Why I like Air Canada in two tables

I missed out on the big move in the airline companies last year because I never bothered to look at them. And the reason I never looked at them is because I have been conditioned to be skeptical about airline stocks. The mantra chimes away about high capital costs and low hurdles to entry, profits on the horizon that will be never quite there.

But things have changed and with only three major carriers in the United States (down from around 10 a decade ago) price-wars and seat sales have been replaced by full planes and higher profits.

One thing the airline industry has going for it that is rarely mentioned is that once you pass the hurdle of covering your cost, every incremental passenger is at an 80% margin (give or take, depending on the airline).

This provides a lot of leverage if things start to go well. With 5 years of improving profitability (coming off the disastrous bottom of 2008-2009) things are going well right now. The moves last year was a recognition of this.

So when I got a second chance to invest in a couple of airlines, fresh from a beat down caused by the transitory effects of the falling Canadian dollar and exacerbated by the sheer size of the moves to the upside, I added not one but two stocks to my portfolio. Both are out-sized as starter positions for me. Here were my tweets at the time:

Took position in $TRZ.B.CA. Transat AT. Integrated tour operator (ie. vacationairline). Also smaller pos in $AC.B.CA for similar reasons

— L.Sigurd (@LSigurd) March 19, 2014

$TRZ.B.CA was clobbered after Q1 miss on CDN$. Think its overdone. Company will adjust, already increasing prices. Q2 will be poor though.

— L.Sigurd (@LSigurd) March 19, 2014

I am going to talk about Air Canada here, with a hat tip to @17thStCap for raising the idea. While Air Canada was the smaller position to begin with, it kept on falling after I bought it, I added a little as it fell and then more as it went up. It is the bigger of the two now. Its also more liquid than Transat AT, which makes me sleep better with a larger position. Full disclosure, my average position cost is in the $5’s, which is where the stock was when I tweeted about it, but as usual I am somewhat late getting around to a more full discussion of my reasons.

I am going to forgo the usual summary of the business, history, competition and everything else that you probably need to review before investing in Air Canada. This is a large cap company, its covered by pretty much every broker in Canada, and so if you want all the details behind the business you can easily go to one of those sources to find them.

What I am going to do instead is focus on two reasons why I think Air Canada can go higher. These reasons can be illustrated in a couple of tables.

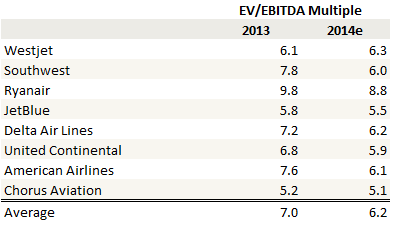

Table #1: Air Canada EV/EBITDA versus competitors

This table is a composite of last years numbers and the estimates from the three institutions that I have research access to.

Air Canada trades at a discounted multiple to its competitors. Air Canada has always traded at a discounted multiple to its competitors. I think this can change. Why? Three reasons:

- Part of the discount is because the company has been in bankruptcy once (2003) and close to it two more times (2009 and 2012), so there’s lots of suspicion that any improvement is a mirage. If those fears go away (which they will with time and success) average multiples will follow

- If the company can successfully reduce costs they can raise their margins to the level of the rest of the industry, and no longer be the high cost competitor in the space. In 2013 they succeeded in lowering costs per available seat mile (CASM) by 5-6% from 2012, so the plan isn’t just smoke and mirrors.

- Air Canada’s enterprise value has typically been discounted because they have had a huge pension liability that is going to have to be dealt with at some point. That deficit was $3.1 billion in 2012, which is not inconsequential to a company boasting an enterprise value in the $3 billion to $5 billion range over the past couple of years. However things change. Air Canada stated in their fourth quarter MD&A that the deficit had been eliminated and replaced by a small surplus. While the market tanked the stock on the news of the fourth quarter, I would argue that the pension news far-outweighed any short term currency headwinds. Without the overhang of the pension, Air Canada can be valued based on balance sheet debt (and lease arrangements, depending on how you want to run your numbers)

Even after the recent move up to $7 per share, the stock still trades at only about 4.5x EV/EBITDAR. A move to 6x, or the average forward multiple in the above table would suggest a stock price north of $15.

