Week 189: Playing the oil trade from all angles

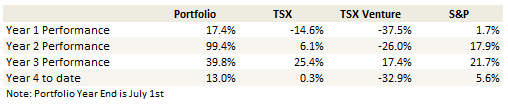

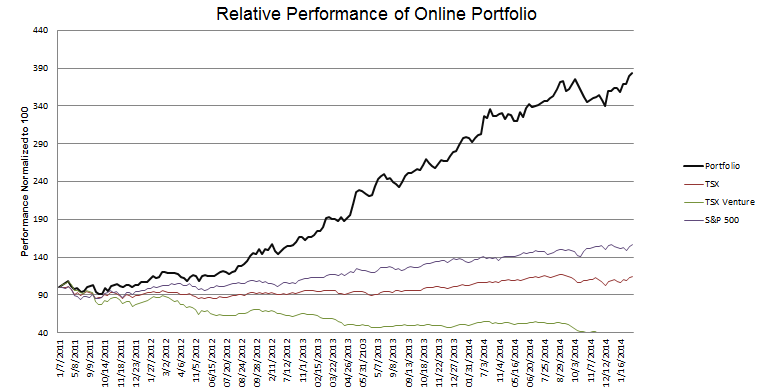

Portfolio Performance

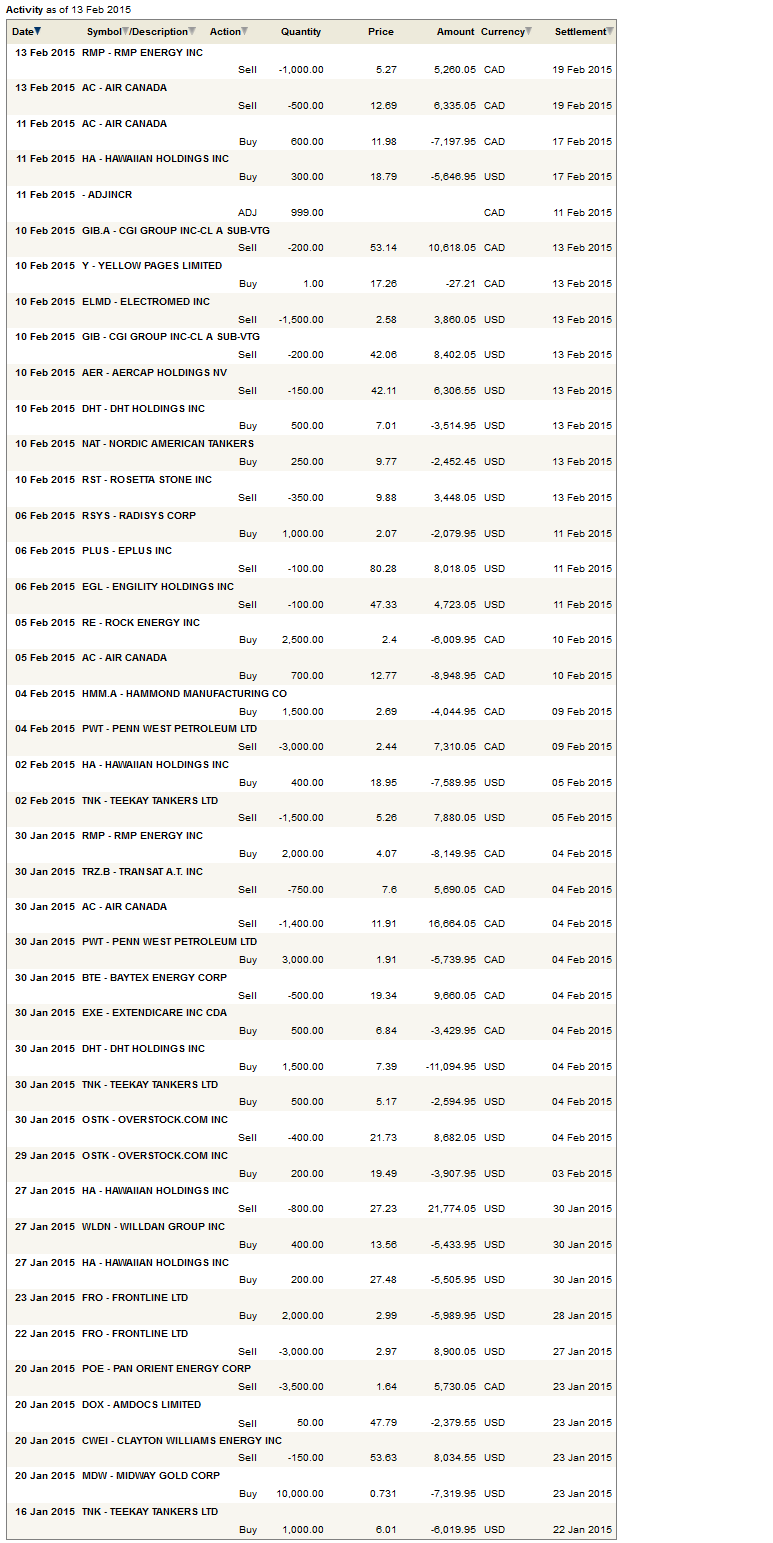

See the end of the post for the current make up of my portfolio and the last four weeks of trades

Updates

One of the themes over the last few months has been a shift in methodology towards taking what I can get. Less have I been holding out for the big gain, and more have I been booking 10-20% gains when they materialize.

The change arises from my confidence, or lack thereof. I know we are in a bull market and still at all-time highs but it doesn’t feel like that and so I remain somewhat cautious. I’m just not comfortable waiting for upsides to play out in full. So I take what I can get.

Sticking with the Airlines for now

This business of scalping, for lack of a better term, worked quite effectively with Hawaiian Holdings. Leading up to Hawaiian Holdings earnings report on January 29th I held a fairly large position. But believing that caution is the better part of valor, I reduced that position to its shadow in the days leading up to the earnings release. The stock was subsequently pummeled after reporting lower guidance than anticipated. While I still took some lumps, it was not nearly to the degree it would have been and I was left to decide where to go from here.

After much review I decided to add back, at least part way. Here’s what I think. The stock was hit because their revenue per average seat mile (RASM) is being squeezed on a couple of fronts. First, on their Asian destinations fuel surcharges are shrinking down to nothing because of the drop in the price of oil. Second, the strength in the US dollar is hurting their competitiveness to book flights from Asia; naturally the majority of