Terra Energy as a bet on gas

I remember back in 2009 when I had a broker recommend Terra Energy (TT) to me. He thought it was a great play on an improving economy and what was known to be infinite demand for natural gas.

I didn’t quite see it that way and I passed on the opportunity. Soon after that I passed on the broker. AECO gas prices were well above $5/mcf at the time (I wouldn’t be surprised if the number was closer to $7 or $8) and I figured there was no way gas prices could stay up there. The stock was at around $1.50.

Fast forward a few years and I bought the stock about a month ago between 28-30c. As usual I am slow getting around to a write-up and unfortunately the price has increased somewhat in that time. Nevertheless, even at the current price I think Terra represents a good risk/reward with the main element of that risk/reward being the future price of natural gas.

Why did I buy Terra?

Here’s the short story on Terra. At the current price the stock has an enterprise value of a little over $50 million. Based on Q3 production they are trading at $14,000 per flowing boe. They have a huge land position of 350,000 acres scattered all over Northern Alberta and Northwest British Columbia.

The company came out with 2014 guidance last week and if they achieve those numbers they would be trading at a little over $11,000 per flowing boe at year end. They also guided to $21 million of cash flow from operations, which would put cash flow per share at 21c. They expect liquids production to increase to 39% by the end of the year.

The main problem with Terra is that they have been heavily gas weighted. 84% of Terra’s production in the third quarter was natural gas. Because all of their production is in Canada, they have been seeing extremely low gas prices. The realized price per MCF in Q3 was $2.62. Four of the last quarters their realized natural gas price has averaged under $3/mcf.

A second problem has been that the company was over-levered given the cash flow generated by their gas assets, so the investment community shunned them. The company began 2013 with over $100 million of debt. However in the summer the company announced agreements (here and here) to sell their Montney assets for about $80 million. What was particularly interesting abut the disposition is that they sold almost none of their producing lands.

Its still all about the gas

The company has recently began to make overtures about getting more oily but to me this is ultimately a play on natural gas. I think there is a reasonable chance that we could end up with year-end storage below 1tcf. While the natural gas futures curve is so far not suggesting that storage is a concern, I think there is may change over the next few months. I don’t think we will see the pick up in drilling required to fill a 1tcf end of heating season storage without some move up in prices.

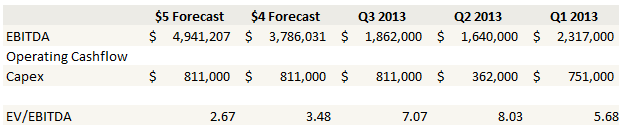

Even if this doesn’t happen, I think Terra will do well simply because the current AECO strip is much higher than it has been in the last two years. Spot AECO gas is over $5 today, and the 12-month strip is over $4. I looked at the $4 and $5 scenarios and came up with the following quarterly EBITDA forecasts for Terra.

But there is oil upside

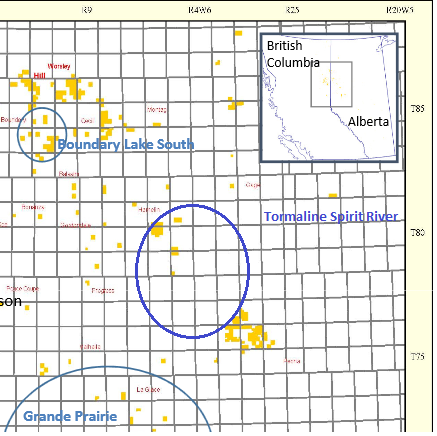

While Terra started out for me as a pure play on natural gas prices, there was some excellent work on the Investorvillage $PEAK board that highlighted how the company actually owns some prospective oil acreage around Tourmaline’s Charlie Lake oil play and the Doig in northwest BC .

According to Sculpin2, a poster on the site that I have followed and invested with on many occasions in the past and whom I have a great deal of respect for, Terra owns land within the core area defined by Tourmaline as well as much more land to the north of the play. Sculpin provided a description of the play in this post, including the following excerpt (my underline):

An overview of operations to date. At Spirit River, in the Peace River Arch, TOU has been chasing Triassic Charlie Lake oil since late 2011. To date the company has drilled >40 wells of which ~25 wells are tied-in. Recent drilling has proven a significant expansion of the original pool to almost double the size in term of inventory (200+ horizontal locations vs. prior 100 locations). A notable southern step-out well (14-8) was drilled in Q1. The well tested at ~1,300 bbl/d, was placed on production mid-March and has since produced 105mboe (53% oil) with current rates >300bbl/d. Major expansion in the Triassic Charlie Lake fairway. Earlier today TOU announced a major expansion of its acreage position in the broader fairway. Over the past 18 months TOU’s exploration team has assembled >400 sections (up from ~100 total section last September) prospective for Charlie Lake oil with estimated exposure to >500mmboe of recoverable light oil and natural gas (internal management estimate). We highlighted the new land and activity in the map found in the Appendix. The exploration fairway extends across 75 miles. We are very encouraged by a short-term test of 700 boe/d 40 miles north of the main pool.

