Week 185 Just your run-of-the-mill Portfolio Update

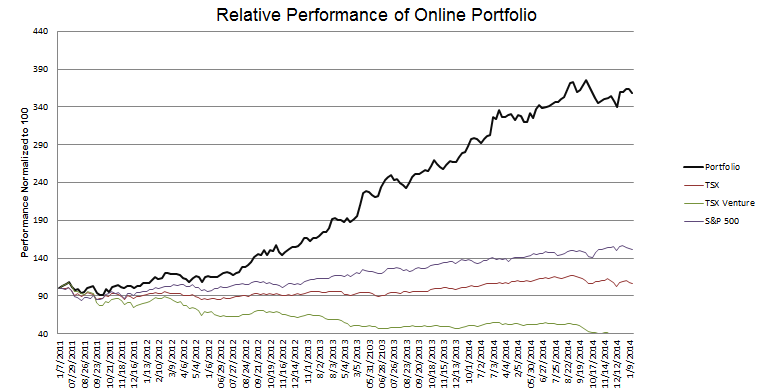

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades

I don’t have any general comments to make so I am going to get right into my portfolio updates for the last month.

The Tanker trade

The biggest moves in my portfolio have tended to take place in the first couple months of the year . In 2013 it was YRC Worldwide. In 2014 it was Pacific Ethanol. I’m hoping that this year its the tanker stocks.

Of course the tanker stocks have already had significant moves. I have been adding positions at prices that are much higher than they were a couple of months ago. But to use Pacific Ethanol as an analogy, the move from $2 to $4 was only the first act. I’m not sure if these stocks will put on the show that Pacific Ethanol did, but I am hopeful there is a second act in the cards.

I have taken positions in Frontline, Teekay Tankers, Navios Marine Acquisition Corp and Capital Products Partners. Of the four Frontline is my largest position and the one with the most upside potential. At the other end of the spectrum, Capital Product Partners is probably the safest and a somewhat different thesis; they do not rely on the spot market and their appreciation will be based on increasing investors comfort with the sustainability of their dividend and dividend growth from tankers coming up for renewal in the next year that they can secure at higher long term charters.

To demonstrate the opportunity I see with the tanker stocks, lets take a look at Frontline.

Frontline operates VLCC and Suezmax tankers, which are the largest vessels used for shipping oil. A few months ago, Frontline was facing dire prospects. At the end of the third quarter they had $190 million of convertible debt due in April of 2015, a lack of cash to pay it off, and with continual losses it seemed that massive dilution was inevitable.

As spot rates have improved this has changed. Witness this excerpt from an article in Tradewinds, quoting Erik Nikolai Stavseth of Arctic Securities:

Stavseth says the current strength of the market has rapidly changed the situation in Frontline’s favour.

His number crunching had suggested the company would need to convert 50% of the bond debt and 50% of its debt with Ship Finance International and also potentially raise further equity.

“However, assuming $40,000 per day [for VLCCs] through the fourth quarter of 2014 and the first quarter of with rates reverting to our estimated $30,000 per day in the second quarter of 2015 we see FRO having a shortfall of $60m compared to our original $100m, he said in a report today.

“Should rates turn out to be $50,000 per day in the fourth quarter through the second quarter of 2015 we estimate FRO will manage to repay the CB in full without any additional equity raised or restructuring.”

VLCC spot rates are currently above $70,000 per day. Suezmax rates averaged $57,000 per day last week.

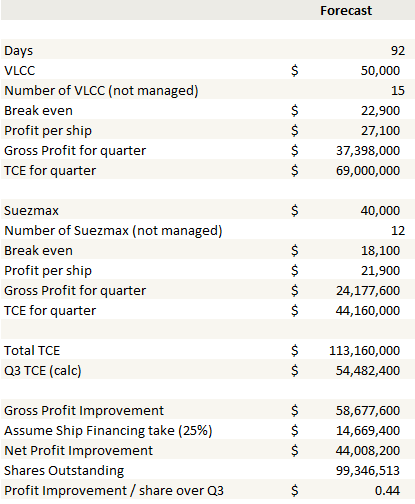

Let’s take a closer look at how the improvement in spot rates impacts Frontline. My approach will be to use the third quarter as the baseline and looking at how the changes in spot rates will lead to improved results.

