Betting some more on BXE

My portfolio had a tough week and has had a weak September. As it goes when I show weakness, I am quick to clean house and start anew. This week I jettisoned a number of names (including Sherritt, Mart, Straight Path Communications and Aercap), made a number of positions much smaller (including Overstock, IDT, Transat, Sanderson Farms, and Supercom) and raised a bunch of cash. When the dust settled I had 10 positions remaining of significant size.

One of those positions is Bellatrix, of which, in the midst of oil and gas carnage everywhere, I bucked the trend and added to this week. This after I had mentioned in a tweet a couple weeks ago that a recent add would be the last one.

Adding again to $BXE again here at $7.70 (cdn). Think I’m probably in as much as I want to be now.

— L.Sigurd (@LSigurd) September 4, 2014

Well I lied. With the stock dropping to the mid-$6’s I decided to revisit the whole idea, and after doing so, I added fairly aggressively. I do not make this decision lightly; as I have written before, once I have a full position I rarely add to it if it starts losing money. There’s just too much chance that I am wrong. At the time of the tweet Bellatrix was a 4% position for me. Its now the largest position in my portfolio at 12%. My average cost base is down to around $7.17.

Why was I willing to add so significantly? Because the work I did helped reassure me that my original idea is most likely correct; that the company is suffering from a short to medium term processing bottleneck that should be alleviated by the commissioning of their own plant in mid-2015.

Most of my work focused around a production/decline model that would help give me a better idea of how production should trend under various drilling scenarios and capacity constraints.

My model is simplified, but not too simplified. I think that oil and gas models are some of the most difficult to make. The inputs require estimates of decline rates, which changes over the life of each of the wells in the field, drilling schedules, which are impacted by weather, rig and processing availability, and in the case of the Western Sedimentary Basin, by spring break-up. There are so many difficult to determine parts that I think it is better that one not try to confuse precision with accuracy.

Thus it is that I have based my estimates on two type curves for the primary zones that Bellatrix is developing: the Cardium and the Notikewin. I have not further delineated the Cardium between Ferrier Gas, Pembina Oil, Willesden Green Oil and Strachan liquids rich gas areas. I don’t really have any insight into how many wells Bellatrix is going to drill into each individual area so there is really no point going to that level of detail.

I modeled out for the next six quarter, until the end of 2015. Past 2015 I think it’s really anybody’s guess what capital expenditures will be. It will depend mostly on how close to the model 2015 turns out. I assumed an initial base decline and added wells each quarter at an average quarterly rate consistent with the type curve. The well scheduling and costs are based on historic precedents. I go into each of my assumptions in greater detail below.

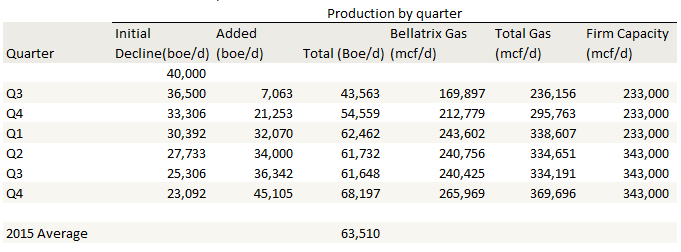

The conclusions can be summarized in this table:

Now before I go any further, I want to say that I am sure that someone is going to glance through this post, look at the numbers in the tables, and that make some off the cuff comment or send me a nasty email about how Bellatrix is never going to hit the fourth quarter or the first quarter 2015 number, or the 2015 average for that matter and tell me how stupid or naive I am to suggest this. Now even though I’m sure that will still happen, because that person would not read a paragraph this long, let me make clear for the record that I am not making a production forecast here. As I stated at the beginning of this post, I am making a model to validate my thesis that Bellatrix is constrained by facilities but that if those constraints were removed there is significant growth to be had. My quarterly production estimates are clearly not considering processing constraints and thus should not be considered to be a “forecast”.

With that said, on to the assumptions.

All of my assumptions are listed in the foot notes of the spreadsheet which I am going to make available if anyone wants to review it and verify if I have any mistakes, feel free to email me. Some of the more significant assumptions are described below.

First, I ignored the structure of the individual joint ventures (Grafton and Troika). I simply assumed that a net well drilled is a net well produced. In reality, in the last two quarters about 28% of the wells drilled have been joint venture wells. The joint venture wells should allocate more production per dollar of capital than a non-joint venture well. Grafton pays 82% of the capital and gets a 54% interest before payout and a 33% interest after payout. Troika pays 50% of the capital and gets 35% and 25% before and after payout respectively.