I did some work to delineate Tormaline’s core position at Spirit River versus the land maps provided by Terra. The original Charlie Lake discoveries were to the southeast, or just west of Terra’s large acreage position (in yellow).

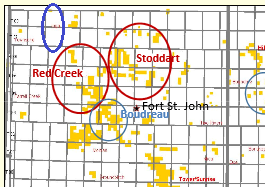

As for the Doig play, more great scuttle from Sculpin in this post. He thinks Terra has around 6 sections, or ~3800acres, northeast of the wells Artek and Kelt have been drilling. The excerpt below is taken from a Cormark report on Artek’s work in the area.

The 10-17-87-23W6. well was into the Doig where a previous step-out well one section over encountered thick Doig sands with high NGL rates. This latest Doig horizontal test flowed over 135 hours (5.5 days) and during the last 24 hours flowed up production tubing at a rate of 4.2 MMcf/d (including 9% propane load fluid) and 1,003 B/d of condensate, or a combined 1,639 BOE/d net of load.

This latest well confirms the technical work that determined the south Inga block to contain higher NGL yields than in the north. The 13-16 Doig step-out well produced over its first 30 days at a restricted rate of ~1,200 BOE/, of which 53% was liquids, versus this latest one at 10-17 which has a 61% liquids yield. Note that the 13-16 well tested at equally strong rates (1,762 BOE/d net of load, 70% liquids); as such we believe that the 10-17 well can have IP30 rates of at least 1,200 BOE/d.

Below, I have reproduced a close-up of where Terra’s land (yellow) is with respect to where Artek and Kelt are drilling the Doig play (the blue circle). Terra owns a lot of land to the south and east of the play.

Finally, I haven’t done any research on it yet, but Terra apparently holds a fair sized Duvernay position. While those wells are going to be expensive to drill, any news about a joint venture or possible sale could be another positive catalyst.

Conclusion

Terra has done a lot to improve their balance sheet. They only have $18mm of debt versus $100+ million before the sale of the Montney assets. Removal of the Montney assets significantly reduced debt but did not impact production at all. With the removal of the debt they are extremely cheap on pretty much any metric (per flowing boe, net asset value, price to cash flow) if, and this is the if, you believe their gassy Canadian assets can be profitable. And that profitability is all about the price of natural gas, which I think is going to at least stay at these levels through the summer, with the possibility it goes higher.

At $4 gas I think Terra can generate nearly $4mm of EBITDA per quarter. If the company was regarded as a legitimate concern they would begin to receive a fair multiple. A 6x multiple on that would put the stock at 70c.

So that is a fair upside. But I’m not getting carried away thinking the good-old days are back and looking for a $1+ stock price. For that you would need to see the kind of gas prices we saw pre-2007 – and I’m not so bullish as to think that is going to happen. Plays like the Marcellus and Utica are for real. But in the short to medium term I think that production lags what it needs to be, and Terra’s stock price should see benefit from that.

Great write-up! What I find most encouraging from the Feb presentation is the chart showing monthly operating income hitting $3MM per month at the end of 2014. This is with the assumption that oil will be around $86 and NG at $3.80 or so. If they can hedge both oil >$95 and NG over $4.50 we could see op income on an annualized basis over $40 million.

My valuation target for Terra is as follows:

What would it be worth if they hit these numbers? $35K per boed less $25MM debt. This would put the shares at $1.44 by December vs the current $0.36. This puts it in line with the Company’s current 2P NAV. Further upside would come from land sales, JV’s and any acceleration in drilling with higher cash flows.

in the same neighborhood, have you ever gone over the Peyto story?

No I have never looked at it in depth as I’m usually a small cap value investor. My largest micro cap E&P positions are Yangarra (TSXV -YGR), Marquee (MQL – TSXV) and Terra Energy.

can you also re look at Niko resources? Recent developments as you might already know:

1. The Gas pricing is set to more than double and is for real.

2. Management took a strategic decision to focus on Indian and Bangladeshi assets and stop wasting money on other assets. Infact they are looking to farmout or sell those assets.

3. One of the issue though is they have further diluted the equity.

SP also looks have formed a base and also on rise from couple months now.

What do you think about Terra now at this environment? Obviously, it has touch quarters ahead. Do you think that it can survive through the rainy days?

I honestly haven’t looked at Terra in over a year so I can’t comment specifically. I still can’t be very positive on ng though, the production levels are so high. I want to catch the turn on ng when it happens but it doesn’t seem like we are there yet.