Hawaiian’s customers on their Asian routes are traveling from these destinations and flying to the US: Hawaiian’s US dollar cost structure is hurting them here. Third, the company said that North American capacity would be at a record high this year, with capacity growth peaking in the first half and this would put some downward pressure on prices.

The bottom line of all of this is a year over year total RASM decline of 3.5%-5.5% in the first quarter (including 3% that is attributable to currency and fuel surcharges). I think that the market looked at that and said, whoa that’s a lot of headwinds for a stock that is up some 100%+ in the last year, and promptly sold it off.

While it’s a fair assessment, they are a lot less of a concern now that the stock is down some 30% in the last few weeks. What is easily overlooked is that all of the negatives are more than made up for by the drop in jet fuel prices. Using the company’s 2015 fuel guidance I calculate that the savings will be $230-$240 million for the entire year. That is over $4 per share.

If the experts are right and oil prices are going to stay in the $50-$60 range for 2015 I simply do not see how a company like Hawaiian Holdings, or for that matter the other airline stock I continue to own, Air Canada, will continue to trade at such low PE multiples. I have based this discussion on Hawaiian but I could have made similar arguments with Air Canada, with the primary differences being different events leading to a perceived earnings miss (in Air Canada’s case it was employee benefits, adjustments to pension assumptions and a lower Canadian dollar) and that the stock has quickly gained back its losses. But Air Canada, like Hawaiian, will see gains from the lower price of jet fuel that far exceed any currency or revenue headwinds they encounter.

