Week 168: Cutting my gains

Portfolio Performance

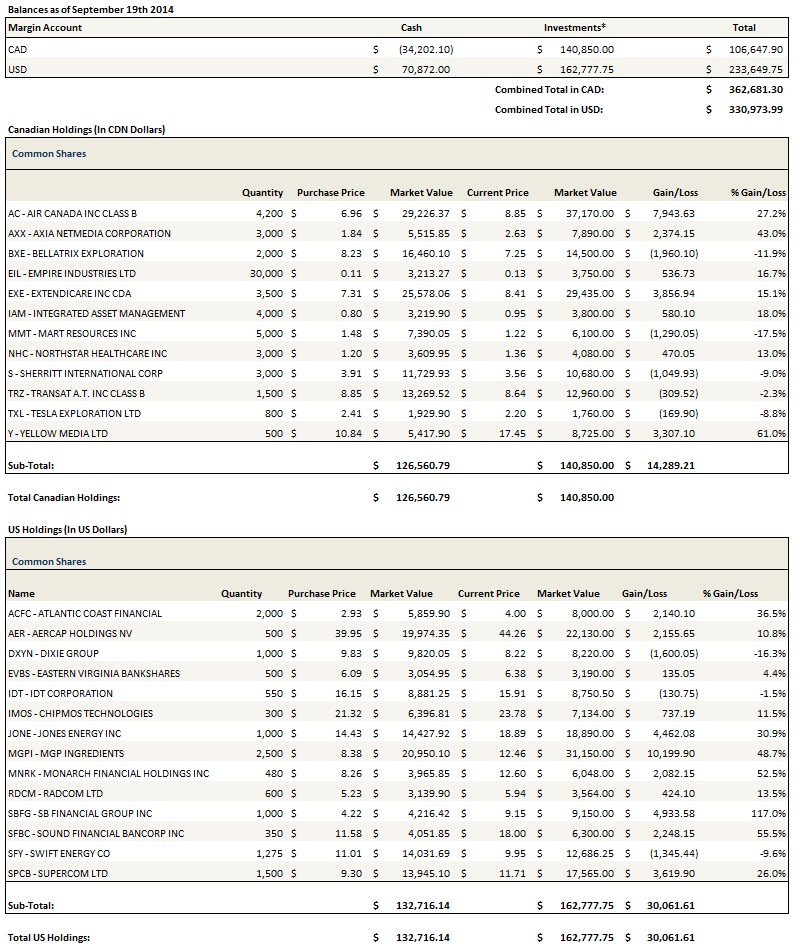

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

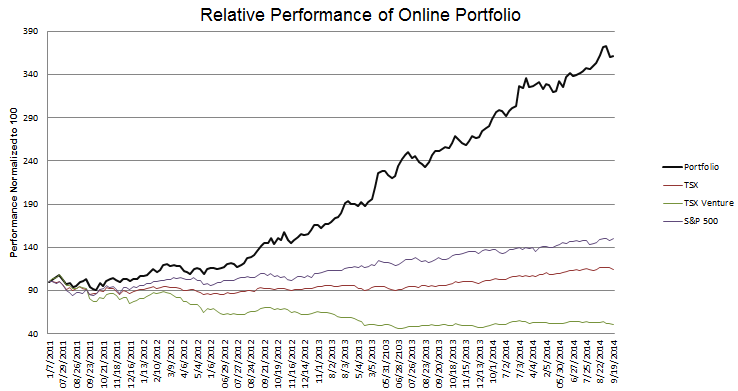

I don’t know if the chart of performance really does justice to the volatility my portfolio has had over the last couple of weeks. It feels like much more of a roller coaster than that little blip in the trend that you see on the screen.

