More Quarterly Results: Sherritt Thesis Intact

I’ve owned Sherritt International since January, when I posted about the idea here. The timing of my stock purchase coincided with the start of the Indonesian export ban on ferrous nickel and nickel in pig iron. I bought Sherritt throughout the low to the mid $3’s (my average cost is $3.48) and did pretty well on with it until the last couple of weeks when the stock has dropped back to the $4 range.

About half of that drop occurred after the release of the second quarter results. The stock pulled back because nickel production from the Moa joint venture was a bit weak in the first half and because full year guidance for the Ambatovy joint venture was reduced (from the range of 44,000-50,000 tonnes to 37,000 – 41,000 tonnes). The Cuban oil business saw production in-line with what I had expected and the company has recently signed an extension on its oil production sharing contract with the Cuban government and expects to expand that agreement to include new exploration targets.

The Ambatovy Ramp

The slow ramp at Ambatovy comes as no surprise. Its been slowly ramping for almost two years now. The mine has seen one hiccup after another. Yet there is progress being made towards positive cash flow. By the first quarter of 2015 Sherritt is expecting the mine to operate at 90% capacity (its currently in the mid-70’s) and when it does cash costs are expected to drop to the $3-$5 per pound range.

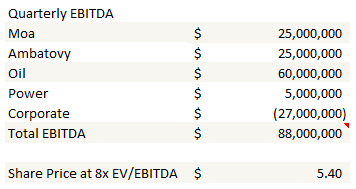

Full production at Ambatovy is the first of two catalysts that define the event path to a higher share price. Once at full capacity, Ambatovy will produce slightly more nickel and cobalt net to Sherritt than Moa. The high end of the cash cost range at Ambatovy is $5 per pound, or about what Moa costs right now. So its not unreasonable to expect similar or better EBITDA from Ambatovy than what Moa currently delivers. Below is a rough EBITDA estimate for the company as a whole, including a contribution from Ambatovy. The estimate assumes everything remains the same at Moa, in the oil segment and with the power segment. The EBITDA of those segments are roughly based on first half numbers.

There is reasonable upside to be had with Sherritt from Ambatovy alone if and when the mine produces up to expectations.

The Indonesian Nickel Ore ban is working

The EBITDA estimate that I came up with above assumes nickel prices in-line with the second quarter, or $8.38 per pound. The second leg of the thesis is the expectation that by this time next year, nickel prices will be significantly higher than that. I am optimistic that if the Indonesian export ban hold, nickel will move up well past $9 by this time next year.

If you want a more detailed background on the current state of the nickel market I would refer you again to my original post on Sherritt. Here I’ll only briefly cover the main points. I bought Sherritt because of the Indonesian ban on exports of nickel ore. Indonesia basically banned exports of unrefined nickel in hopes of encouraging investment in the country (via refining capacity). Somewhere around 30% of the nickel produced globally comes from nickel in pig iron that is mined in Indonesia and smelted into nickel in China. The loss of that production will eventually mean a dramatic tightening of the nickel market.

My concern has always been the fortitude of the Indonesian government. The ban on exports has undoubtedly hurt the economy. Jobs have been lost, growth has slowed. I haven’t felt comfortable with making my position too large because of the headline risk that the government eases up or reneges entirely on the ban.

But as time passes I am becoming more comfortable that the ban is here to stay. The government’s strategy is working. Short term costs have been manageable and long term investment is beginning to flow in. From the Jakarta Post, quoting Morgan Stanley:

Chinese companies have already committed to downstream processing build out of Indonesia – the primary purpose of the ban,” they wrote in the note. “Indeed we now include a healthy ramp-up profile of nickel pig-iron smelters in Indonesia.”

Plans are being drawn to build nickel smelters in Indonesia. As many as 40 nickel plants may be built in Indonesia by 2017. This capital investment will soon begin to exceed any economic losses the ban may have caused:

Tanjung pointed to recent data from the country’s investment coordinating board that showed close to $8 billion was being spent to build three alumina refineries and two ferronickel projects. “This is creating investment in Indonesia,” he said. More projects were expected to follow, Tanjung said, which would help reduce the country’s trade and current account deficits.

Looking three years out, the capacity added by these smelters may make the supply/demand dynamics for nickel unfavorable. But that is a long way away. The more immediate future is a significant supply deficit next year. The consequence should be much higher prices. From the MetalMiner:

Back in September at Glencore’s Investors Day, Director of the Nickel Commodity Department Kenny Ives said the Indonesian mining ban, if implemented, had the potential to double or even triple the nickel price – in fact, “the sky’s the limit” were his words, if I recall correctly. At the time, nickel on the London Metal Exchange was under $14,000 per metric ton, and not a few participants raised their eyebrows at each other as if to say “nickel miner talking up the market.”

Today, the nickel price is over $20,000 per metric ton and rising. Last week it rose nearly $2,000 in the space of a couple of days. According to a Bloomberg article, Citibank reported last week that the price could rise to over $30,000 next year as the nickel market swings to a deficit of 132,200 tons next year from a surplus of 13,800 tons this year.

Conclusion

I have not added to my position in Sherritt yet, but I am tempted to. I think that the tailwinds from higher nickel prices will be strong, particularly if Ambatovy can demonstrate that it is a viable long term source of nickel. As I wrote in my original post about Sherritt, I sat through the run that nickel had in 2006-2007. Next year, as stockpiles begin to dwindle and it becomes clear that the Indonesian government is not backing down, I wouldn’t be surprised to see nickel prices go far higher than anyone is anticipating.

Not sure if you saw, but Clarke sold out of Sherritt last quarter and this quarter with this quarter’s sale around $4.31 , so you’ve lost that activist push. It appears that the board implemented a lot of the things Clarke was looking for, so may not be a big deal – just hope they don’t fall back to their old ways. There is lots of potential here, but there has been for a long time, so strong execution will be key to prove they can surface this value.

Thanks Brent – i didnt know that Clarke was out. I agree their track record makes me worry too. But the buoyant nickel price is at least out of their control 🙂