Week 163: Knowing when you are not at an advantage

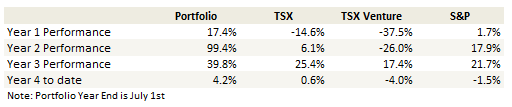

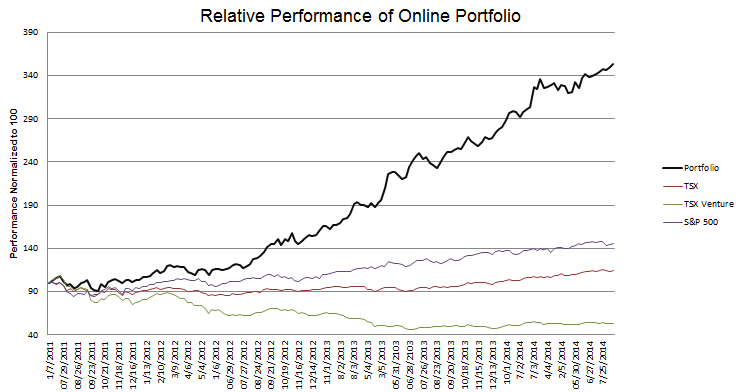

Portfolio Performance

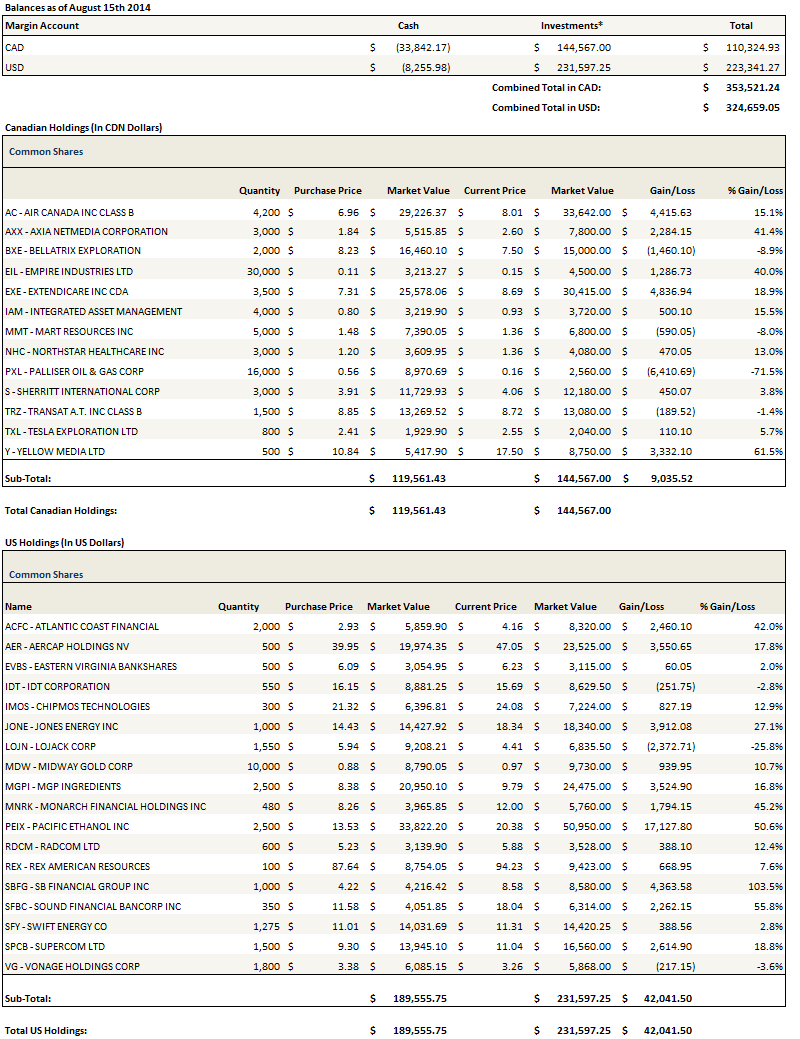

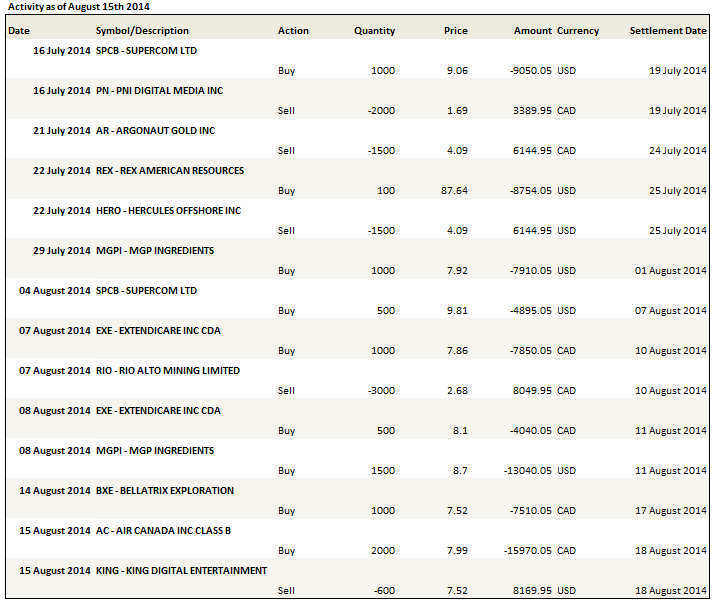

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

Note that this update is as of Friday, August 15th. I have been a few days delinquent in getting it out.

I have strayed from my bread my butter of late, away from the tiny micro-caps that pass everyone else by and into the world of still small but not so obscure caps. These are stocks like Air Canada, AerCap and Bellatrix among others, still far from being large caps, but big enough to receive the attention of analysts and funds.

I am not so sure of my own advantage with these stocks. I may be overstepping my own abilities to think that I can see something here the market is not. I am under no misconceptions about my research. There is simply no way that I, as an individual investor with a couple of hours of free time every day, can match the depth and scope of the research that the institutions have.

As I research these stocks in greater detail, I can see that. Air Canada is a good example. At first it appears to be a relatively simple play on earnings with the tailwind of the economy buoying the ascent. But its not so simple. The strategy that Air Canada has staked their turnaround on is complicated, it relies on large low cost but low revenue capacity additions to routes that, in some cases at least, are not under-served already. As the second quarter showed, they are losing revenue (on a seat-mile adjusted basis) while other airlines are gaining it. There is the headwind of the Canadian dollar and always the worrisome possibility of higher oil prices. The cost reductions depend to some extant on large capital expenditures for brand new, high efficiency aircraft that will add to debt levels over the next couple of years.

All of this is known by the analysts. They have resources looking at the flight path capacities, researching the other airlines and how their results align, doing spot checks of ticket prices to get an early indication of demand. I can get the reports (at least some of them) and read the analysis, but anything you read by someone else is being read too late.

I don’t think its a coincidence that my best returns come from two places: 1. sectors or stocks that are so hated that no one is following them any more and 2. companies that are so small that no one cares. I do extremely well when my primary opponents are disgust and indifference. I do less well when my skills are pitted against teams of analysts working 10 hours a day fine tuning models down to the penny.

Thus it is that I am very excited about my position in MGP Ingredients. I think there is an opportunity here to do extremely well. I don’t believe there is a single analyst that follows the stock. I doubt that there are more than a few dozen people in New York City that have even heard of Atchison Kansas. The last Seeking Alpha article on the name was done in 2007. The last bulletin board post I was able to find was written over two years ago. I doubt there is a screen outside of a short that would pop up the name as a search result. I only have three foes here. The first two already mentioned, with the third being my own constitution, accepting that I can be right without any other confirmation. I have no problem with that one.