Getting back to Hawaiian, using the company’s guidance leads to earnings of about $2.75 per share. Do they really deserve a mid-single digit multiple in a market where the average multiple of an S&P stock is somewhere north of 20? I feel like the upside potential is, as they say, asymmetric to the downside risk.

The downside risk, of course, is that the price of oil rises significantly. While this is something to keep a close eye on, particularly with disruptions in Libya and Iraq, I feel well hedged by the oil stocks I own in my portfolio. My positions in RMP Energy, Mart Resources, and my recently taken position in Rock Energy will all do very well if the price of oil spikes. And as always, if things start to go south, I plan to exit my positions quickly to limit my losses. But I don’t think I will have to. I think this is probably at least a somewhat new paradigm for oil, which means its also a new paradigm for the airlines, something that even with the run up in the fourth quarter last year I don’t think the market has fully appreciated.

New Position: Willdan

I got the idea for Willdan from a couple of SeekingAlpha articles that outlined the investment case for the company (here and here).

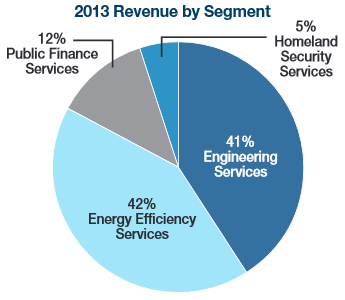

Willdan provides consulting services. They separate their business into four segments: engineering services (Willdan Engineering), energy efficiency services (Willdan Energy Solutions), public finance services (Willdan Financial Services) and homeland security services (Willdan Homeland Solutions). Of these, the energy and engineering services make up the bulk of the revenue.

To get a sense of the sort of consulting Willdan performs, its worth taking a closer look at a few of their contracts. In 2009 Consolidated Edison awarded Willdan with one of if not the largest contract, $67 million to perform the role of “program implementation contractor” for an energy efficiency program directed at small businesses. The contract was extended in August of last year. Willdan’s role as contractor includes:

To get a sense of the sort of consulting Willdan performs, its worth taking a closer look at a few of their contracts. In 2009 Consolidated Edison awarded Willdan with one of if not the largest contract, $67 million to perform the role of “program implementation contractor” for an energy efficiency program directed at small businesses. The contract was extended in August of last year. Willdan’s role as contractor includes:

providing outreach to small businesses, completing on-site energy efficiency surveys, implementing energy-saving projects, and partnering with the community and local businesses.

As another example, Willdan provides engineering services to the city of Elk Grove California. After a bit of investigation I found that the services Willdan provides are things such a road construction and repair, drainage construction, lighting design and maintenance and traffic engineering. Basically all the civil engineering tasks that one would associate with maintaining a city.

So this gives you an idea of what Willdan does. Its probably not a bad business, not terribly reliant on the economy, but not really much of a moat beyond the skills of the individuals you employ who do the work for your customers.