Ignoring the joint venture terms should be a conservative assumption. I thought about trying to incorporate the joint venture structures into the model, but it makes things a lot more complicated; you have to make assumptions about the wells being drilled by the JV’s, about when payout occurs, about how the existing joint venture wells affect the decline of the existing production base, and the specific terms of the JV’s seem to be based on IRR before payout which means that even using the before payout percentage is probably not correct. The truth is, I got the answer I was looking for out the model as is, so I didn’t need to go further with an assumption that was already conservative.

My Cardium and Notikewin type curves are based on the curves presented in the company’s September 2nd corporate presentation, available here. Its worth noting that the Cardium type curve (average 2013 and 2014 wells) on slide 19 is significantly better in the later months (8-12) than the one the company provided in the earlier April 2014 presentation (available here). In year 2 I estimated that the Cardium wells would experience a 10% decline rate. The Notikewin decline curves for both year 1 and 2 are derived directly from their type curve, which went out the full 24 months that I needed for my model.

I assumed a decline of the existing production base of 35%, which is what the company stated it was on the second quarter conference call.

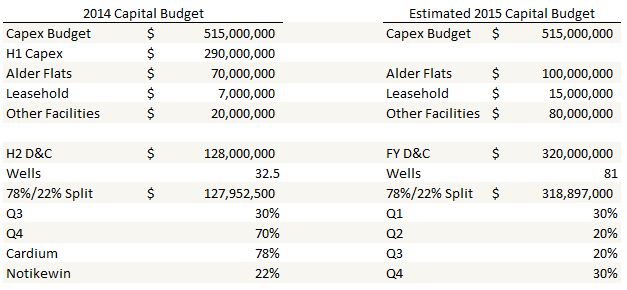

My capital budget for what remains of 2014 is based on company guidance and my own guesstimate of facilities and leasehold costs in the second half of this year. We know that there is about $70 million being spent on phase 1 of Alder Flats in the second half. I’ve assumed that they will need to spend an additional $20 million in general maintenance and tie-in facility costs. I based this off of some eye-balling of their historical capital expenditures when they didn’t have any major projects on the go.

The 2015 budget assumes most of the rest of the Alder Flats Phase II spending (which seems to be about another $100 million in total) and an additional $80 million of facilities spend outside of Alder Flats. I have to admit that I’m not super-confident in the accuracy of my facilities spend for 2015 so please pipe up if you have reason to think these numbers aren’t accurate.

I’m assuming a 78% Cardium, 22% Notikewin split on the drilling and completion budget. This is based on the trailing twelve month average. I know that Bellatrix typically drills 0.5-2 wells outside of these two areas each quarter, but I don’t really have any information on what this production is so I’ve decided to simplify and assume that all drilling capital is spent in the Cardium and Notikewin. If its not at least as high IRR they shouldn’t be spending it elsewhere anyway.

My seasonal drilling split in 2015 is dampened a little from the historical numbers. In the past twelve months I found that Bellatrix only drilled 13% and 14% of their total wells in the second and third quarter respectively. However when I used those numbers for 2015 I got pretty extreme fluctuations that I didn’t think were realistic. In reality there is so much else going on from quarter to quarter, what from wells coming offline to drill other wells on the same pad, timing and duration of spring break-up, even changes to the line pressure due to fluctuations at the TransCanada tie-in (the company said it was 300 psi higher in Q2, not an inconsequential amount!), that I don’t think its a great idea to pretend you can be too precise. Better to smooth out the fluctuations and observe the bigger picture trend, which is really what I’m after here.

Finally, I assumed that the Cardium wells cost $3.75 million to drill and complete while the Notikewin wells cost $4.6 million.

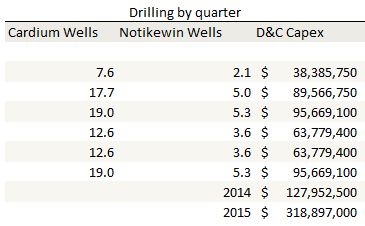

Using the above assumptions, my assumed overall drilling and completion spend by quarter is illustrated in the table below:

Finally, I assumed that gas represents 65% of production over the entire 18 month period. This probably isn’t right; in fact, once the Alder Flats plant goes into operation one would hope that percentage would shrink and NGL production would increase as more barrels of ethane, propane and butane are extracted from the gas stream but again, for the broad brush that I am hoping to paint with, it will suffice. I also assumed that partners gas continues to represent 39% of the overall gas that Bellatrix has to find processing capacity for. So the column titled “Total Gas” represents both Bellatrix and partners total gas volumes.