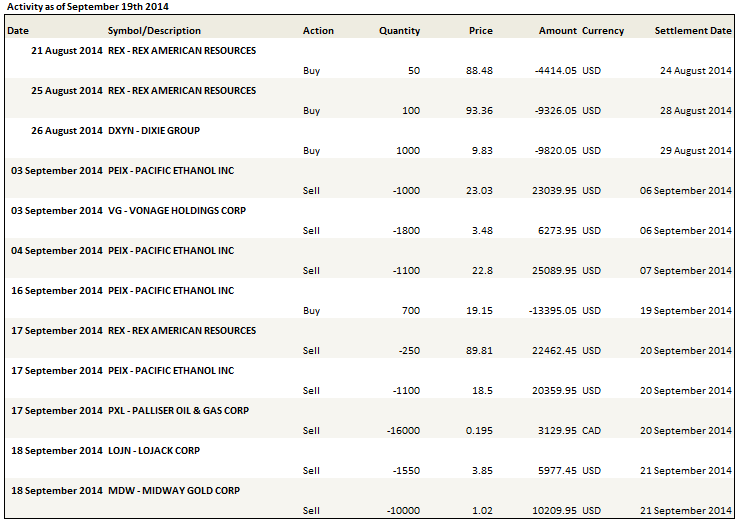

I sold out of the rest of Pacific Ethanol and Rex American Resources in the first half of this week. I hemmed and hawed through the weekend, even briefly added to my position to Pacific Ethanol on Monday (at the same time I was reducing my position in Rex American), but the volatility of the stocks, the declining price of ethanol, and specific to Pacific Ethanol, my uncertainty with respect to their corn basis (I concluded tentatively it is actually quite a bit higher than Q2) led me to capitulate on many of my shares on Tuesday. I followed that up by selling the rest on Wednesday in the minutes that followed a very bearish EIA inventory report (+800,000bbl!). I tweeted on my sales at the time.

My caution turned out to be fortuitous as the stocks continued to fall the rest of the week. I was even able to catch a few dollars of profit on the way down; always remembering the old classic to which this blog takes its namesake, I took the lesson that if a stock is to be sold it is likely just as well sold short, and so I took a small short position in Rex American and a few $18 puts on Pacific Ethanol. The puts were sold Friday and my short position has been cut more than in half, so these were merely short term trades taking advantage of a clearly bearish dynamic.

Yet even having made a couple dollars on the way down, I still gave up a lot of gains from the way up, as I held most of my Rex shares from $105 to $90 and my core position in Pacific Ethanol from $23 down to the $18’s. Its a frustrating conclusion, but truth be told I did not expect that the price of ethanol could fall this far this fast. The California price currently sits at $1.85 per gallon, which is down an astounding 65c from the $2.40 level its traded around for the last number of months and up until the last two weeks.

What can you do? I wasn’t being particularly greedy, I was merely taking profits in my usual manner, peeling them off slowly a little bit each day. Little did I know that a tsunami was right around the corner.

Yet I don’t think I am done with these stocks just yet. I’ve listened to the Green Plains second quarter conference call multiple times, and I’ve listened to both Green Plains and Pacific Ethanol discuss the current market dynamic during their presentations this week at the Imperial Capital Renewable Energy Conference. I would recommend in particular listening to the Green Plains presentation (available here). Its clear that exports are going to play a big part in the fourth quarter. I suspect that some, if not much of the inventory being built is in advance of exports expected to be shipped in the coming weeks. Green Plains alluded to this during the Q&A. I also wonder how much ethanol is being moved now ahead a rail car backlog that is bound to erupt once harvest comes into full swing.

The bottom line is that ethanol capacity right now is 14.5 billion gallons. To maintain the 10% blend somewhere between 13.5-13.8 billion gallons has to be consumed in the United States. Exports are expected to average between 800 million and 1 billion gallons this year, and the strong demand in the first quarter and what is expected in the fourth quarter backs that up. To think that we are suddenly experiencing an ethanol glut doesn’t make sense, especially considering that the price in the United States is far cheaper than Brazilian imports at the moment.

On that subject I was somewhat pleased to hear the Green Plains CEO tear apart the idea that a 3% export tax break in Brazil is somehow going to flood the US with imports. To think that was just crazy. Maybe selling sooner rather than later has turned out to be fortuitous consequence of those that panicked on this rumor, but correlation is not causation and this was simply good luck and bad logic.

As was said by I believe the Green Plains CEO, the ethanol market operates Wednesday to Wednesday, from EIA report to EIA report. Thus there is probably no rush to step back into these stocks until they are truly washed out. We still are a couple of weeks away from the fourth quarter when exports will begin to pick up. And a continuation of the current spot price would imply far lower margins and stock prices for all the producers. But if it begins to appear that the build in inventories this week was an anomaly, or that export volumes are going to make it difficult to continue to build inventories through the winter, then I plan to step back into my positions.