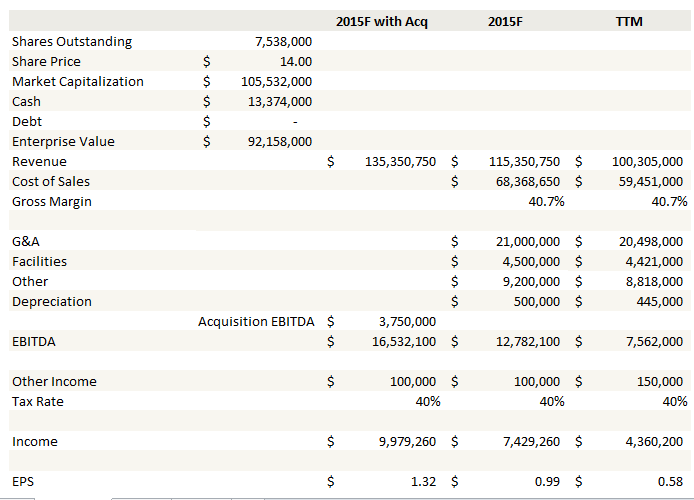

Willdan is a small company, trading at a market capitalization of about $100 million. When I first stepped through their historical results, Willdan looked somewhat interesting to me but I could have easily passed. But what caught my attention were two recent acquisitions for $21.2 million. Both of these businesses are complimentary; typically Willdan provides energy audits and consulting but does not perform the engineering services for energy efficiency projects; these companies will expand that offering to the latter. The businesses also expand Willdan outside of their core areas of California and New York and into the Pacific Northwest and Midwest.

So Willdan benefits on two fornts: they can expand their energy services auditing into new territory, and can market the engineering services of the new businesses within their own operating regions, presumably for energy efficiency audits they already have under contract.

On the conference call to discuss the acquisitions management said they paid 4.3x EBITDA for the guaranteed portion of the acquisition price. The acquisition structure is tiered, by which Willdan pays 60% of the price (about $12.7 million) up front, with the balance contingent on the performance of the acquired businesses. In particular each business has to grow operating earnings by 25% to obtain the full payment. It seems to me like a great structure for Willdan.

The acquisition price implies that businesses are generating about $3 million of EBITDA in the trailing twelve months. Before the acquisitions Willdan said they could grow their top line organically by 15% in 2015. Below is a rough estimate of earnings per share assuming that Willdan achieves their top line growth, maintains their existing margins, and that the acquired businesses perform sufficiently to achieve the full acquisition price.

Its not unreasonable to assume that a company with $1.30 earnings and a growth profile over the last few years would be given a multiple of greater than 10x.

Its not unreasonable to assume that a company with $1.30 earnings and a growth profile over the last few years would be given a multiple of greater than 10x.

This is a small company and small position for me, and not one I am likely to add to. I think there is a decent chance I will make a few bucks on it as it has a run to $17 or $18 or if I’m lucky even $20.

One new Energy Position: Rock Energy

As I mentioned in my last update, I had been in and out of Penn West a couple of times during the first month of the year. I held Penn West for perhaps the last time a couple weeks ago when I bought the shares for a little under $2 (Canadian) and sold them at $2.60. Regretfully I sold much too soon, the stock kept roaring all the way up to $3.30. But consistent with my theme this month and with the thesis I presented in my last update, the nature of my purchase was a short term scalp and to stray from the nature of my intent would have been little better than a blind gamble.

But having some conviction that oil prices have hit bottom, and as I mentioned already, having an eye on the production shut-ins in Libya and Iraq, I did peruse the energy universe for other names that I might want to take a position in. I am by no means convinced that oil prices have bottomed, we may have, may not have. Thus I was looking for companies that could weather a continuing storm but still pose a decent upside to a stabilization in price.

A lot of the stocks I looked at had gone too far too fast; reviewing Baytex, Suncor, the larger Canadian names, and they all seemed to be already pricing in an oil recovery. Ditto for smaller names like DeeThree Energy, which I should have been looking at $2 ago. Others, like Penn West and Lightstream, certainly have a lot of upside if a truly bullish scenario develops, but they run too much risk of a big drop on some bad news event driven by lenders getting skittish. I don’t want to have to worry about that.

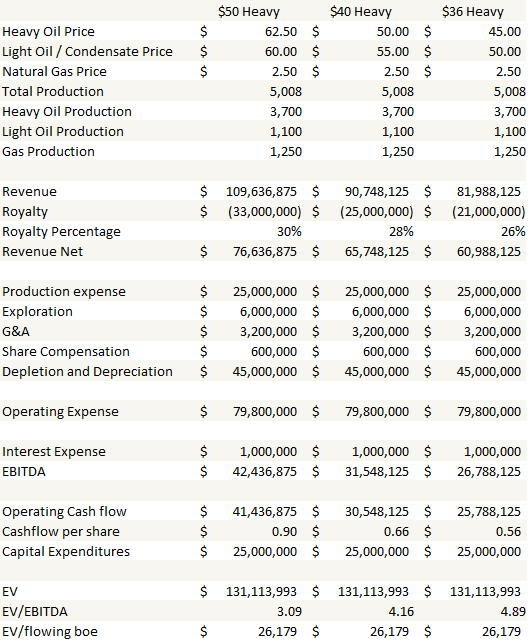

I settled on Rock Energy, a name I used to own at prices not far off what I bought it for now. Here are the reasons I like Rock:

