Week 279: Cautious on trade(s)

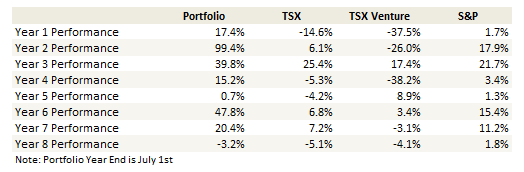

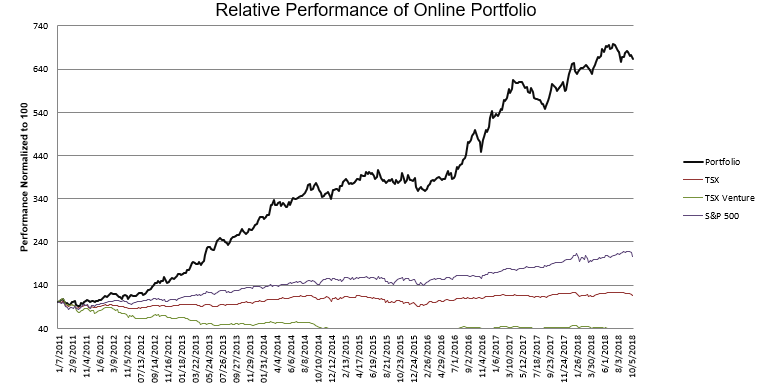

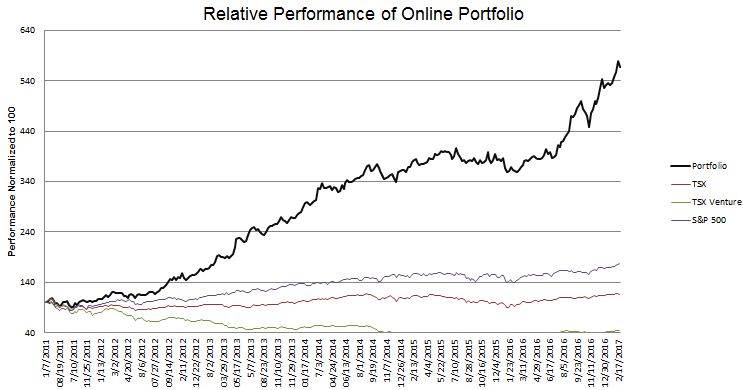

Portfolio Performance

Thoughts and Review

I haven’t written a post since my last portfolio update. Up until this last week I did not add a new stock to my portfolio. I have sold some stocks though. Quite a few stocks really.

I have been cautious all year and this has been painful to my portfolio. While the market has risen my portfolio has lagged. I have lagged even more in my actual portfolio, where I have had index shorts on to hedge my position and those have done miserably until the last couple of weeks. In fact these last couple of weeks are the first in some time where I actually did better than the market.

My concerns this year have been about two headwinds. Quantitative tightening and trade.

Maybe its being a Canadian that has made me particularly nervous about the consequences of Trump’s protectionism. With NAFTA resolved I don’t have to worry as much about the local consequences. But I still worry about how the broad protectionist agenda will evolve.

I continue to think that the trade war between the United States and China will not resolve itself without more pain. The US leadership does not strike me as one open to compromise. Consider the following observations:

Peter Navarro has written 3 books about China. One is called “Death by China”, another is called “Crouching Tiger: What China’s Militarism Means for the World” and the third is called “The Coming China Wars”.

In the Amazon description of Death by China it says: “China’s emboldened military is racing towards head-on confrontation with the U.S”. In the later book, Crouching Tiger, the description says “the book stresses the importance of maintaining US military strength and preparedness and strengthening alliances, while warning against a complacent optimism that relies on economic engagement, negotiations, and nuclear deterrence to ensure peace.”. The Coming China Wars, his earliest book (written in 2008), notes “China’s dramatic military expansion and the rising threat of a “hot war”.

Here’s another example. Mike Pence spoke about China relations last week at the Hudson Institute. Listening to the speech, it appeared to me to be much more about military advances and the military threat that China poses than about trade. The trade issues are discussed in the context of how they have led to China’s rise, with particular emphasis on their military expansion.

John Bolton’s comments on China are always among the most hawkish. Most recently he spoke about China on a radio talk show. Trade was part of what he said, but he focused as much if not more on the Chinese behavior in the South China Sea and how the time is now to stand up to them along those borders.

Honestly when I listen to the rhetoric I have to wonder: Are we sure this is actually about trade?

Is it any coincidence that what the US is asking for is somewhat vague? Reduce the trade deficit. Open up Chinese markets. Less forced technology transfer (ie. theft). Now currency devaluation is part of the discussion.

I hope that this is just a ramp up in rhetoric like what we saw with Canada and Mexico. That the US is trying to assert a negotiating position before going to the table and reaching some sort of benign arrangement. But I’m not convinced that’s all that is going on.

If this has more to do with pushing China to the brink, then that’s not going to be good for stocks.

