Week 141: Portfolio Allocation

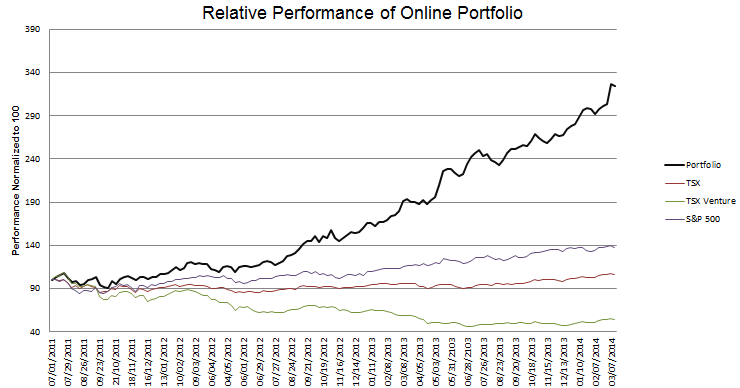

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

I’ve been on vacation and so am a couple weeks late getting an update out.

My portfolio had a big move up, thanks mostly to the movement of Pacific Ethanol and MagicJack. Pacific Ethanol had a one day gain of 67% last Thursday, and is nearly a 4-bagger since I bought in. MagicJack is nearly a double.

But what has really helped is that even before the run-up Pacific Ethanol was my largest position. MagicJack was my fourth largest position.

One of the ironies of writing about the stocks I own, is that what I write about most is often not what I have the biggest position in. The stocks I have the most to say about are the one’s that are on the cusp, where I am constantly debating whether to hold on to them or not. My biggest positions; Pacific Ethanol, Yellow Media and MagicJack, for example, I have written only a single post about. That post states the thesis, and as long as that thesis is valid I don’t have much else to say.

Yet the stocks in my portfolio are far from being of equal weighting. I usually have a lot of stocks. Unless the market is going down, the stocks number at least 30 and has recently approached 40. But most of the positions are quite small, in the 1-2% range. These as starter positions; enough to keep me interested and following the company, but not enough to hurt me too much. If my thesis for these companies plays out, or if, as I learn more I become more comfortable with the idea, I add. If not, if the company materially lags or sometimes if time simply passes and I lose interest in the idea, I drop the position and move on.

There are only a few stocks that take a heavy weighting my portfolio. And those few can be very over-weighted. I am not afraid of taking a very large position in a stock if I think the rewards far outweigh the risk.

This was the case late last year when I briefly had about 20% of my portfolio in New Residential. Before that at various times during 2013 I had made similar but not quite as large a bets on YRC Worldwide, Gastar, IDT, MBIA, Yellow Media and unfortunately, Niko Resources.

I took a similar sized position with Pacific Ethanol. Going into the fourth quarter results it seemed unlikely to me that the company would deliver anything other than an eye-popping earnings per share number. I made the stock an 8% position heading into earnings, including leverage from some options.

It was a favorable result. The stock is nearly a 16% position for me right now.

I think its important pillar of my strategy to take advantage of the concentration that I can have. I don’t have anyone pressuring me to be diversified or questioning my risk level or anyone to answer to if something goes wrong. So I don’t hesitate to have a large percentage of my portfolio tied to the names I think will perform the best.

