Tracing out Nordion

I’m going to start this post with a short summary of why I took a position in Nordion. I tweeted the following at the beginning of January after establishing a position in the stock.

As I briefly explain in the tweet, Nordion has about $323mm of cash and another $40mm of restricted cash on their balance sheet. They have $41 million of debt. There are 61.9 million of shares outstanding. I bought the stock at a little over $10, so at an enterprise value of a little under $300 million.

What they do

The company is involved in two related businesses. They sell systems that use radiation techniques to sterilize medical devices and foods, and they process medical isotopes for the diagnosis and treatment of diseases.

It is the isotope business that has presented a problem for the company and been the cause for the stocks poor performance over the past few years. Nordion supplies molybdenum-99 (Mo-99), which is the source of the isotope technetium-99 (Tc-99, (the isomer that Mo-99 decays into that is ultimately used in the diagnostic imaging procedures) that is used in a number of medical imaging procedures. Wikipedia has as good of a summary as anywhere on the usage and production of both Mo-99 and Tc-99).

To create Mo-99 you need highly enriched uranium that necessarily comes from a nuclear reactor. Nordion has had a long standing relationship to purchase the raw Mo-99, which they then purify and distribute, from the National Research Universal (NRU) reactor outside of Ottawa. But the NRU reactor is very old and has been scheduled to go off-line in 2016. Noridion is actively looking for another reactor source but they have yet to announce anything significant.

If the NRU reactor goes off-line in 2016 and Nordion does not have a second source of the raw Mo-99, the isotope business would be finished. I think the market has been discounting the stock to a level that basically assumes this is a foregone conclusion. If you look at the sterilization segment, which would be the remaining business if the isotope segment ceased to exist, the current enterprise value of the company trades at 9.5x EV/EBITDA. The segment has been a very consistent, albeit slow growing business with the stability to justify a 10x multiple. The company guided positively for the sterilization segment in 2014, setting an expectation of a 10% improvement in revenues over 2013.

(Note that the company expects an impressive 30-40% revenue up-tick from reactor isotopes in 2014. Reactor isotopes make up 70% of the overall isotope business. So earnings from isotopes in 2014 will also be up significantly from this year.)

I think that at the price I bought the stock, and even at today’s price which is 10% higher, you are getting the isotope business, if not for free, then at least at a significant discount. Which begs the question, is the isotope business really dead in the water?

I’m not so sure.

Nordion and Mo-99 Production post-2016

Its not 100% clear to me that the NRU reactor just shuts down in 2016 with nothing firm yet in-line to take its place. If I were a newsletter writer I would have titled this section “The Coming Mo-99 Crisis”. I’ve spent a fair bit of time researching the outlook for Mo-99 production and its not a pretty picture.

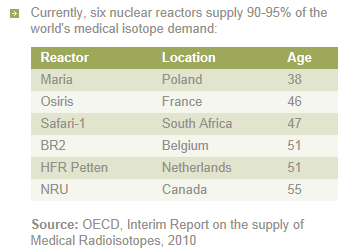

The NRU reactor currently supplies somewhere in the neighborhood of 30-40% of Mo-99 supply. In fact, there are only 5 reactors in the world that supply Mo-99. These reactors are all very old.

Most reactors are not equipped to produce Mo-99 and it doesn’t appear that it is a simple process to retrofit reactors to equip them to produce Mo-99. Moreover, because the process requires access to highly enriched uranium, the same stuff used to make a nuclear weapon, you have to be very careful about who is doing the isotope making.