I can’t see China backing down.

From what I’ve read China can’t possibly reduce the trade deficit by $200 billion as the US wants without creating a major disruption in their economy. Never mind the credibility they would lose in the face of their own population.

Meanwhile quantitative tightening continues, which is a whole other subject that gives me even more pause for concern, especially among the tiny little liquidity driven micro-caps that I like to invest in.

I hope this all ends well. But I just don’t like how this feels to me. I don’t want to own too many stocks right now. And I’m not just saying that because of last week. I have been positioned conservatively for months. It’s hurt my performance. But I don’t feel comfortable changing tact here.

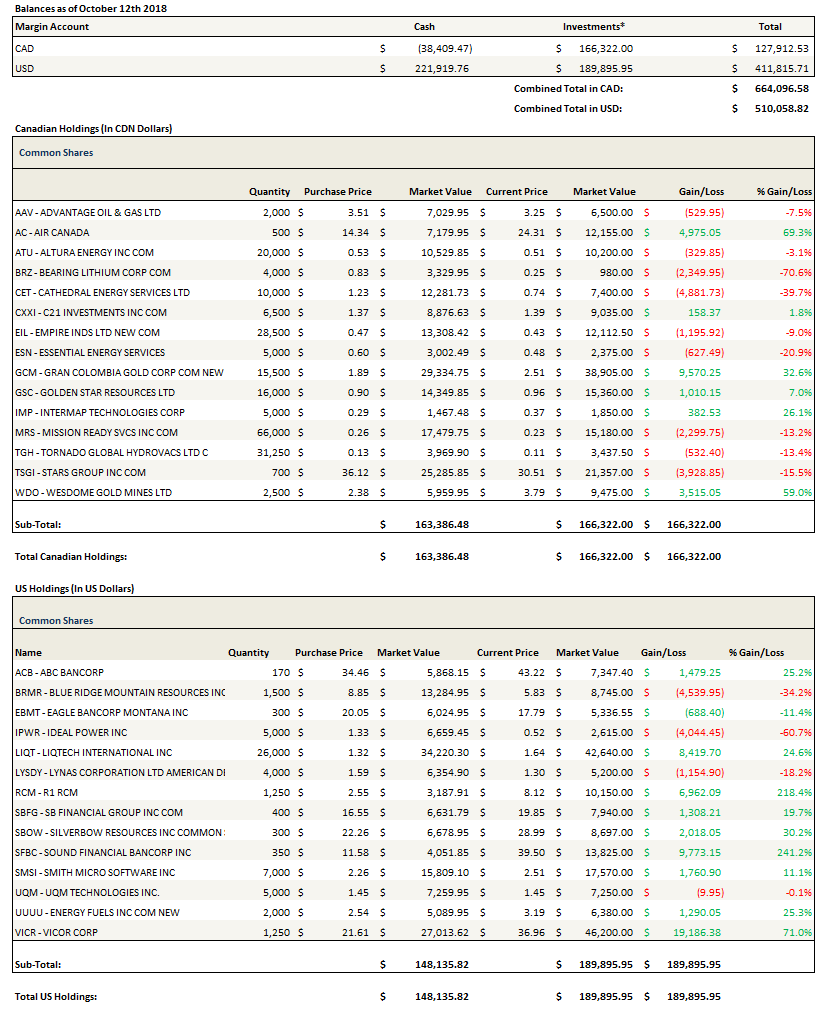

Here’s what I sold, a few comments on what I’ve held, and a mention of the two stocks I bought.

What I sold

I don’t know if I would have sold RumbleOn if I hadn’t been so concerned about the market. I still think that in the medium term the stock does well. But it was $10+, having already shown the propensity to dip dramatically and suddenly (it had fallen from $10 to $8 in September once already), and having noted that Carvana had already rolled over in early September, I decided to bail at least for the time being. Finally there was site inventory turnover, which if you watch daily appeared to have slowed since mid-September. Add all those things up and it just didn’t feel like something I wanted to hold through earnings.

I was late selling Precision Therapeutics because I was on vacation and didn’t actually read the 10-Q until mid-September. That cost me about 20% on the stock. I wrote a little about this in the comment section but here is what has happened in my opinion. On August 14th the company filed its 10-Q. In the 10-Q on page 14 it appears to me to say that note conversion of the Helomics debt will result in 23.7 million shares of Precision stock being issued. This is pretty different than the June 28th press release, where it said that the $7.6 million in Helomics promissory notes would be exchanged with $1 shares. Coincidentally (or not) the stock began to sell off since pretty much that day.

Now I don’t know if I’m just not reading the 10-Q right. Maybe I don’t understand the language. But this spooked me. It didn’t help that I emailed both IR and Carl Schwartz directly and never heard back. So I decided that A. I don’t know what is going here, B. the terms seemed to have changed and C. it’s not for the better. So I’m out.

