to recapture agreements). I believe the BV of the asset (~$667mn) already reflects recapture assumptions. I’m also not sure how you arrived at your cash flows from MSRs. I think the easy way to look at it is $35mn of cash flow from MSRs in 3Q13 (see slide 10 bullet points) – which annualizes to $140mn. $667/$140mn = 4.76x. That’s still a 21% return – which is higher than the expected lifetime yield of 16% on p. 6 for a variety of reasons. But certainly NRZ isn’t making a 33% return on these MSRs. That doesn’t mean the stock isn’t a buy, however, I think it is. Issue is that the WA life of many of the company’s investments is only a few years – so in a way it has the same problem the MREITs have – the market doesn’t believe it will be able to replicate these returns (and therefore, its dividend) over a long period of time. NRZ should do a better job at that than the MREITs over the next few years, however, which is why the stock is trading at a premium to book. Question is, how does company replicate these returns in 4 or 5 years… If you amortize the premium to book over the next few years on the assumption that the returns won’t be replicated, you’ll get to a dividend yield closer to 8% or so. Just one way to look at it.

In my calculation, as I wrote in the post I subtracted the recapture part of book (at cost basis) from the MSR book before calculating a multiple. You have to do that in order to have an apples to apples comparison to typical MSR valuations. Applying a multiple to a book value that includes some value associated with recapture doesn’t seem to be consistent with the methodology used to value MSRs, or at least my understanding of it.

My total cash intake from the MSRs on the books at end of Q was $184mm annualized. I can’t break out why the $35mm number annualized is less than that but a lot of closing happened in Q3: Pool 12 closed in Sept, Pools 7,9,10 weren’t fully funded until into Q3, there was an additional 10% investment in Pool 10 in Sept, and Pools 3,4,5 closed June 29th so maybe Q3 cash flows don’t reflect full cash from those pools either. But to get the $184mm number is pretty straightforward, just take UPB less delinquencies and multiple by WI and by MSR.

Nice call on NRZ and the transaction you expected has now been announced.

http://finance.yahoo.com/news/residential-announces-acquisition-mortgage-servicing-122000462.html

I am still confused on your MSR picks and why you decided to exit PHH. Was that exit just to add to the NRZ and CHMI positions? I still like PHH but wondering if you saw anything else there that gave you reason to get out.

Sorry for the slow reply. I guess I had gotten into the stock because I hoped for a spin-off of the MSR and Fleet business and when that didn’t happen I exited. But you are right, another consideration was that I was pretty long NRZ at the time, as well as having a position in CHMI, and it was just a little too heavily weighted to that MSR end. PHH also has the head-wind of originations, while the other two do not.

Thanks, that makes sense. I completely overlooked originations, although I am sticking with PHH because even with the headwind, it is too cheap to ignore.