- Their debt is nearly non-existent at $20 million as of the end of third quarter and now, after a recent $13.2 million bought deal (done at $2.32 per share) debt is even lower. There is no question that this company survives.

- Rock revised their 2015 guidance and cut capital expenditures to the bone, to $25 million for the year, down from their original guidance of $90 million.

- At an average price $40 USD WCS, with a US/CAD exchange rate of 1.25, they will generate $35 million of cash flow for the year, more than covering capital expenditures.

- At this low level of capital expenditures the company would exit the year at somewhere in the neighbourhood of 4,600 boe/d. That values them at $28,000 per flowing boe upon exit.

The sensitivity analysis I did below shows how the company will cover its capital expenditures even at current WCS prices and illustrates the upside to an increasing oil price.

Rock will rise when the price of oil rises. If the price of oil does not rise, Rock will flounder, but I doubt it will crash much further.

Hammond Manufacturing

I’ve been on the look-out for Canadian manufacturers that stand to benefit from the dramatic fall in the Canadian dollar. I haven’t had a lot of luck. There aren’t a lot of manufacturers left in Canada, and most of the big one’s move dramatically in November, anticipating the move, and I wasn’t quite so quick to the trigger.

However I did find one overlooked name a couple weeks ago. Hammond Manufacturing. Hammond is engaged in the heavily moated business of electronic enclosure manufacturing. I’m kidding of course, but when your business is one of commodity manufacturing there is little more that could be asked for than for a 20% currency devaluation to bring down your unit costs.

Hammond is a pretty simple story so I’ll keep this short. The company manufacturers electronics enclosures, so racks, cabinets, wire troughs and a few more technically complicated items like air conditioners and heat exchangers. They manufacture these products in Canada (Guelph) and thus they incur their costs in the Canadian dollars. That means their costs have declined significantly of late, and that puts them at a competitive advantage. The company is expanding production to meet the increased demand brought on by what is likely increasing market share.

The stock is also cheap. Looking back at the trailing twelve months, at the current price the stock is at 6x free cash flow. That free cash flow is going to decline in the upcoming quarters as the company looks to expand their business which means an increased level of capital expenditures. I think there is a reasonable chance that capital translates into meaningful growth, and in turn, a higher stock price.

The Tanker Trade – DHT Holdings

I have remained patient with my position in Frontline even as it sank significantly from my original purchase. When the stock hit $2.90 I reluctantly reduced because it had crossed my 20% loss threshold. I held onto the rest as it sank further and subsequently added back as it recovered. The thesis still seems intact and my position sizing is not so big as to make me uncomfortable with the wait for it to play out. In addition to Frontline I continue to own Nordic American Tankers (which I mistakenly referred to as Navios Marine Acquisition Corp in my last update).