Frontline owns 15 VLCC and 12 Suezmax tankers. They have another 6 VLCC tankers, 6 Suezmax tankers and 1 Aframax tanker that they manage in return for a fee. I’m not sure whether there is any upside participation on the managed ships, so I’m going to focus on the owned fleet with the following napkin calculations.

In the third quarter the average time charter equivalent, which is basically the gross margin for a ship, averaged $24,600 per day for VLCC tankers, and $18,600 for Suezmax tankers. I’m going to assume somewhat lower numbers than the current rates that I quoted earlier: I will use $50,000 TCE per day for VLCC tankers and $40,000 TCE per day for Suezmax tankers.

I’m going to use the company’s own numbers for the breakeven cost of ships and I got the owned ship numbers from their latest filing less three VLCC tankers that they terminated in November and one Suezmax that they were expected to take shipment of in January.

Another twist is that Frontline has a profit-sharing agreement with their financing company, Ship Finance International. Ship Finance takes 25% of profits above a certain baseline level. I’m not entirely sure what the baseline is for that profit sharing, but I do know they haven’t paid profit sharing to Ship Finance as of yet, so I made the assumption that the third quarter was right at the “break-even” and that any additional profits will go 25% to Ship Finance. That should be conservative.

With all of these assumptions in place:

So the net profit improvement is around $44 million for the quarter, or 44c per share.

Worth noting is that as part of the profit sharing agreement with Ship Finance, Frontline prepaid $50 million as a non-refundable deposit. Therefore the first $50 million of profit will not incur any outflow to Ship Finance. Thus first quarter cash flow will likely be higher than subsequent periods, which is good because the company has cash requirements in the short-term.

Before impairments the company lost about $15 million in the third quarter. If I combine the improvement suggested by the analysis with the third quarter result, I get earnings of around $25 million per quarter. So if rates can maintain this level, Frontline could earn about $1 per share for the year. At $3 and change and with restructuring concerns alleviating, it seems like a cheap bet.

The other positions I’ve taken are a little less speculative than Frontline. Teekay Tankers is probably the next most exposed to spot price changes. On their third quarter conference call Teekay said that 82% of their fleet was exposed to spot. This is intentional, Teekay sees a stronger spot market going forward than what they will be be able to get from time charters.

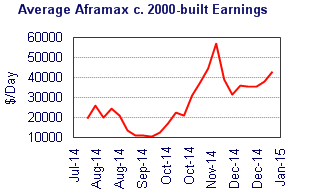

Teekay primarily owns Aframax tankers, which are smaller ships used for regional routes. They aren’t the primary beneficiary from crude inflows to Asia and are not going to be the first choice for storage. But as Teekay management indicated on the third quarter conference call, Aframax tankers indirectly benefit from the lack of competition from the bigger Suezmax and VLCC tankers that are now being used for storage and in more demand for longer routes. You are seeing that right now, with Aframax above $40,000 per day, well above where they were 6 months ago (chart from Clarksons).

Apart from the number of day traders involved in the stocks that are whipping them around by high single digit percentages, I think the biggest risk is an OPEC production cut. This would hit the tankers from all sides, reducing supply, reducing demand, likely reducing the contango which would make storage undesirable. But I don’t think that is going to happen. If it does I have some oil stocks that would help compensate for the loss.

Apart from an OPEC swan, the build schedule for all three tanker classes that I am exposed to (VLCC, Suezmax and Aframax) does not show significant supply coming on-line in 2015, and barring a worldwide recession the demand side of the picture should continue to strengthen. I think there is a good chance I do well on this trade. But these tankers are volatile stocks, and rates can change fast, so I will always hold close to the trigger.

Handy & Harman

One of the screens I have been using to find ideas of late has been to simply look at the 52-week highs. It means I have to wade through a lot of unjustified momentum stocks but the screen does pick up the odd interesting idea.