Conclusions

So its a simple model meant to allow for some simple conclusions. The first conclusion, and the one I made the model to draw, is that the company can grow production extremely quickly if the capacity is there to process it. As long as my assumptions are accurate, its really not difficult to see Bellatrix producing 60,000 boe/d by this time next year.

The second conclusion is that until Alder Flats is operational, they are clearly going to be running into capacity constraints. I mean they are already surpassing their firm capacity (note that I realized after snipping the table that my Q3 capacity should not include the incremental 20 mmscfd from Blaze, as that isn’t expected until Q4). This means that any incremental production depends on interruptible capacity that, as history guides, can’t be depended on. Looking at the fourth quarter, its no wonder that when asked about the opportunity to exceed the exit guidance of 48,000 boe/d, Ray Smith replied that they would be tight to meet that guidance with current capacity constraints.

The important point is that it does appear to be only a processing problem. If the capacity was there, Bellatrix would easily exceed 48,000 boe/d. Keep in mind that my model is conservative in another respect; it neglects the “behind pipe” volumes that Bellatrix is always quoting and implicitly assumes that behind pipe production remains behind pipe throughout the forecast period. I did this to add a bit more conservatism to the results. But the actual available “if everything could flow unconstrained” volumes are probably about 5,000 to 6,000 boe/d higher because of the extra amount not being produced due to capacity constraints.

The third point is that the capacity constraints are going to continue even after Alder Flats is completed, just at a higher level. The model suggests they will quickly fill up Alder Flats with their own and their partners gas. This is a good news/bad news story. By Q4 2015 they are again running up against the capacity of the facilities they feed into.

The fourth point, is that you could almost make the argument that Bellatrix might be better off without the JV’s, at least in the short run. I realize that what I am going to speculate is too simplistic but in rough terms, if Bellatrix was drilling 100% wells, they would have a 39% more capacity available and wouldn’t be running up against this capacity problem. And while I don’t know all the terms of the JV’s I have to wonder if the company is forced to fill more pipe with JV gas than they would like to satisfy the IRR commitments. On the other hand the terms of the JV’s are generally favorable, which should help, but it’s worth considering where things would be without them.

The reason I use should in the last sentence is to be honest, I don’t really see much of an impact of the JVs on drilling and completion costs. When I use the anticipated cost of drilling a Cardium and Notikewin well and look at the number of wells drilled over each of the last four quarters

The fifth point, one that is somewhat peripheral but that I am nevertheless going to make, is that if the company experiences this kind of growth, they are going to continue to have a high base decline rate. I bring this up because I keep hearing this mentioned as a real negative for the stock. I’m not really sure what to make of this whole decline rate fascination. It seems like every second analyst on BNN is in love with a low decline rate production profile. It seems to me that this could be flipped on its head to say the company isn’t growing very much. I don’t see how you can grow production ~50% (like the model is suggesting Bellatrix can do in the next 12-16 months) and not have a high decline. Nearly half of their production will be less than 16 months old, so the decline rate is going to be large. But this is a bad thing? If someone could tell me I’m thinking about this wrong I would appreciate the explanation.

The finally thing I would say, and I say this with the caveat that assumes I am correct in my analysis and haven’t made any mistakes in my assumptions, but if I haven’t, then I wouldn’t be surprised at all if Orange has gone through a similar sort of analysis and concluded that Bellatrix can rather effortlessly increase production while spending within their forward cash flow once the processing infrastructure is in place and that is why they are confident enough to keep buying stock as the price sinks lower and lower.

Finally, I think the thesis is still valid. So I added. We will see how it goes.

It will depend what gas prices do, what oil prices do, and how well the team from Bellatrix can execute. But I think there is a reasonable chance the stock is significantly higher by next year at this time.

I think you are a little early.

Why?

he is just talking from technical point of view, don’t listen. BXE is very very cheap and Orange thinks the same

It’s possible that someone from Orange follows this blog. Lane recommended PHH, and then Orange got in. He’s been talking about BXE for some time and now Orange is in BXE. They also were in Nexstar and Sinclar Broadcasting but I don’t know who got in first.

