Week 241: Surviving

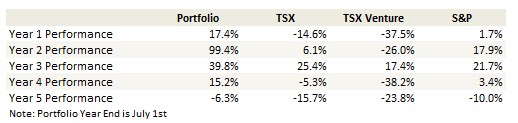

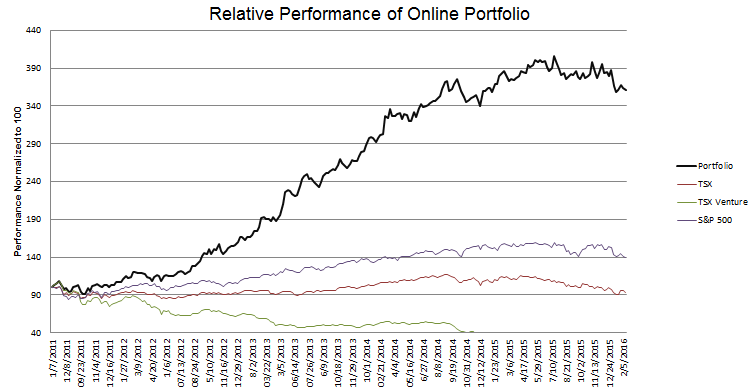

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades

I had more than one acquaintance send me news that Orange Capital was shutting down. I found this sad. Those of you that have been following the blog know that Orange Capital and myself came into large positions in Bellatrix at about the same time. The fall of 2014. Both of us saw a company with excellent assets, the potential for significant growth, and a valuation that was compelling.

Unfortunately for us, while company specific factors lined up, the macro backdrop was quite the opposite. As a consequence in the last year and a half Bellatrix has dropped from my original average cost of $6 down to, at one point, below $1 and current $1.42.

How Orange Capital and I responded was quite different. Strong in their conviction that Bellatrix had solid assets and weather the storm, Orange Capital held their position and continued to buy more. Myself, never all that sure whether I am missing some vital information, always wary of “giving it all back”, threw in the towel at around $4.50 in late November, capitulating into an interim low.

That I happened to be right in this case isn’t the point. I didn’t forsee $20 oil or a $1 handle in front of the AECO spot contract. I am positive that Orange had a better researched position than my own. That I was right was, to a large extent, just luck.

What is demonstrated though is a difference in philosophy between what I am trying to do versus many money managers. I’m not a big believer in my own infallibility. As my positions go down, I try to reduce them. I’m not perfect in this respect, but its something I try to follow.

This is a methodology that I am finding has its shortcomings in this bear market. You end up selling a lot of stock only to see bounce back shortly after. I’ve been whipsawed on a few positions.

The other point I want to discuss, which is semi-related to Orange Capital, is the topic of blowing up.

The point of existence of a hedge fund is to risk money in order to make more of it. You can argue the particulars of that statement, that risk reduction can occur through various hedges, diversification, concentration, whatever your flavor is, but the bottom line is that the money should be at risk somewhere or why is the fund even there?

But that’s not my job. While part of what I am trying to do is of course maximize my profit line, my first mandate at this point in my life is also very clearly and in capital letters, TO NOT BLOW MYSELF UP.

I see some of the funds shutting down and stories about others that are down 15 or 20% this year already. If a hedge fund is down big going into this weekend (I suspect that this is not completely uncommon and that there are many I have read about that are down far more) their primary motivation has to be to get it back. They need to make money to survive.

I am down 9% since the beginning of the year as well. But while it would be nice to get it all back, my primary motivation right now is not that. My motivation is simply to make sure that my family and I are in a position to live comfortably regardless of what happens. Whether that is 9% higher or not is really not the fundamental point. Most important, and what I guard against with absolute vigilance, is insuring that my capital doesn’t permanently disappear.

With that said, my biggest transaction over the past month is irrelevant to this blog. I paid down my mortgage in full. I also went to a mostly cash position in my RRSP (the Canadian equivalent of an IRA). My investment account, which I track here, has more risk to it at the moment than I would perhaps like, but that is because, as I tweeted on last Wednesday, I thought there was a decent chance of a rally, which we seem to be getting.