Non-ethanol Developments

The last few weeks I have spent the majority of my research time trying to figure out the ethanol market. That has left little time to investigate new opportunities. With my ethanol positions sold early in the week, I spent some time screening stocks and delving into names that looked promising. Unfortunately I didn’t find anything that blew me away. Here is a list of the one’s I did find and that I plan to follow and look at more closely in the coming weeks. There is no guarantee that I will initiate positions in any of these names. Please email me if you have insights on any of them:

- VSE Corp

- Silicom

- Twin Butte Energy

- Ellomay Capital

- Com Dev

- Reitmans

- Moduslink

A New Position

I did add a new position to the portfolio a few weeks ago. Dixie Group (DXYN). They manufacture mostly high end flooring, with a focus on carpets. This is the sort of company for which I typically get needled about when I mention my investment on twitter. Someone inevitably points to their lousy history of operating profits, the lack of free cash flow generation, basically how this does not fit the value mold that we know all stocks have to fit to be called an investment.

I’ve gotten tired of the back and forth as it does not uncover anything new so I have stopped tweeting about these positions in any detail. Let me just remind you that there is a reason that the chosen title of this blog is Reminiscences of a Stockblogger. Jesse Livermore was no Benjamin Graham. He was probably richer.

The fact is that I invest on the expectation of change. I rarely look at an opportunity where the thesis is based on a continuation of the way that things have been in the past. While the linear analysis might work in the long-run I haven’t had much luck outperforming when I have tried to apply that that concept myself.

Looking for change means that you have to go out on the limb and predict something different than what has happened in the past. It means you are going to be wrong. Another characteristic I get chastised on is that I am so ready to change my opinion, or even to change my position without changing my opinion. There is out in the investosphere a consensus that a good investment is a good investment is a good investment, and that once conviction is made it should be held indefinitely. That might work with some strategies, but I think its a death knell when your ideas are based on the expectation of change. You have to accept you might be wrong.

With that said, the change that may be underway at Dixie Group is an improvement in operating performance that will lead to a decent level of earnings. The company has been putting out about a 0-2% operating margin for as far back in the financials as I was willing to go. Now they think that they can improve the business and eventually run at an operating margin of 7%. A look at the other public companies in the space (Mohawk, Interface) suggest that they should be able to operate at 7% if they get their ducks in a row. And with some of the recent acquisitions they are more leveraged to the commercial construction business than they have been in the past, which should be at a tailwind at this point in the cycle. If I’m right and they can get their operating margins up the stock should be able to levitate to something around $20 based on a 10x EV/EBITDA that would still put them at a slight discount to their peers.

Like most of my ideas, if the thesis doesn’t look like its going to work, I’ll cut my losses and run. I’m not going to pretend that I know Dixie’s business well enough to have “confidence” that they will turn it around even if the evidence piles up to the contrary. But if I’m right, its another 2-3 bagger from here, and that makes the risk/reward attractive in my opinion.

Speaking of Cutting Losses…

I sold out of a few stocks since my last update, of which a couple I was slower to cut losses than I should have been. First, I sold Palliser Oil and Gas, which has been an absolute disaster, with the only saving grace being that my position was not very large. The company recently announced a transaction that will infuse cash and has bumped up the share price to something a little less dismal, but when I looked at Twin Butte Energy this week, which is undoubtably a better company, it was hard to justify holding Palliser if I wanted heavy oil exposure.

I also sold out of Lojack. This is one of those situations where I might regret selling; the turnaround seems to be always just around the corner and inevitably the corner will come now that I have walked away. But I’m down 25% on my purchase which is more than my usual soft stop loss limit, I don’t really have any concrete evidence that the thesis is playing out positively yet (the TomTom relationship has produced lots of qualitative commentary but very little in the way of actual, known customers). So I’m out, I’ll follow the next quarter closely and if it looks like they are gaining traction maybe I’ll get back in.

Finally, I sold out of Midway Gold. This has nothing to do with the company, which is making solid progress on all its projects. But gold prices are not good and as we all can remember the lessons from 2012 that A. it only takes 1 day to drop gold to the next level down and B. by the time that happens its too late to get out. I did pretty well on my four forays into gold stocks, having returned about 20% on Midway in the last 3 months, after booking similar returns (on average) from Endeavour Mining, Rio Alto Mining and Argonaut Gold. Another opportunity will come but I don’t think that time is now.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

What are your thoughts on Aercap?