I only made a few other moves in my portfolio and for the most part those consisted of adding to positions that I liked. I added to Extendicare, Bellatrix and Air Canada. I also sold out of King Digital for reasons I have tweeted, as well as Rio Alto Mining, which I sold way too early.

Adding to Positions: Extendicare, Bellatrix and Air Canada

I added to Extendicare immediately after earnings and the news that the investigation by the Office of the Inspector General had been settled. As the company said on the call, with the investigation complete the major impediment to a sale of the US operations is out of the way. In the quarter Extendicare was also able to lease 10,000 of their beds in Pennsylvania, Delaware and West Virginia for what works out to $10,000 per bed. Alex Martin, who I follow on twitter, extrapolated the valuation to the rest of the portfolio to come up with the $7+ per share valuation for the US operations as a whole. Another $4-$5 for the Canadian operations and there is still upside with Extendicare, even from this level.

I averaged down with my position in Bellatrix. Averaging down is something that I only do after quite a bit of introspection as I am fundamentally opposed to it, but with Bellatrix I just couldn’t see the stock being down at the sub-$8 level for too long. The problem that the company is grappling with is infrastructure. Existing gas plants are running at full capacity so there is little room to bring on new wells. They are building their own plant to alleviate the bottom neck but that costs a lot of money up front and we are going to have to wait until the spring of 2015 to see it.

This is a classic example of a case where value is delayed but not impaired. The production is there (witness the Ferrier well producing 18MMscfd). The gas plant will drive even more value: I’m quit certain (though not positive because I can no longer access the call) that the company said that the new gas plant would increase liquids yields from 40 to 80 bbl/d – resulting in another 8,000 bbl/d of NGL production. This would be significant incremental liquids production that is less than a year away.

I have been quite lucky with my timing though. The delay may turn out to be far shorter than I had anticipated. Two things happened in the first two days of this week that have caused the stock to shoot up substantially. First, this Top Idea article on Seeking Alpha laid out the peer analysis in much more detail than I did and I’m sure was mostly responsible for the move in the stock on Monday. Second, an article in the Globe and Mail Tuesday reported Orange Capital is rumored to have taken a 5%+ stake in the company. Its nice to catch a bottom once in a while.

Finally, I’ve already said a lot about Air Canada so I will just add this. What they are trying to do is simple. They are adding low cost capacity to lower costs and drive margins. So far the strategy is working and they saw a 50 basis point increase in margins year-over-year in the second quarter. They said on the conference call that their 2014 results will only reflect about 1/3 of the overall cost savings they eventually hope to realize. And the stock is trading at a single digit multiple. While it is always helpful to know the details of the story, sometimes it is equally helpful to be able to distill the story down to a few key points that, when you brush away all of the debris around RASM guidance and yield declines and length of flight, paint a pretty clear picture of a stock that has significant upside. On Friday I was able to do that, and so I added significantly to my position.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

I generally invest in very small and underfollowed stocks like you do and have found my best success comes from doing my own analysis.

But the market moves in cycles and it seems we are in the part of the cycle when it makes sense to go into larger stocks. There are still some good small stocks out there, but they have generally moved up and the upside/risk ratio has changed.

I think you are just taking what the market is giving and moving to where the best opportunities are, which is just smart investing.

That’s a good point. Anything you are looking at right now that is worth mentioning?

Congratulations on your excellent performance.

We go together with Extendicare holding, seems to be clearing the doubts and soon will be announced the sale of the USA business unit.

Do you have any idea of the possible selling price?

All the best.

Iban

Re: small stocks – Have you taken a look at MPET or DAP.U? Those seem like interesting opportunities.

thanks for the ideas

Thanks for your wonderful investing ideas and your due dilligence in detail, which is very interesting to read. I was wondering, if you have taken a look to Kandi Technolgies Group (KNDI)? The Chinese version of Tesla with wonderful results, both the stock and the financials, but still a lot of doubts with very negative Seeking Alpa articles.