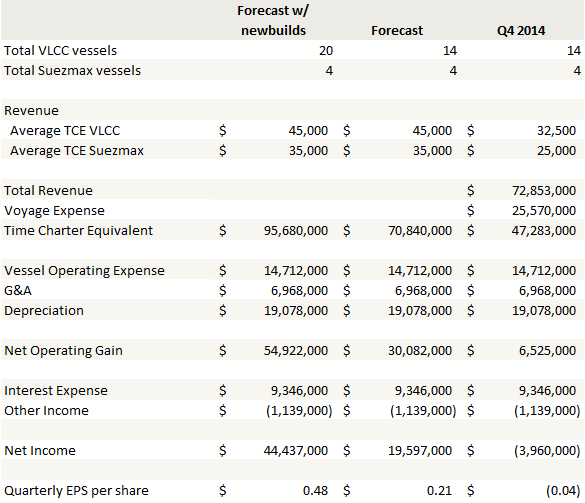

I added another name to the trade a week ago: DHT Holdings. DHT is a bit safer way to play the thesis, insofar as any of these stocks can be considered safe. Their ships are newer, they have a number of new builds scheduled for delivery over the next two years, they do not have the debt overhang, and with ~60% of their ships on the spot market they still stand to benefit from improved rates.

DHT has 14 VLCC tankers and another4 Suezmax tankers. There are another 6 VLCC new builds that will be delivered over the next two years. When I look at DHT’s earning performance at rates even slightly below today’s level, I am left to conclude there is significant upside in the stock if the thesis does play out as I expect.

A couple of weeks ago I posted Teekay Tankers monthly update video onto twitter. It is available here. In the video it was noted that supply growth over the next year or two for the three classes of ships used for crude transport (VLCC, Suezmax and Aframax) is non-existent. Meanwhile demand is expected to increase, including further pressure given the fall in the price of oil, and a number of VLCC tankers are being taken off the market for 1 or 2 years for storage. I think that what we have seen over the past month is a short attack on the tanker stocks from those that believe we are seeing a repeat of last year; a brief spike in rates that will soon be followed by a collapse down to marginal levels. What I think the shorts are failing to realize is that the dynamic is quite different then last year. Indeed as we move through February you are not seeing significant weakness in rates and as a consequence the tanker stocks are being to firm up again. I suspect (and am anticipating) that this is the precursor for another move up.

Scaling back on US names

I sold out of a number of positions in the last month, most of them for reasonable gains. Included on this list was Engility Holdings, Rosetta Stone, CGI Group, Electromed and ePlus. Each is an excellent illustration of the scalper trade in action.

Of the group, I most reluctantly sold out of CGI Group. I think there is a decent chance it continues to trade higher. But I also note that they are predicting somewhat weaker results in the first half of the year, followed by strength in the second half, they may experience some currency headwinds with the Canadian dollar falling, because they trade in the US and its not clear to me whether it is the Canadian or US ticker that determines the price they may also face share price headwinds if the Canadian dollar rises, and they simply aren’t as cheap as they were when I bought them 20% lower. But really, my primary reason for selling the stock is because when I bought it I assessed that there was an easy 20% of upside but that my outlook was cloudy after that. I’ve gotten that first 20%, so to hold on without a change in thesis feels like a bit of a gamble.

I was pleased with the results from ePlus but surprised that the stock took off to the extent it did after earnings. Shares were up nearly 15% at one point. Much like CGI Group, ePlus is coming up on weaker seasonality in the next two quarters. Also much like CGI Group, the discount I saw originally has been eaten up with the 20% gain in the share price. Were I convinced we were in a bull market I may have held out for another leg up. I’m not so sure though, so I just took my profits and walked away.

I spent a lot of time thinking about Rosetta Stone. You can read my comments on a couple of short articles that were posted on Seeking Alpha. I finally sold out of the stock for about a 10% gain and with some reservations about whether I am doing the right thing. I still don’t really buy the short argument. But I also didn’t feel confident enough about the business to hold the stock through its fourth quarter results. I think the fourth quarter is going to be good; seasonally it is the best quarter by far. I’m less sure about guidance.

My actual 2014 portfolio performance

As I have noted before, I write this blog based on the performance of a tracking practice portfolio that is made available from RBC. This portfolio is intended to mimic the general trend of my most risky investment portfolio. However the practice portfolio has some limitations, in particular that you can’t short stocks in it and you can buy and sell options. Every year I try to give a quick update on my actual portfolio performance as comparison. In this last year the gap between the real portfolio and the one I track here was a bit bigger than usual, and mostly for a single reason: Pacific Ethanol. In my actual portfolio, when given the fat pitch that was ethanol back in the early months of 2014, I not only loaded up on Pacific Ethanol stock but on options as well, with the result being very large gains on the calls. Thus below, you can see the discrepancy between my more speculative account, where the options were bought, and the more restricted retirement account where you can only buy stock. I had a pretty good year in my retirement account, but my investment account flourished particularly well thanks in large part to our good friend Pixie.