I read on twitter that its a bit of a hedge fund hotel. One manager that tweets and seem to have a big following said he was shorting it at $48 because he thought the funds that owned it were weak hands and could be shaken out. I think we’re just seeing that shaking out. I still hold it, havent added but am waiting for it to eventually get above $50.

what do you think of sherritt at current levels especially given that Nickel price has come down below $8?

I think the idea still makes a lot of sense but its not really working is it? I’ve cut back a little, but I still am holding. I hope its just delayed but the drop in nickel and the continuing rise in inventories is a bit disconcerting.

Re Reitman’s, the Contra the Hear guys have bought if you didn’t see:

http://www.contratheheard.com/cth/contraguys/140404.html

No I didn’t know that, but Benj Gallagher sometimes has some good picks. Thanks for the link

Fairfax is a big holder too, so between Contra and Fairfax, you’ve got a couple of very strong bottom fishers in there.

Personally, I am avoiding anything retail these days as I think competition from the internet and all the US retailers coming to Canada is too high, but I can see why people like this down at current prices.

Its anecdotal but my Mom went into Reitmans the other day and for the first time in a couple of years said there were decent clothes there

I’m in Twin Butte and Com Dev Lane, although too early on Twin Butte and hanging on now on the chance it may be turning into a takeover candidate and as the dividend is still generally regarded as sustainable. Com Dev very recently based on opinions in Stockchase.com. You can get analyst snapshots on Stockchase.com – including recent commentary on Twin Butte and Benj’s recent opinions http://www.stockchase.com/expert/view/101 (searchable bycompany, analyst and top picks)

Are you still keeping the faith on Yellow? Teck is also in the bargain basement, if you are still positive on Sherritt.

Whats your take on BXE’s current action? Stock has taken quite a thumping lately, its almost at its 1 year low. Seems like the company’s botched financing and production bottle necks have negatively impacted the stock. I see good value here but wanted another perspective.

I’ve been adding to it. What you said above it true, and there is clearly some sort of sector based capital retreat going on. I’ve seen that happen before, it pulls the CDN oil stocks down and it seems like they will never stop falling and then they do stop and head right back up again. I’m expecting something similar with BXE.

Arguably something similar going on with GST (botched financing, sector retreat), though “arguably” is a dangerous word on which to start an investment…

yeah I guess it is somewhat similar. I have a lot more confidence in BXE acreage than GST though. I sold b/c i couldn’t get comfortable with repeatability of Hunton. So far they are continuing to do ok with it though.

I do think Dixie could be a multi bagger. TILE has an EV/Revenue of 1.1 times compared to 0.61 to Dixie and it is buying companies much lower than that (Burtco at 0.23 and Atlas at 0.32). My main concern is that this is an old management with low ownership and a new margin expansion plan.

Its true. I would give success higher probability if it wasn’t same ole same ole as well. Where did you get the Burtco and Altas metrics from? I looked around for Burtco info the other day and didn’t find much.

This is one of two articles:

http://timesfreepress.com/news/2014/sep/25/dixie-group-buys-burtco/

I couldn’t find the other.

With regards to the margin expansion, we should see gradual evidence (or lack of) very soon. In the latest conf, CEO and Chairman said “I think in the first half of 2015, we will still have a fair amount of restructuring. We will be shutting down our rug operation and moving into a building we already own, which is the last piece of that integration. And so I expect we would probably achieve that would be in the latter half of 2015.”

I think the sell-off at AER is more sector related than the weak hands theory. ALL competitors AYR, AL, FLY,…were down around 12%-15% since mid-summer. That usually happens when people starts talking about raising rates… but in some degree air lessors are protected. AER has 82% fixed rate debt, another 5% is covered with derivatives, some of their contracts with airlines include price increases in the case that rates go up, their average debt maturity is around 2020 and after.

what really matters is the type of airplanes, supply/demand of those airplanes , airlines solvency, utilization rate, ROE, scale. AER scores well in this metrics

in 2006-2007 with rates much higher some of this companies traded even for 20x earnings… i think at 8x fwd earnings in AER is a good investment.

Thanks for the comments. Those are all good points.

Well, figured out the reason for the nice move in TRZ.B this week. Looks like Ross Healy can still move stocks as he had it as a top pick on Market call again this week on the 23rd and the stock immediately took off (look at an intraday chart). Says seasonality is great from October into year-end almost every year, even in bear markets. Looking for 25% to 30% upside, so say $11.00.

http://www.bnn.ca/Video/player.aspx?vid=448589