So what do I see that is making me take such a bearish, worried stance? A couple things, and I will get into those in a minute, but the overriding factor is the same one that led me to sell Bellatrix in November 2014. It simply isn’t working. And when it doesn’t work I have to stop doing it before I suffer a permanent and significant capital loss.

As for those other things, the two legitimate concerns I see are the same one’s everyone else is talking about (which is partly why I think we might be due for a rally).

- The collapse of oil bringing about energy company bankruptcies that a. lead to investor losses that start to domino into broad based selling, and b. lead to bank losses and bond losses that cause overall credit contraction

- The collapse of China’s banking system leads to currency devaluation and god knows what else. Kyle Bass wrote a terrifying piece (which I would recommend reading here) about how levered China’s banking system is, how their shadow banking system is hiding the losses, and about how government reserves are not large enough to pacify the situation without a significant currency devaluation.

Just how and to what extent these things come to pass is about as certain to me as $20 oil was in November 2014. I have no clue. But they are there, they are clearly worrisome, and what I have been doing is not working. So I have to act accordingly.

What I did this Month

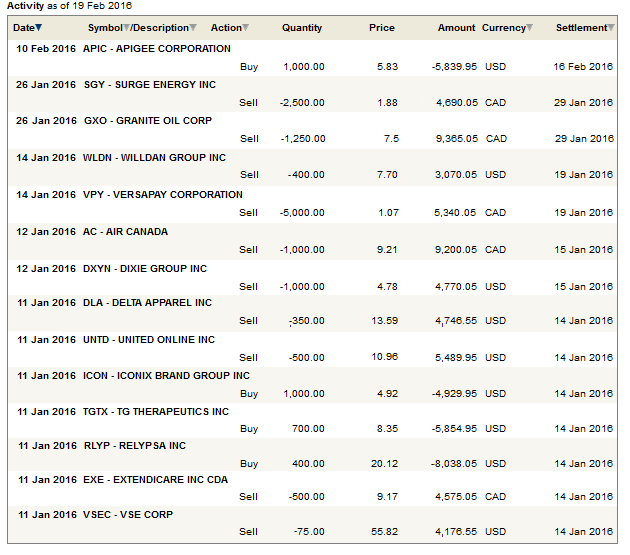

Not a whole heck of a lot. In my online portfolio I added back two stocks and sold a few other. I bought small positions back in Relypsa and TG Therapeutics a few weeks ago. I also made a couple of more buys on Wednesday of last week, adding (very small) positions in Cempra, Apigee, Five9, Ardmore Shipping and DHT Holdings (I subsequently sold DHT on Friday in favor of Teekay Tankers).

This week I added a small Air Canada position back and made two adds to existing positions: Radcom and Intermap. Radcom gave a very positive quarterly update, said that the recent contract for NFV deployment is much bigger than the $18 million originally announced and that we should expect more contracts in the second half of 2016 or beginning of 2017. I’m pretty sure this contract is with AT&T. And while Radcom doesn’t give guidance they did say they expect $20 million of cash by the end of the first half of 2016. This would be up from current $9 million. They clarified that the cash is due to new revenue not deferred payments which exemplifies how profitable the new NFV contract is. I think its quite a good growth story in a landscape bereft of them.

Intermap closed their $125 million SDI mapping contract and I don’t think the market is giving them full credit it for it. I would expect that as the money rolls more believers will jump into the stock. Intermap remains highly speculative but if they can follow up this contract with another large contract the upside for the stock would be significant, making it just the sort of market-insensitive story that I like to have in this environment.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

Great insights, as always. The link to your last four weeks of trades doesn’t appear to be working.

Thanks, its been included now.

Insightful article, thank you for posting

Thanks L! Good comments as always.

If you’d like some comfort, Kyle Bass is a complete macro tourist. Look at his 50 interviews over the past few years saying the exact same thing about Japan’s imminent economic destruction; he’s a master at taking data points, matching with absolute certainty, and then maintaining credibility despite everything moving against him.