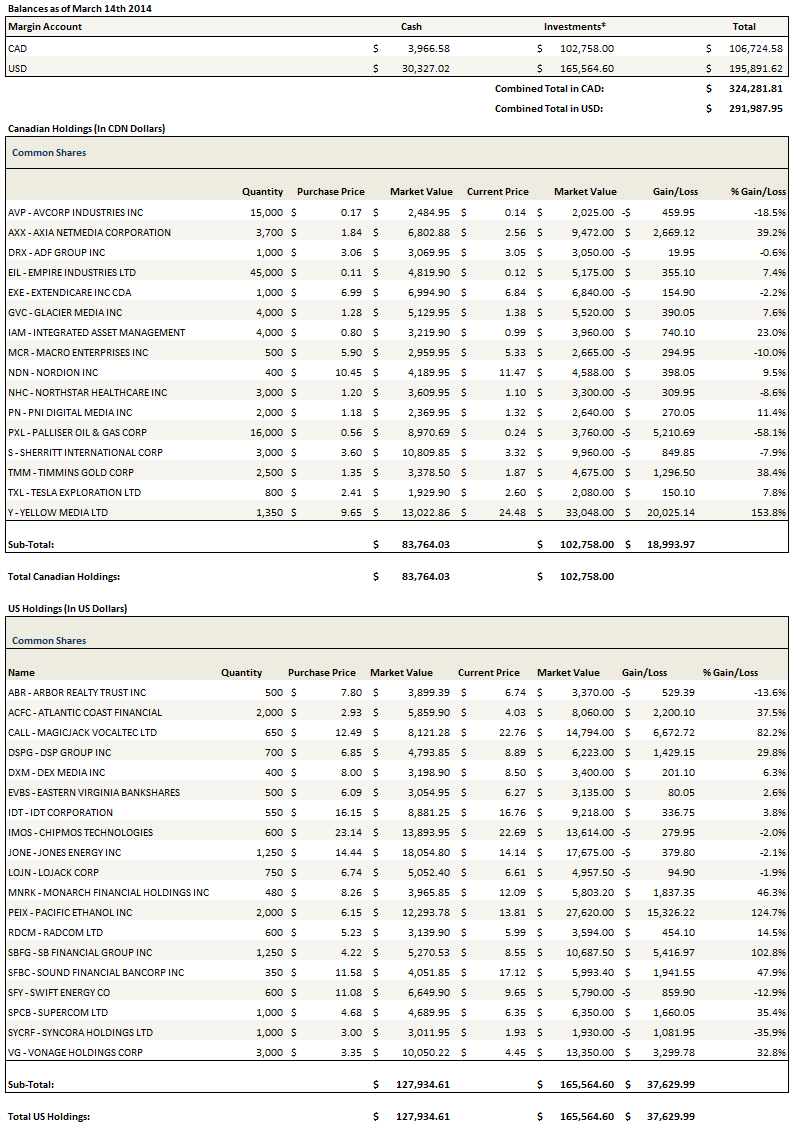

With that said, the names that I am currently of the heaviest weight are, of course, Pacific Ethanol, which remains my largest position by far (the weighting in the on-line portfolio I track here actually understates my true exposure as I have not always been diligent in matching my purchases); MagicJack, which has remained roughly the same size over the past few months; Sherritt, a position which I reduced after earnings but have subsequently added to as the price of nickel has risen; Jones Energy, which I have added to as the price has fallen; and Extendicare, for which I seem to be forever waiting for the end of their strategic review, but am picking up a 7% dividend in the mean time, which helps me keep my interest.

Note: Its worth noting that while I was going through this reconciliation of my larger positions, I did notice a few discrepancies (in addition to what I already mentioned with Pacific Ethanol) where the on-line portfolio doesn’t truly reflect my actual holdings. First, I own a larger percentage of Extendicare and MagicJack than is currently represented in the on-line holdings. My holdings in Extendicare are nearly double what it they are represented here, while MagicJack is 40% higher. Second, my on-line position in Vonage and ChipMos are too high. My position in Vonage is about half the size that is reflect there while Chipmos is about 2/3. From time to time I have to reconcile the practice account I use to track my portfolio with what I actually own because it tends to get out of sync. I think I will have to do that again soon.

A final note before going on to specific names. I have been reducing my overall exposure to stocks over the past few weeks. I’m about 10% cash right now. I expect to go more to cash over the next few weeks. No specific concern is responsible for my caution, just recognition that the market has risen a lot and the economy still has many weak links.

I made a few portfolio moves over the last few weeks.

