Looking at more quarterly results: Air Canada’s miss

Air Canada is a fairly large position for me so I’ve spent a lot of time on their quarterly results in the last two days. The short story here is that the stock stock got hit because revenue per average seat mile (RASM) was below expectations and because of this, earnings were also below estimates.

There was an expectation among analysts that because load factors (how full the aircraft is) were strong in the second quarter, and because there was anecdotal evidence that ticket price checks showed improvement, Air Canada would pull off a decent year-over-year RASM increase in addition to its cost savings.

Because they didn’t the company missed earnings estimates and, on Thursday, the stock did what the stock did. The average estimate for earnings per share for the quarter was 51c. I saw that BMO was as high as 57c. The actual number came in at 47c.

First, let me say that I added to position on Thursday afternoon. I actually pretty much picked the short-term bottom on this one, a rare occurrence indeed, getting in at $8.50. I added because while the stock was down hard on the RASM miss, I thought that once everyone wrapped their heads around why, we would see it quickly move back up.

RASM was down because of Air Canada’s focus on adding economy seats to long haul destinations. In particular capacity is being added to leisure destinations through Rouge, which is marketed as a low cost solution. The added seats are generally lower RASM seats. So you add more of this capacity and the overall RASM number declines even as price increases to the existing capacity take hold.

The thing is, the new capacity being added is at an even lower cost per average seat mile (CASM) seat. Air Canada’s strategy is to add capacity in this manner and in the process to increase margins. That’s what happened in the second quarter. While RASM was down, CASM was down even more with the overall effect of increasing gross margins by 50 basis points.

I think that what really threw everyone for a loop was that WestJet had reported strong RASM numbers in their second quarter, up 4.8%. The reflexive reaction is that both focus on North American flights so they should both see similar results in their Canadian and to a lessor extent their US business. Yet the weakness in RASM for Air Canada was most noticeable in the domestic and transborder market.

Management touched on the discrepancy in the call. WestJet has a very different focus than Air Canada right now. They are expanding their business by flying more short, regional routes. These routes are naturally higher ticket prices for the distance, but also quite naturally, higher cost. WestJet’s strong RASM number is a consequence of their mix change in the same way Air Canada’s is. Indeed, CASM at WestJet increased significantly year over year, reflecting the higher costs of these shorter destinations.

Watching the stock fall some 8% in Thursday, what I think is being missed is that the lower yields are mostly a transitory phenomenon. They are putting more seats on low cost routes. And by adding significant capacity in the short run they are limiting ticket price increases on those routes (though given the increase in load factors that they experienced, meaning they are actually filling more of the plane then they were a year ago, the impact should be somewhat muted). But with decent economic growth (and a corresponding increase in demand for air travel) both of these effects will work their way through the system over time.

Once this happens Air Canada will start building off that revenue base. So far the company hasn’t raised prices on the new capacity, but that doesn’t mean they won’t. On the call when asked why they were not raising prices given that demand was out-pacing the additional capacity, the company responded that because the capacity was new they were reluctant to begin to quickly reprice it upwards. I think its too backward looking to see second quarter RASM as indicative of what to expect going forward.

If demand stays strong increases will happen and you will begin to see margin expansion from both ends. Its not a terribly complicated formula; you just need to see continued demand and no hiccups on the cost reductions. The unfolding of that thesis, and the valuation, is the story here.

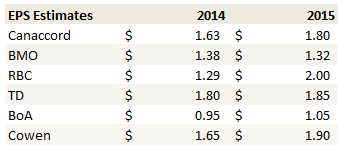

The valuation remains compelling. While I don’t have access to all the reports on Air Canada, the one’s I do provide forecast earnings per share estimates that just about have to lead to a higher share price if they are met. Apart from Bank of America, which must be anticipating that either the cost savings won’t be realized or that we will actually see yield declines going forward to come up with those numbers, the other estimates are well above $1. Even with a conservative multiple the stock should be in the low teens.