Read Michael Pettis’s blog if you want a more realistic scenario of what’s happening in China, and less emotional baggage: http://blog.mpettis.com

Long time follower of your blog here. Great work!! What do you think of Jones Energy at this point? I’m tempted to go back but is still worried because the company’s debt situation. Will it breach any debt covenant this year? Their Cleveland break even price is just below $40 so I’m not sure why it did not spike up in the last few days like Baytex.

I haven’t looked closely at JONE in a while. The hedge book helps in 2016. They are good operators, they have been squeezing positive cash flow out of their wells. So the company has lots of strong points. Problem is the debt level is pretty high at these commodity prices. This is one where if I could see the bonds I think that would be an interesting point – are they collapsing like some others? I really have trouble with E&Ps here. When oil was $45 I’d look at BTE or any others and say ok, so the stocks are beaten up and at this oil price they can squeak out enough cash flow to weather the storm so maybe there is something here. But at $30 oil its different, I mean these companies aren’t going to make it at this price. So it feels like a real gamble as to whether the commodity rallies first or the company goes under first. Now if you really believe this price cannot continue and come the summer we are back into $40s then you are probably good with JONE, BTE etc. But what if we are still at $30? That is too uncertain for me.

Possibly of interest, this JONE insight from the very last response to a question in the comments section of a Bottom of the Barrel club post on Seeking Alpha

“Not a fan here, for 3 reasons: (1) co. [JONE] uses successful efforts accounting and has yet to book an impairment, (2) debt is high on its face compared to SE, much less to what the full cost or SEC10 value will be, and (3) much of what appears on JONE BS and IS actually belongs to 3rd parties.

With respect to (3), co. includes production, revenue, costs, etc. in the income statement based on the total owned by JONE and 3rd parties, then backs out via a one line, “non-controlling interest” item the net amount attributable to 3rd parties. On the balance sheet also, properties include 100% of JONE/3rd parties, then backs the net impact of all items out via adjustment to shareholders’ equity. Note- in doing so, the debt shown is all attributable to JONE, not to 3rd parties, so the leverage is even higher if you were to construct a “JONE only” balance sheet.” http://seekingalpha.com/article/3804816-e-and-p-bottom-barrel-club-issue-2-stocks-bondage

I may be misunderstanding his analysis but I dont think the share structure is overstating assets unless you use the low share count that you see on Yahoo Finance. The market cap on Yahoo Finance is too low, actual market cap is about 3x that I believe (I havent run the numbers in a while). As long as you use the proper share count the entire balance sheet is consolidated and accurate I think.

Good job on your sell discipline to avoid blowing up, that’s something that I need to improve on. I think you are positioned well because your IRA cash position in Canadian Dollars will rally when crude rallies eventually, and I recommend staying in cash until we figure out who the next US President will be. A globally destabilizing trade and currency war leading to a world wide depression followed by a shooting war, WWIII, is a real possibility if neo-fascist Trump is elected. The only investments one can make to hedge against the kind of turmoil he would bring can’t be made through brokerages. Investments in church life, family and friends, physical fitness, beans, bullets etc…can’t be made through a brokerage account. There is no way to “…make sure that my family and I are in a position to live comfortably regardless of what happens.” If a neo fascist is elected and we enter WWIII then there is no such thing as ensured comfort. I too paid off my mortgage completely this week, but it will have been a mistake to have done so if SHTF. War creates refugees far from home and war turns lots of real estate, including possibly my home, into scorched earth and rubble.

Any comments on Bellatrix earnings call? I thought they did pretty well considering the expectations and actually managed to pay off the debt. I don’t understand the market reaction though. That analyst at Raymond James must be smoking something.

I haven’t been following BXE for some time so I can’t really say much. It looks interesting given the magnitude of the recent sell off but I still look at the AECO price at $1.30ish and that can’t be profitable for anyone. Given that you are following the story closely, would you say that debt service could become an issue with such low gas prices?