I came across Handy & Harman using this screen and soon after I added the stock to my portfolio after a pull-back.

Handy & Harman is a diversified manufacturer that operates in the following segments:

- Joining Materials – Lucas Milhaupt sells specialty metals for soldering and brazing

- Tubing – HandyTube and IndianaTube make coiled and straight length tubing

- Building Materials – OMG Roofing Products makes/markets pretty much every building product under the sun for roofing installation and maintenance (fasteners, adhesives, drains, vents, flashings)

- Kasco Blades and Route Repair Services – sells blades for the food industry and for industrial uses

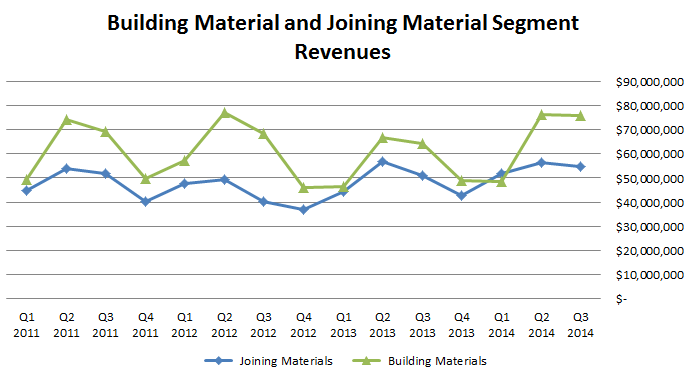

Of the four segments, building materials generate about half of the operating income and a little less than half of the revenue. Joining materials is about 25% of the business, with the tubing business being next and Kasco being a relatively small contributor.

There are a few reasons I took a position in the stock.

I got interested after noticing that Handy & Harman had just completed the sale of one of their businesses (Arlon, an electronics manufacturer) for proceeds of $157 million. This was a significant amount given that the market capitalization of the company is less than $500 million. Yet the operating income contribution of Arlon did not appear that significant, and it looked like it would be mostly made up for by the savings on interest payments if the company used the cash to pay down the debt.

Second, I thought that the stock looked reasonably priced. The company generated $52 million of operating cash flow in the trailing twelve months. Capital expenditures has been around $3.3 million per quarter this year so their free cash flow generation is close to $40 million. At a stock price of $40 the market capitalization is about $430 million, and that does not include the $217 million of cash and investments that they have on the balance sheet and that is not currently generating cash (this figure includes the $157 million they received for Arlon and an equity ownership in Moduslink). Debt is $220 million but the servicing cost of that debt is included in the free cash flow, so I believe that the effective cash generating potential of the company, assuming they can put the cash on the balance sheet to use in a similar way to what they have been able to in the past, would be at a single digit free cash flow multiple.

Third, the larger business segments seem to be picking up steam. The roofing business has posted stronger numbers in Q2 and Q3 of 2014 than it has in the last few years. The joining material business also had a good third quarter. Both businesses should benefit from an improving US economy in 2015.

Finally, the company has an active investor (as opposed to an activist investor), Steel Partners, that clearly has a strategy for them. As of year end Steel Partners owned 16,700,879 shares, or a little more than 30%.

Steel Partners has created a web of companies that they own interest in. In addition to Handy & Harman they own a piece of Moduslink, of which Handy & Harman has a 5.9 million share ownership position of their own. And Steel Partners owns about 40% of JPS Industries, which Handy & Harman recently made an offer to acquire.

Whether they get JPS Industries remains to be seen. JPS responded to the offer rather scathingly; there is clearly a lot of bad blood between the two companies.

So far, my position in Handy & Harman is small. I remain wary that the stock has run up quite fast and that the fourth and first quarters tend to be their weakest. But given that Steel Partners seems to be in the process of making some significant moves with its group of companies, I think its a worthwhile hold over the next couple of months to see what shakes out.