Portfolio Composition

Click here for the last four weeks of trades. Note that the name change of Yellow Media to Yellow Pages removed that ticker from the practice account so there are a couple of transactions there to add back the 1,000 shares that disappeared.

{kind=link}

what are the red bar and the brown bar in the graph you posted?

Those are my portfolios.

Lsigurd, Thanks for the update.

Being in Canada have you looked at MBA.To (MBAIF)? Someone has taken a big position on my website and has me interested. Wondered if they crossed your path. Interesting story.

http://www.vancouversun.com/Downtown+hotel+converting+housing+foreign+students/10781986/story.html

http://globalnews.ca/news/1808165/former-downtown-hotel-to-become-luxury-dorm-for-international-students/

Here’s a reply to one of our members from the CEO;

http://www.joestocks.com/forum/showthread.php?667-Member-Twepps-JANUARY-2015&p=40910&highlight=mbaif#post40910

I’ll start looking at it. Its a pretty big purchase for a small market cap isn’t it?

Here is a promo fact sheet.

https://drive.google.com/file/d/0BxeV9p_u5AOUeG1Lb1d0ck54NDg/view

Also…You use to be in JONE. I am intrigued by the private placement at 10.50, and the public offering at 10.25. Also, the $250mil senior unsecured private placement. Looks like they took strategic steps to shore up their balance sheet and hold some dry powder.

“Organizations with the liquidity to capitalize on opportunities have a significant advantage in low commodity price environments,” said Jonny Jones, Founder, Chairman and CEO of Jones Energy. “We are pleased to welcome Magnetar and GSO as strategic investors. This deal further solidifies our capital structure and allows us to execute on our long-term growth plan while providing us with the flexibility to take advantage of any opportunities that may arise.”

Thoughts?

I thought it was interesting too. i think JONE is a decent company. Every time I write about them I get crapped on by the same folks but I think they seem like good operators, good acquirers of acreage. Only thing is they are fairly dependent on NG and NGLs and its really tough to get behind those commodities right now. NG production is just so high. But that said I haven’t actually done the work to see how levered JONE is to changing NG and NGL prices or whether they are more levered to oil now, especially after the changes to their frac design that is getting more oil out. Maybe I am making a mistake not looking more closely. Wouldn’t be the first time.

Wouldn’t you say that Hawaiian has a much better business model then Air canada? They are one of the few airlines with a moat, with their interisland segment. They seem to have a low cost advantage there, also judging by past results.

Seems like Air canada is simply experiencing cyclical tailwinds now, and can easily go back to earning next to nothing a few years from now.

Doesn’t HA have a better moat with their interisland segment then air canada? Could be that Air canada is just in a cyclical tailwind.

Could be that earnings will crash down for Air canada 2 or 3 years from now.

Whats the reasoning for selling Transat? I couldn’t find it in your notes.

Yeah you know I never realized I didn’t mention it. I thought I did, I guess I just overlooked it. So I sold the stock because I think the weak CDN dollar is going to make Q1 and Q2 difficult. They also hedge fuel so in the very short term they are going to be hit by the dollar over the winter but not going to gain from fuel to the same extent yet. The winter routes also have a lot of added capacity from Air Canada and such so that is making it more competitive.

I still really like transat though in the medium term. I think once we get Q1 released I will look to adding it back, because the summer is going to be stronger, they will begin to benefit from fuel more, and presumably the dollar will stabilize. And I really don’t know how the stock reacts at Q1 – market could look at results and send it down or look past results and send it up on summer expectations. But I am just stepping aside until that uncertainty is past.