What to do with Pacific Ethanol

Being invested in Pacific Ethanol (PEIX) is like riding a yo-yo. Up and down, up and down. It can get a bit nauseating.

As I tweeted earlier this week, I got tired of the motion sickness and reduced my position in Pacific Ethanol considerably.

I dont love this higher ethanol / higher corn prices dynamic. High margins but not sustainable. Rather see low corn, lower ethanol

— L.Sigurd (@LSigurd) April 1, 2014

Halfed my $PEIX position today. Reasons I described earlier. Been great idea for me, 3+ bagger off of avg cost since mid-Dec.

— L.Sigurd (@LSigurd) April 1, 2014

Since that time I’ve sold a bit more and it’s now about 25% of my original position. It’s still a reasonable size but its not going to hurt me (I will remind you that as of my last portfolio update, when Pacific Ethanol was at about $14, the stock was a 16% position for me. That number jumped closed to 20% as the stock rose, but now sits at about 4% with my sales last week and the current price).

As the tweet explains, I didn’t like that the stock was going up because of rising ethanol prices while at the same time corn prices were creeping higher. This wasn’t the dynamic I had invested upon. I wanted sustainable ethanol prices and low corn prices. Ethanol can’t trade at nearly a dollar above RBOB gasoline and you saw that on Wednesday when the weekly EIA statistics showed imports of ethanol. The market was suitably spooked and the price of ethanol has since tanked. More on the ethanol price dynamic in a minute, but first let’s talk about Pacific Ethanol.

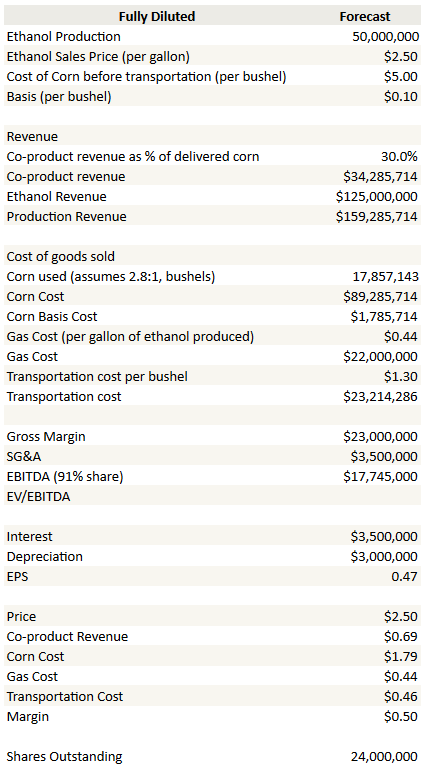

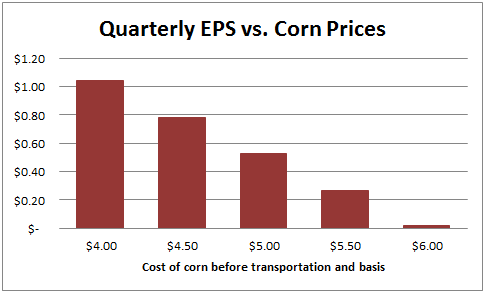

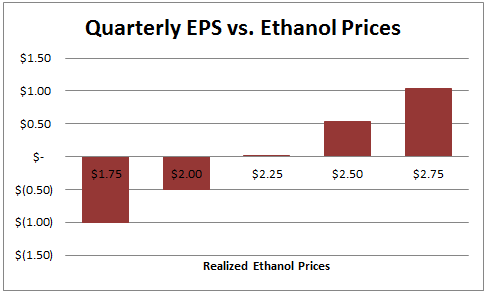

Pacific Ethanol goes up and down like a yo-yo because their bottom-line is extremely sensitive to changes in the price of corn and ethanol. I estimate that every 10 cent move in the price of ethanol creates a 20 cent fluctuation in the earnings per share. I have recreated a simple spreadsheet model below.

This is intended to be a rather generic “going forward” forecast and is not correlated to anticipated volumes or prices in any particular quarter. There’s a lot of assumptions in this model. I know that the way I’ve modeled distillers grains (and implicitly, corn oil) is simplistic. I also made some assumptions about the transportation costs and about the basis that may end up being off what is realized, particularly if rail remains tight. But I’m not intending to predict first or second quarter earnings here, I just want to give an idea of sensitivity.