What I’m doing with oil

After flushing most of my oil positions in October I stayed away from the sector until mid-December when I made a couple of short-term focused purchases. Since that time I’ve been in and out of a few stocks (Mart Resources, Penn West, RMP Energy, Clayton Williams and in one case Lightstream) but always with my finger close to the trigger. I have been taking profits on 10% up moves and accepting small losses when the price of oil breaks down. As much as anything I am doing this to keep tabs on the market so that when it does bottom I am able to take advantage of it.

Companies like Penn West and Lightstream are either going to zero, or they are going much higher. Its that binary. Lightstream is probably the most extreme example in the Canadian universe. At a $60 oil price Lightstream has a debt to cash flow of around 7x. At current oil price I would guess this number is in the double digits. They won’t survive at this price. If oil prices recover into the low $70’s at some point in the next few months, I bet the stock is $3-$4. So its a huge range.

Penn West is in a similar but less extreme boat. Debt to cash flow at Penn West at current oil prices is 6.5x (according to RBC). If prices stay at this level for an extended period of time the company is going to have a very tough time. But a move up in prices to even $60 would likely make Penn West a $3+ stock, which is more than a 50% gain from its lows last week.

These companies are illustrative of the sector. As dangerous as they are, I think the trading upside is extremely rewarding if you can peg it right.

My personal take is that oil is going to bottom and rise faster than most are expecting. I explained my reasoning in this post. But as always, I take my cues from the market. I’m not confident enough in my assessment to risk much money and will quickly admit I am wrong if the market goes against me. So I pinball myself in and out of these names with the goal in mind of being in them, at least to a small degree, when we finally do get that solid reversal in the price of oil that signals that the trend is on the way back up.

Other names that didn’t stick

While I added a number of new stocks to my portfolio I didn’t keep very many of them. At various times during the last four weeks my portfolio included Atlas Air Worldwide, Accretive Health and Virgin America. None of these positions lasted for more than a couple of days. I’ve talked before about how I like to add small starter positions that incentive me to look more closely at the company. In each of these cases a closer look caused me to back off.

What I’m out of

I often think that the most profitable investment attribute is the ability to drop positions in the face of uncertainty. Having seen the evidence first hand, I know how hard this skill is, and I also know how painfully unprofitable it is to watch a stock sink further and further as you sit paralyzed. While I am far from perfect at its practice, I think I am better than many.

With that in mind, I dumped my mortgage servicing positions a few weeks ago. I found the regulatory uncertainty too great and came to the conclusion that I am simply not smart enough to draw conclusions. In retrospect, this was a prudent move; the collapse in the price of Ocwen stock is evidence of impact of the known unknowns. We already know that the regulators in California have subpoenaed Walter Investment for information, and Nationstar appears to be embroiled in some business with respect to forced placed insurance, so you just have to ask yourself, what shoe falls next? Maybe none, and if so these stocks will end up being the greatest buy of the year, particularly if some larger entity takes advantage of the valuation and decides to scoop up servicing rights on the cheap, but I can’t handle the volatility (or permanent loss of capital) that may happen from here to there. I took my small loss and moved on. There is always a bull market somewhere – this isn’t where.

I also exited my gold stock positions – too early I might add. But that’s how it goes. I bought Argonaut Gold at $2, doubled down (after much consideration) at $1.30, and ended up selling it for a 45% gain at $2.45. I bought Timmins Gold at $1.10 and sold it $1.30 two weeks later for a 20% gain. Gold stocks are always a trade, and for every one of the big secular moves up (which this may or may not be) there are 10 small swings that you miss if you keep holding on for the big one. Maybe this is the big one and I will have missed out. If not, I’ll probably be able to buy these stocks again at an attractive price in a few months.

I also want to discuss a couple of other companies that I did further work on in the last few weeks, Rosetta Stone and CGI Group.

Rosetta Stone

For a while last year I was having my articles posted on Seeking Alpha. I have decided to stop doing that. The reason I’ve stopped is because I do not like the certitude that needs to accompany a Seeking Alpha article.

Having unfailing conviction in a position is not my modus operandi. As I described above, I can see value in not knowing everything about a stock. The crumb of uncertainty keeps my positions right-sized and helps me cut losses faster.