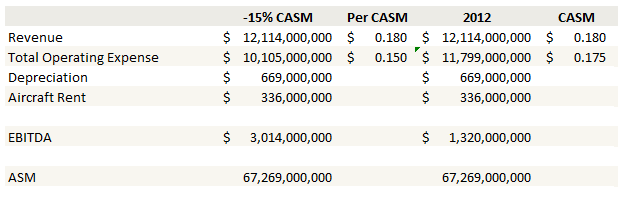

Table #2: Air Canada EBITDA before and after cost reductions

Air Canada has stated that their goal is to reduce CASM by 15% from their 2012 numbers by 2015. The table above shows you what it would mean if they can accomplish that goal.

Air Canada has stated that their goal is to reduce CASM by 15% from their 2012 numbers by 2015. The table above shows you what it would mean if they can accomplish that goal.

Obviously there are lots of other factors that could impact the actual bottom line and so this isn’t a projection. Fuel prices, revenues, and the Canadian dollar could all work against the EBITDA estimate and make it materially lower. Nevertheless the point is that there is a tremendous opportunity here if Air Canada can meet their targets and if other factors play out in a positive way.

By way of comparison, I looked at what Westjet and they currently achieve a CASM of under 14c. So Air Canada’s goal is not unreasonable.

Conclusion

As witnessed by the move up 2013 and the halving of the share price in 2014, this stock isn’t for the feint of heart. The volatility is due to the sensitivity to prevailing conditions and changes in the company’s own operating performance. Being one of the higher cost airlines means that Air Canada is particularly sensitive to swings in the industry. However, if they can reduce their cost structure, this high-cost competitor discount will disappear. And if, at the same time, the underlying conditions for the industry continue to improve, I think the stock can rally a long ways.

In particular I will be on the look-out for changes in the following important factors:

- currency stability

- further reductions in CASM

- better load factors and revenue

If these factors play out in a positive way, I would expect a gradual re-rating of the share price to something closer to what other airlines are given. And if you give Air Canada the average multiple that other airlines get, even assuming no future improvements in CASM or revenues, it presumes a decent amount of upside from here. So we shall see how it goes.

Is your thesis esssentially the same with Transat? I don’t believe Transat has the same kind of pension obligations, was that part of the reason you took a larger initial position with TRZ.B?

Yeah its pretty much the same idea. Transat got hammered a bit more by the CDN dollar though because its weighted more internationally and so that is more of a risk going forward. Also being vacation oriented makes me think its a bit more levered to the robustness of overall economic growth here. But right now, with the dollar having actually risen a bit to 91c, they might be able to pull off an upside surprise.

Any thought about American Airlines Group Inc. (AAL)?

Refer to S-4 ,as filed with the Securities and Exchange Commission on April 15, 2013 stated that EBITDAR 2014 $7,793M. current EV 27,260M. Just trade at 3.5x EV/EBITDAR .(http://www.sec.gov/Archives/edgar/data/6201/000119312513155207/d486518ds4.htm)

In addition Doug Parker, CEO Short-term Incentive Pay: For 2014, my short-term incentive target payment is 200% of my base salary. But I will only receive a target payment if American Airlines earns $2.5 billion in pre-tax profit in 2014 – far more than American has ever earned in its history. (http://www.sec.gov/Archives/edgar/data/6201/000119312514022363/d665075dex991.htm)

Creditor will be the Major shareholder and likely to sell regardless the fundamental aspect of company. Share will start distribute to creditor within 120 days on Dis 9, 2013.

Hence, share price will substantially higher after April 2014

Thanks for the info. I’ve been intending to take a closer look so that info will help.