Earnings are sensitive to both corn and ethanol, but not surprisingly, it’s the ethanol price that is going to make or break it for the company. Below are charts that illustrate this. The corn price chart was done assuming $2.50 per gallon ethanol, whereas the ethanol price chart was done assuming $5 per bushel corn. Both charts used the fully diluted share count before the 1.75 million offering, so around 22.2 million shares (I apologize for my laziness, I made the charts earlier in the week when I was debating whether to sell some shares, so before the offering was out).

So basically what I’m saying here is that you can come up with any EPS estimate you want depending on where you want to peg corn and ethanol prices.

The sensitivity carries over to other inputs too. For example, I assumed $1.30 per bushel transportation costs for the corn, which is at the high end of the historic range and of the range that the company provided on their third quarter conference call. But with rail traffic bottlenecks all around, its quite likely they are paying higher than that now, and again, every 10 cents on the cost side is a 20 cent reduction in EPS.

On the other hand, the ramp of corn oil technology and the use of low priced sugar for 10% of the feed stock could be having a bigger impact than one might think. On the third quarter call management said corn oil alone improved margins by 5 cents.

So what do you say about all this? Look, this company is what it is. Its a highly volatile stock and that’s because its got highly volatile earnings. So plan accordingly. Nevertheless, while I was happy to take off stock at $16 and $17 and even a little bit at $18, I am going to be less inclined to take more off at $14 and below. Because I’m not so sure that this ethanol party is over yet.

So where are ethanol prices going?

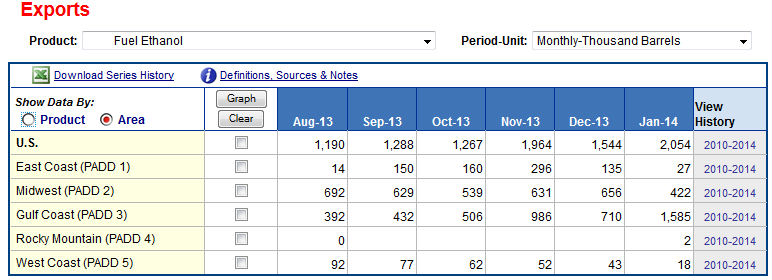

I had a really interesting letter forwarded to me on Friday. While I am not going to reproduce it, I will say that its essence, which was written by a Dallas based money manager, was that what is going on in ethanol is not strictly about rail congestion. It pointed out that ethanol exports have jumped significantly in the last few months. Below I have grabbed the data from the EIA that shows the pick-up in exports beginning in November:

While February and March data aren’t out yet we should expect more of the same.

At the current level of exports we would be hard pressed to meet our blending mandate (currently expected to be around 13 million gallons). This is exacerbated by inventories, which are at very low levels compared to the historic seasonal trend. Take a look at the following inventory chart. We should have been building inventory to over 20 million barrels at this time of year. Instead we are riding inventories down to levels that are lower than those usually experienced at the end of the summer driving season.

In March, as this situation became more critical, something had to give and that was prices, which went through the roof. While the level they peaked at was unsustainable, I’m not so sure that means they are going right back to where they have been in the past.

The main competition on the export market is Brazil, and they have two problems right now. First, their ethanol industry is awash in bankruptcies, and second, they are having a drought that is damaging the feedstock, sugar cane. So that export demand is going to stick around for a while.

Back to the letter. The suggestion was that if you wanted to shut down the export market, you couldn’t have more than a 20-30c discount to RBOB. If the discount to RBOB reached 50 cents, the export window would be wide open. That’s saying something. With RBOB a little under $3, that would put CBOT ethanol in the $2.50 – $2.70 range, which would put Pacific Ethanol’s price somewhere around $3. You can extrapolate where we are at earnings with $3 ethanol and $5 corn in the charts above.

If that becomes, in the short-term, the “sustainable” price, meaning that it can hold for at least the summer driving season, then I doubt we are finished with the Pacific Ethanol run.

Conclusion

The difficulty here is that there are a lot of if’s, not the least of which is whether the dynamic we are seeing is truly being driven as much by exports as by a temproary rail car backlog. There is also weather (its still cold through much of the country and so we’ll have to see how planting season goes off), the economy and, given the momentum attention the stock has gotten, the overall stock market sentiment.

To deal with this uncertainty I’m doing a couple of things. First, rather obviously, I’ve reduced my position to something more appropriate to the volatility. Second, I think I might try a call spread for any future shares. The idea was passed on to me by an acquaintance on twitter. It limits the downside and let’s you participate in some of the upside.

I think that some exposure remains worthwhile because, unlike the gloom I’ve been reading on message boards and elsewhere, I think we may have some upside left. I’m not so sure we are at end of days of the ethanol cycle. We might yet have a couple of more innings left.