Rosetta Stone had two negative SeekingAlpha articles (here and here) come out on it in the past two weeks. The first of the two articles is by far the better one, and it raised some good points around deferred revenue. The article pointed out that the increase to backlog that we’ve seen from Rosetta Stone may be a result of the company’s focus on 3-year contracts in its enterprise and education business (the part of the business where Rosetta sells its enterprise solutions) and not because of increased uptake by customers.

I get the math behind this and indeed the company said in its third quarter 10-Q that:

We have seen a decline in renewal rates from existing Global Enterprise & Education language customers while Global Enterprise & Education language bookings are increasing, primarily due to the sales of multi-year deals

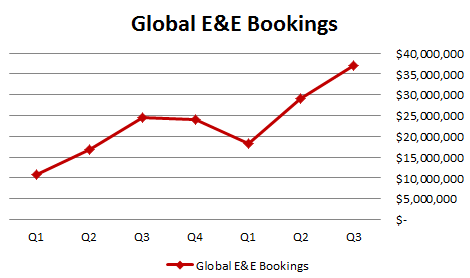

I waffled back and forth on whether this point warranted reducing my position but in the end I’ve decided to hold on. First, the trend in Global E&E bookings is strong. Here are bookings over the last seven quarters:

Second, the multi-year deals that the company is signing are with new customers. The sentence that immediately follows the last one quoted is instructive:

Second, the multi-year deals that the company is signing are with new customers. The sentence that immediately follows the last one quoted is instructive:

With Global Enterprise & Education language bookings increasing, this means we are seeing an increase in bookings from new customers, which has a higher cost of acquisition when compared to the renewal of an existing customer.

Third, that company’s are willing to make a three year commitment to the product is unquestionably positive.

Fourth, there has been disruption from the Tell Me More acquisition that has been contributing to lower customer renewals. From the third quarter conference call:

After a softer first half in terms of renewal rates, we saw renewal rates rise in the third quarter. For the fourth quarter, we’re expecting renewal rates to increase again.

Rosetta Stone is a good example of a company I own where I am optimistic about the bull case but cognizant of the bear case. Being a SeekingAlpha writer forces you to keep your feet firmly entrenched in one camp. I am going to stick to the blog format from now on, where I can say what I think and be as wishy-washy as I need to be.

CGI Group

I also spent time reviewing CGI Group. My intent was to decide whether I would add to the position or keep it fairly small. I decided to add.

The essence of my investigation was evaluating the short thesis on the stock, as presented in a few Seeking Alpha posts (beginning with this one) from early last year. The short thesis is that CGI has been goosing their earnings by clever accounting. The author contended that they are massaging their receivables to keep a bank of earnings they can use when they miss on a quarter, that they were overstating their operating cash flow by holding back cash outflows to employees via compensation and by factoring receivables (selling product/services for lower cost to generate cash), and that organic growth had been negative since 2011 and that acquisitions were being used to obscure this fact.

This is a case where I don’t really have a strong disagreement with anything the author says. He makes some valid points and he may be right about some of his claims. I just don’t think that it matters that much.

First, since the time the articles were written the company has shown that it can grow organically, as they did so in 2014 (revenue grew 4% while adjusted EBIT gre 26%).

Second, I’m not sure that the focus on organic growth is a relevant indicator. For one, the last four year period has been a difficult one, particular for the US Federal government of which CGI has a reliance on. An improving economy would make the past not indicative of the future. As well, the company’s strategy is to leverage its free cash into acquisitions that produce growth. Whether growth is coming from internal capital investment or from external acquisitions is not terribly important as long as it is accretive to shareholders.

Third, the bottom line is whether the company is generating cash flow. And they are. Excluding integration related costs the company generated about $1 billion of free cash. That puts them at about 12x free cash flow.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

What’s your take on SPCB?

Just what I wrote in the post where I sold it.

Any thoughts on FRO after the selloff?

I had to reduce after it hit my stop. I’m still holding a small position and the fundamentals havent changed at all but the market is telling me I am wrong so who am I to argue?

As the author of the inferior RST article mentioned above thanks for the link and glad you got out in time despite your misgivings about the bear case.