While there are efforts to produce Mo-99 by other means, as of yet there is no sure fire process to take the place of reactors like NRU. I would recommend reading this paper. It gives a historical perspective and state of the union for the Mo-99 market, as well an outlook of the runway to the 2016 shutdown. While the purpose of the paper is to discuss how to create incentives that entice private enterprise to build alternate facilities for creating Mo-99 from low-enriched uranium (which wouldn’t require a reactor), you can’t help but read between the lines that the real story is how unlikely it is that even a significant portion of the NRU production is replaced in time for the 2016 shutdown. While a couple of facilities have passed the design stage and some approvals, the process is onerous with the added complication that the low-enriched uranium product will require more post-processing by the Radiopharmeutical manufacturers that take the Mo-99 and turn it into the Tc-99 that is ultimately used in the diagnostic procedures.

So it appears unlikely that there will be a way of replacing the Mo-99 production from the NRU by 2016. Yet Mo-99 and Tc-99 are absolutely essential to the medical industry. From what I can tell there is no easy substitute.

Its a tricky situation and the Canadian government is aware of it. In this paper the government discusses the impact of the shut-down of the NRU. And for background on the history of Mo-99 production at NRU and some of the

I’m not sure how this plays out, but a number of the scenarios are positive. First, if there aren’t sufficient viable alternatives for Mo-99 by 2016 the Canadian government may be forced to extend the life of the NRU reactor. Second, Nordion may be able to find another reactor source (potentially from Russia, as the company has had discussions in the past with securing a Russian supply, though there has been almost no information on the progress of this recently) and continue with isotope production at at least some level.

Also possible is that Nordion develops a relationship to develop Mo-99 from altnerative low-enriched uranium. I note that Nordion is a commercial partner with TRIUMF, which is a national labratory that was recently given a grant from the Canadian government “to develop new sources of supply of the key medical isotope, technetium-99m (Tc-99m).” They would be producing the isotope via a particle accelerator. I note the following news release from TRIUMF:

TRIUMF is developing a new “Made in Canada” technology in partnership with MDS Nordion that uses accelerator-driven photo-fission and non-weapons-grade uranium to produce Mo-99 in a manner that easily integrates with the existing supply chain. A technical demonstration is scheduled for 2012 with pilot commercial production by a third-party technology licensee expected by 2015. Such an accelerator system producing sufficient Mo-99 for Canada’s domestic needs would cost $50 million to design and build.

Note that in 2012 TRIUMF did successfully demonstrate that they could produce Mo-99.

The negative outcome is that the NRU shuts-down in 2016 and whatever solution or non-solution that exists at the time excludes Nordion. In this case you still get 3 more cash generating years from the isotope business and a stock that currently doesn’t price in the extended production anyways. It doesn’t seem to me like a lot of downside risk to participate in a play that holds a lot of upside if one of the first two scenarios comes to fruition.

What I’m Doing

I’ve taken a starter position in Nordion and am watching the developments closely. I am probably one of only a handful of people on the planet that have a Google Alert for molybdenum-99. The key for an increased position will be some clarity on Mo-99 production post-2016 and Nordion participation in it. The stock is a decent risk/reward on some sort of positive outcome.

You have had tremendous success in your thrift conversion strategy. Have the ones that you own run their course or is there still upside? Also, are you looking at adding any additional thirft conversion to your portfolio? This si a great webiste by the way.

I have a number of banks in my portfolio still, some of them are former thrift conversions. They are: ACFC, CLBH, EVBS, MNRK, NWYF, OSBC, PKBK, SBFG, SFBC

Hi Lsigurd,

Interesting post. As a fellow Canadian I like that you cover Canadian companies!

I’m just wondering as to how you estimated EBITDA for this section of the company.

My estimate came from Note 25 (segmented information). If you take the sterilization segment earnings (35,309), added back in depreciation/amortization (3,746), then subtracted a weighted average of the Corporate and Other section (based on the earnings of the three sections). So given that sterilization technologies contributed ~55% (35,309/64,215), you could subtract 55% * 11,979 (6588). This gives an EBITDA estimate of 32,467, which seems to be roughly around what you’ve estimated.

Thanks!

Thanks for this post. I bought NDZ this morning, 2014-03-04, before stumbling on your post. I too will add a Google Alert for molybdenum-99.