I don’t know anything about this company, but I don’t understand why you would second guess your research on the company when it’s pretty clear the reason it’s going down is because the entire sector is dropping. Seems like if you have a problem to investigate, it is on the macro level, not micro.

I think that there is both a micro and macro issue worth investigating. This post just focuses on the micro.

That’s just not true. BXE has far underperformed the energy sub-sector ever since they ran into capacity issues.

One important key element missing from your analysis is the profitability of the wells from a source outside of the presentation – it’s obviously biased. Production growth is interesting, but the profitability of that growth is more important relative to the capital spent – cough LTE anyone? Also, how are wells actually tracking relative to prior years?

I also think you’re missing another real key point here, which is quality of management and SO SO SO important in the energy sector. This is a homogeneous sector and we can pick and choose so many companies with comparable or better assets. One thing to consider is that BXE didn’t have the foresight to anticipate these infrastructure bottlenecks… AND with the recent secondary JV just signed, will be required to continue demonstrate production growth without retaining flexibility of capital.

Lastly, just for correction, it’s spelled “Notikewin”

Sorry but I think this comment is rudely written. I dont like these sort of allegations of fraud when they haven’t been backed up by anything. Im not going to respond to its points.

If you haven’t already went through them please take at look at “bankstocks” posts in the BXE thread on investorvillage.com message board. She or he points out specific contradictions in various BXE’s quarterly reports. Since you stand by your endorsement of BXE, please take a bit of time to refute bankstocks’ allegations of doctored or messed up quarterly reports.

I’ve read through all his comments. But first, let me say I am not “endorsing” any stock. I’m writing about the reasons I own each stock I own. And I might change my mind on any stock I own without saying anything to anyone. So nothing I write is an endorsement. I don’t like the way you word your comment because I don’t have an obligation to refute anything. He is entitled to his comments and I am entitled to mine.

In my opinion Bankstocks allegations boil down to 3 points:

A. There is a JV with Daewoo with numbers that don’t make a lot of sense. There is one quarter where the gross and net capital requirements actually increases (??), and the net wells to BXE in the JV change from quarter to quarter from 23 to 35 to 30.4.

So I think he’s right that if this was a straightforward JV those numbers don’t make any sense. But we don’t really know any of the details of the JV. Would it be nice if management disclosed all the details of every JV agreement so we could align it with the numbers? Sure, but they don’t. That might be reason to petition management for better disclosure but bankstocks seems to be going a far more severe level with it. I don’t understand why?

But if this was something nefarious, would Bellatrix really be sand bagging their net working interest initially only to raise it from 23 to 30.4 wells, and in between overstate it at 35? Also, the net costs per well have actually improved over time.

I think its far more likely that we just don’t know all the terms, and maybe even that the terms have been adjusted over time. So that is a great reason to petition for better disclosure. But it seems pretty extreme to be calling fraud.

B. there is capex that moved from facilities to D&C from Q1 2013 to Q2 2013 (I’m sorry but I don’t have these numbers in front of me so I might have this backwards). I saw this one before bankstocks even mentioned it, when I was doing my spreadsheets a couple months ago. It didn’t seem like a big deal to me.

C. BXE is filling up their pipe with partners gas. Yup, I stated the same thing in my post, so I totally agree that this seems to be happening and I bet this is where a lot of the analyst discontent comes from. It’s less clear to me whether the terms of the JVs over the long run are favorable enough to compensate for this negative.

That’s all that I have garnered from his posts. Anything else you’ve seen?

Only other thing I’d say is doesn’t it seem weird to you that someone with a large position would keep using the word fraud all over the message boards and basically writing things that will cast doubt on the stock for any weaker hands who have not reviewed the numbers themselves? I think this is really strange behavior.

So no (I mean your name), your assertion that Bellatrix has a terrible management team is flat out wrong. The stock price has gone up 700% since jan 1 2009 (http://www.bellatrixexploration.com/docs/default-source/presentations/bxe-corporate-presentation-sept-2-2014.pdf?sfvrsn=6 pg. 10). But the reason the stock has gone up so much is because management has constantly shown that they can find, develop and produce oil at under $20 a barrel and Nat Gas at under 1.25 a mcf over 5 years (I compared CAPEX + Acquisition costs – divestment proceeds to the change in oil and nat gas times $20 and $1.25 respectively). A management team that can do that will compound capital at a high rate in the industry and buying them below NPV of reserves probably is considered a steal (I say probably because I only have looked into them briefly but will look further at this reduced price). Frankly, it doesn’t matter if oil is at $80 or $100 because of the proven ability of management to find, develop and produce oil and gas at a low cost.