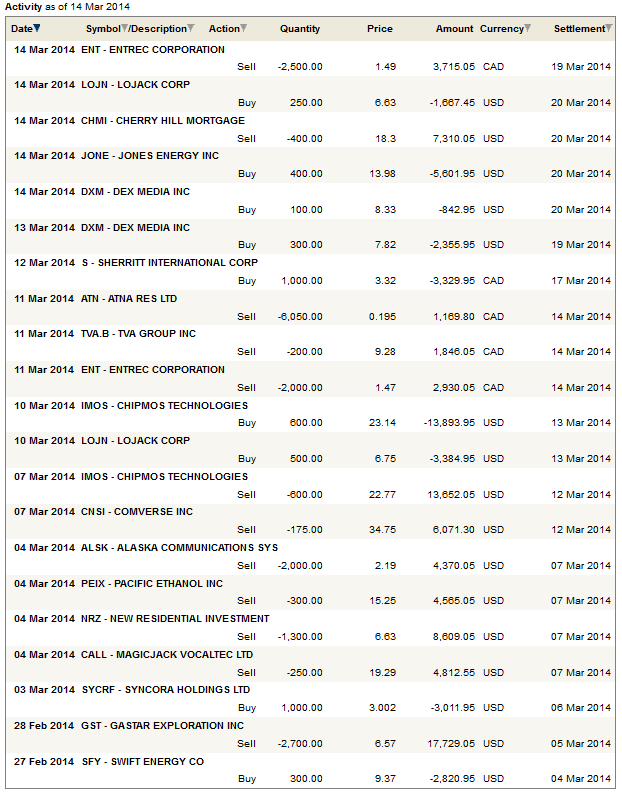

No More Gastar (GST)

First, I sold out of Gastar. Gastar’s been a great winner for me, I’ve watched it run up from $2 to $6 over the last 10 months. Recently however I tweeted about my skepticism of their Hunton play. The more I researched the play the more it appeared that what they had were a number of easily identifiable (through seismic) pods that they could exploit for some early big wells, but that repeating that performance over the entire acreage would be difficult. From what I understand, the Hunton isn’t the Eagleford or the Marcellus; its not the kind of formation you can cookie cutter drill at a fixed spacing and expect consistent results. On top of that, the company has moved south with their drilling, and those wells, while costing less, are also going to be less prolific with their IPs. I haven’t reviewed the company’s Q4 results that were released Friday, but the stocks performance suggests I might be onto something.

Sold out of Comverse (CNSI) and Entrec (ENT)

Second were a number of sales that reflect, as much as anything, moves to redeploy cash to other ideas. I sold out of Comverse for a decent 23% gain for me in a little less than a year, and out of Entrec which had a negligible gain. Both of these stocks represent potential opportunities where I’m just not clear enough on the outcome. Will Comverse hit their eventual margin targets? They might, they are making progress, but there is more risk built into the stock here at a price that is 20% higher than I bought it. Entrec may be a long-term winner but as some of the commenter’s noted when I first bought the stock, I was too early. I probably will miss this play entirely, because you have to sit around and wait until the LNG projects are not yet announced but will be so imminently. That’s a tough window to catch.

Out of Servicing Plays (in the tracked portfolio)

I also removed my two mortgage servicing plays, New Residential and Cherry Hill Mortgage, from the portfolio. But that should not be confused with me being out of these names entirely. I track one portfolio with what I post on-line, and that portfolio tends to be the most speculative and aggressive one. It is also the most fun to write about. I exited these names here to chase other ideas. I still own significant amounts of both in less aggressive, income oriented accounts. I should note that removing REITs also helps my performance here; the RBC practice account I use does nothing to track dividends, so over the last couple of years I have had zero performance from the dividends paid by the REITs and other dividend paying stocks I own.

Out of Alaska

Finally I removed Alaska Communications. I sold this stock back in mid-January at around $2.40 because I was happy with the gains I had. I forgot to sell it in the on-line portfolio until I noticed it in March, so I ended up with a 10% gain instead of 20%.

I also added a couple of names.

