An LNG Venture: Macro Enterprises

Back in the summer I bought a company called Entrec whose business was to provides large cranes and heavy load transport services. My purchase was based on the thesis that there would be increased demand for these kind of services as the liquefied natural gas terminals began to be built along the BC coast.

Well I still believe that this thesis plays out over the next couple of years and Macro Enterprises (MCR) is my second endeavor under its umbrella. Macro provides pipeline and facilities construction services in Northern Alberta and British Columbia.

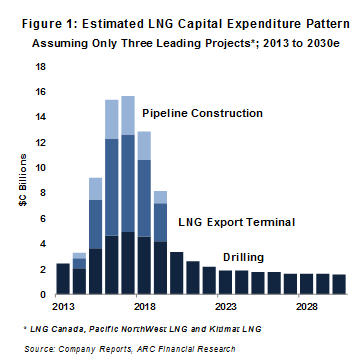

Macro should benefit from the construction of the LNG facilities anticipated over the next few years. There were a couple of good articles written by ARC Energy’s Peter Terzakian with respect to the opportunity presented by LNG development (here and here). Terzakian quantified the magnitude of the impact of LNG spending as follows:

If three projects get the green light, the implied wave of capital crests at $16 billion per year in 2017. Let’s consider some comparative perspectives. Spending by oil and gas companies in BC is typically only $6 billion a year, so the magnitude of what’s to come could be nearly triple at the peak. How about the speed of the wave? What happened during Alberta’s early oil sands development provides a comparative vignette: Three LNG projects will generate a steeper spending swell than what the Fort McMurray area experienced a decade ago.

The following graph, provided in the first article, illustrates the concept graphically:

Macro is a really simple business. They win projects to build pipelines and related infrastructure, they execute on those projects by building said infrastructure, and they generate a reasonable margin in the process.

While it’s unlikely that Macro will get any contracts directly associated with the LNG facilities themselves, there should be plenty of infrastructure like compressor stations, fractionation plants, gathering systems and all the other peripheral infrastructure needed to bring the LNG to market. The company is well respected and competitive so I would expect them to do well and win their shares of bids.

As we wait for the LNG projects to be approved and begin awarding contract, Macro will depend mostly on Fort MacMurray project work. Because their revenue is project dependent, and because they work on a few large projects at a time (in the third quarter most of their revenue was generated from 5 projects) their revenue can be lumpy. So depending on how the next few quarters go for contract wins, the stock may fluctuate up or down. In the third quarter MD&A the company guided towards an okay but not great fourth quarter, saying that until some of the LNG projects are approved work in North East BC is expected to be weak.

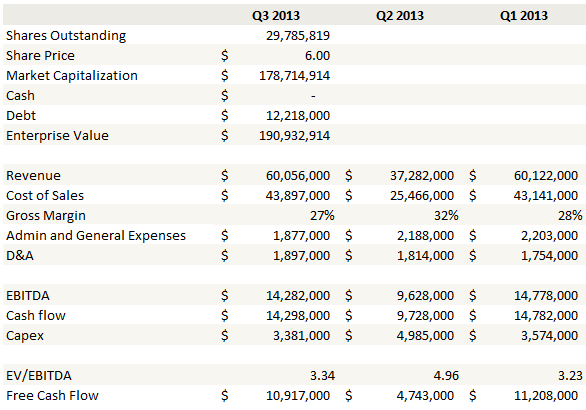

The stock is pretty cheap based on its recent business level which is really why I’m not hesitating to buy it here even with some near-term headwinds. Below is a table of the EV/EBITDA of the last few quarters.

So you aren’t paying up for that growth which I would expect to be associated with the development of a few LNG projects.

But it’s a tough business and I’m not going to get carried away. I have invested in these engineering and construction service companies before. I did very well on a little company named Steeplejack and another larger one named Flint back about 7-8 years ago. I learned that while the tide is high these companies can make a lot of money and, if you are lucky, the excitement will build, a few takeovers will occur, and some decent multiples start to be slapped on the stocks. But when the tide goes out you have the same number of companies competing for a much smaller universe of business, which leads to plunging margins and breaking even at best. Its best to take the profits while they be had.

Fortunately I don’t think we are anywhere near that point. When the LNG projects begin to ramp up we should start to see the kind of positive momentum I am talking about. I don’t even think that game has started.

So I’ll wait and hold this one hoping for a few large projects that change the game. To conclude, I will leave you with the last slide of their presentation, and what might be one of the most boring concluding outlook slides that I have come across.

Go team.

Go team.

Are these projects really a slam dunk to get approved? What about the environmental and first nation oppositions? What if prices in Asia is lower (they get the same technology or supply from elsewhere) by the time these terminals get built. I guess that’s more of a problem for Shell, but still.

No I don’t think they are a slam dunk. This isn’t oil though, these are natural gas pipelines that are being proposed. But I think the bigger point is that nothing like a slam dunk is priced into the stock here. Its trading at a reasonable to low multiple based on work that has zero contribution from LNG. So its all upside potential.

Fair point. Better hope the tide arrives though. These types of companies just tread water otherwise. It might be too late then, but I would wait until the boom shows up in one quarter before jumping in. If you’re right then there should be a few years of runway here. Just my 2 cents.

What do you maie of mcr now. Any chance it sees new highs within the next 12 months? Really been hard in 2014.