I don’t like the facilities bottlenecks either – it’s an additional cost & delay that some other companies don’t have. I took a position nonetheless, because, at this stock price, what’s the downside? Production will be substantially higher soon as this post illustrates, even if there’s a delay (plant construction, lower oil prices). Unless oil prices stay below $60 for years, I think the thesis is intact. 2015 EV/EBITDA ~2.5 at current oil prices and ~5 at $60 oil (if I assume production cost ~ $30/bbl). Maybe I’m oversimplifying things (liquids = oil) but I don’t see much downside really. So I took a position.

Curious on how you arrive at that number. The street is assuming something like ~$450 million in EBITDA in 2015 which would imply a 2015 EV/EBITDA of 3x – close to your number. However, the Street is also assuming $100/Bbl oil price on average for 2015. So if you take out $10 in the oil price, that roughly equates to $290 MM of cash flow using Street production estimates (51,000 Boe/d) and a reduction in netback (adding a little back for lower royalties). The result as an EV/EBITDA of 4.3x. That’s where I think the stock has traded historically. So I think perhaps saying the EV/EBITDA is cheap is implicitly saying that you’re trying to bet on oil prices rising because it seems pretty efficiently priced – at least relative to its history.

david you are funny, how is it possible to reduce CF from 30% the EBITDA from 450m to 300m with just 10$ drop in oil prices, when % of oil production in BXE is less than 20%…

you historic numbers are also funny, for example in 2011 with the European crisis and gas prices in a very bad shape BXE traded for 55k BOE ( based on 12k boe/d in 2011) in 2011 BXE traded for around 6x EV/CF.

In 2012 with gas prices in all time lows,BXE traded on average for around 4$ represents EV/flowing BOE of 40.000$ , the EV/CF was around 6x ( based on 100m CF in 2012 and EV=600m).

so in your apocalyptic scenario BXE is going to do 300m CF and 51k BOE/d in 2015, that means 8$ ( based on CF) and 10$ based on flowing BOE…

And remember in 2012 gas prices went to 2$ in 2012¡¡¡

on sept 2012 gas prices were around 3,40( NYMEX), gas prices in sept 2013 were around 3,85. right now is at 3,75…i think part of the move is due to USD strength, if you back out the 10% USD appreciation in 2014 Gas price could have been around 4$…

Yesterday i was looking at couple E&P in CANADA like Kelt or delphi even after the big sell off they trade for around 6x-8x EV/CF and 60k/flowing BOE with around 65% gas production like BXE. this suggest a price for BXE around 12$-15$ in 2015…

That doesn’t make sense

Yes, but when has BXE ever traded in line with 6-8x EV/CF? Also how do you expect EV to change going forward? They will increase their debt load dramatically so that EV goes up

Falling knife. Don’t catch. At least wait for the tax loss sellers to clear out.

Agree that I should have worded my question better – my apologies, and thank you for

taking the time to give us your viewpoint on bankstocks’ allegations. I have no opinion, just

a miniscule position in BXE and the need to decide whether or not to increase it. I doubt

there are any nefarious goals to bankstocks posts; he appears to be just a concerned shareholder with a well above average understanding of accounting and oil and gas business and repeatedly points out he’s long the stock.

I don’t know. His comments in light of his long position make no sense to me. There must be more to it. But anyways, who cares, what matters is what happens to the company, to oil, to gas prices.

Not sure if you saw the latest operations update, but it’s another sign that management has mismanaging or having trouble with the takeaway capacity of its volumes. The comment earlier on BXE’s management is a good one – if you do look at performance vs. the TSX Energy Index since 2009 they have done well. However, I am not sure if the company, which was smaller and more nimble back then, is the same company today which is much larger and is more dependent on execution. I think you can find better value in other smaller cap energy stocks… especially with the whole sector down.

Which names would you recommend?

I would like to review your model if you wouldn’t mind sharing. Have done quite a bit of work on BXE myself and hopefully can offer some insight/assumption-checking.

GXE, CJ

Thanks – why GXE instead of TBE?