Added Lojack Corp (LOJN)

First, I added a new position in Lojack. I’ve been following Lojack for a while but hadn’t pulled the trigger until after reviewing the fourth quarter earnings. Its unfortunate that I have been so busy lately; I could have bought the stock at just over $5 after earnings if I had been able to get to the results sooner.

Lojack sells installed stolen vehicle recovery systems, mostly through an extensive dealer network that sells the device in 28 states and 30 countries. Basically its a device that allows you to locate a care if its been stolen. The fourth quarter were very good for Lojack and suggests to me that the company has turned the corner on this business. Based on the company guidance for 2014 (which may be conservative) I think the stock is probably fairly valued right now reflecting the turn-around of this business.

More interesting is the recent move the company has made into fleet management. On the conference call the company gave a glowing update on the progress of their fleet management relationship with TomTom. I think they may be onto something with significant growth here. I’m still working on putting numbers to the potential, but the market size (currently $11 billion, expected to rise to $30 billion by 2018) is large, their relationship with TomTom appears to have resulted in a solid product offering, and they should be able to leverage their existing dealer network to leverage sales and up-sell customers into buying both the Fleet management and the theft prevention devices. Like I said, the current stock price reflects the existing vehicle recovery system business, but I don’t think it gives much credit to this early stage opportunity. So I have taken a position there.

Added back Dex Media (DXM)

Second, I added Dex Media, a company I have owned before on two occasions to admittedly less than impressive results. The company had a decent first quarter with 5% growth in their digital business and showed improvement in the legacy yellow pages business, which declined at a 19% rate (versus 21% for the last few quarters). The thing about Dex Media is that the difference between a $6 stock and a $20 stock is almost a rounding error on the overall enterprise value. As I wrote back in my original piece on the company in the summer they are kind of like the ultimate store of leverage. Defining risk/reward is always tricky, but the reward here is so ridiculously large if they actually succeed and create a viable digital business that its hard not to take a position if there are a few positive signs. The short interest is also very large (its 28% of the float) so there’s that.

Adding more Pacific Ethanol (PEIX)

Though I was somewhat loath to do so given the size of my position already, I was compelled to add to Pacific Ethanol when it dipped below $13. I had sold a little of the stock when it was around $15.25 and some more at $16, but I more than added back what I sold. Even with the incredible run of the past few months I am hard pressed to find a better opportunity out there.

The key will be corn prices. I’ve spent some time trying to wrap my head around the corn market and I am of the mind that the recent rise in price is mostly technical, being compounded by the geopolitical effects of Ukraine which is a large corn producer. The year-end stocks are simply too high to justify any sustained rise in the price of corn. Even now, with the current move back to the high $4’s, there is evidence of demand destruction in the way of lower consumption by the ethanol industry and lower exports.

If corn prices stay at this level (below $5/bu) or lower, I think Pacific Ethanol will be at least a $20 stock in 6 months. If corn prices continue to rise and begin to approach the $5.50 level, I will scale back on my position.

Adding Syncora (SYCRF)

I added a small position in Syncora. This was terribly timed; I first added at $3 and a second tranche at $2.70, so both are heavily underwater. I’m still waffling about whether I simply made a mistake here or whether I want to hold on for the long term. The mistake, which I tweeted, was a misunderstanding of how their statutory balance sheet included the $400 million settlement with JP Morgan. I thought the $400 million was not included in the balance sheet (in fact it appears to say exactly that in one of the notes in the stat filing!), but it turns out that isn’t the case, as its obscurely included as an offset to losses. Needless to say, $400 million is a big swing in my valuation estimate and the stock, while still quite undervalued on an adjusted book value basis is not quite as screaming of a buy as I had originally thought.

Adding to Jones Energy (JONE)

I added to my position in Jones Energy on Friday, for reasons I have already discussed.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

Syncora likely has $250-$400 million still to come from Greenpoint/Lehman.

I did know that but thanks. Hope it brings along step change in price again.