I decided to sell R1 RCM after digging back into the financial model. I came to the conclusion that this is just not a stock I want to hold through a market downturn. You have to remember there is a lot of convertible stock because of the deal they made with Ascension. After you account for the conversion of the convertible debt and all the warrants outstanding there are about 250 million shares outstanding. At $9.30, where I sold it, that means the EV is about $2.33 billion. When I ran the numbers on their 2020 forecast, assuming $1.25 billion of revenue, 25% gross margins, $100 million SG&A, which is all pretty optimistic, I see EBITDA of $270 million. Their own forecast was $225 – $250 million of EBITDA. That means the stock trades at about 9x EV/EBITDA. That’s not super expensive, but its also not the cheapie it was when I liked the stock at $3 or $4. I have always had some reservations about whether they can actually realize the numbers they are projecting – after all this is a business where they first have to win the business from the hospitals (which they have been very successful at over the last year or so) but then they have to actually turn around the expenses and revenue management at the hospital well enough to be able to make money on it. They weren’t completely-successful at doing that in their prior incarnation. Anyways, I didn’t like the risk, especially in this market so I sold. Note that this is an example of me forgetting to sell a stock in my online tracking portfolio so it still shows that I am holding it in the position list below. I dumped it this week (unfortunately at a lower price!).

I already talked a bit about my struggle and then sale of Aehr Test Systems in the comment section. I didn’t want to be long the stock going into the fourth quarter report. Aehr is pretty transparent. They press release all their big deals. That they hadn’t announced much from July to September and that made it reasonably likely that the quarter would be bad. It was and the stock felll. Now it’s come back. It was actually kind of tempting under $2 but buying semi-equipment in this market makes me a bit nervous so I didn’t bite. Take a look at Ichor and how awful this stock has been. Aehr is a bit different because they are new technology that really isn’t entrenched enough to be in the cycle yet. Nevertheless if they don’t see some orders its not the kind of market that will give them the benefit of the doubt.

BlueLinx. I don’t have a lot to say here. I’m not really sure what I was thinking when I bought this stock in the first place. Owning a building product distributor when it looks like the housing market is rolling over was not one of my finer moments. I sold in late August, then decided to buy it in late September for “an oversold bounce”. Famous last words and I lost a few dollars more. I’m out again, this time for good.

When I bought Overstock back in July I knew I was going to A. keep the position very small and B. have it on a very short leash. I stuck with it when it broke $30 but when it got down to $28 I wasn’t going to hang around. Look, the thing here is that who really knows? Maybe its on the verge of something great? Maybe its a big hoax? Who knows? More than anything else what I liked when I bought it was that it was on the lower end of what was being priced in and the investment from GSR showed some confidence. But with nothing really tangible since then it’s hard to argue with crappy price action in a market that I thought was going to get crappier. So I took my loss and sold.

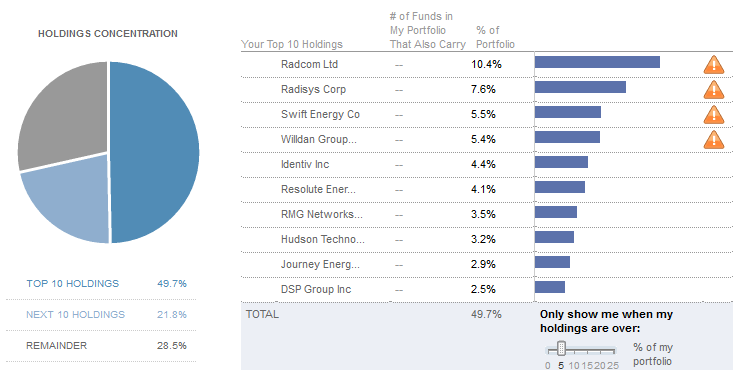

Thus ends my long and tumultuous relationship with Radcom. I had sold some Radcom in mid-August before my last update primarily because I didn’t like that the stock could never seem to move up and also because I was worried about the second quarter comments and what would happen to the AT&T contract in 2019. I kept the rest but I wish I would have sold it all. In retrospect the stocks behavior was the biggest warning sign. The fact that it couldn’t rise while all cloud/SAAS/networking stocks were having a great time of it was the canary in the coal mine. As soon as the company announced that they were seeing order deferral I sold the rest. I was really quite lucky that for some reason the stock actually went back up above $13 after the news (having fallen some $4-$5 the day before mind you), which let me get out with a somewhat smaller loss. The lesson here is that network equipment providers to telcos are crummy stocks to own.

Finally, I sold Smith Micro. This is a second example where I actually didn’t sell this in the online portfolio until Monday because I didn’t realize I had forgotten to sell it until I put together the portfolio update. But it’s gone now. I wrote a little about this one in the comment section as well. The thing that has nagged me is that the second quarter results weren’t really driven by the Safe & Found app. It was the other products that drove things. That worries me. Again if it wasn’t such a crappy market I’d be more inclined to hold this into earnings and see what they have to say. They could blow everyone away. The stock has actually held up pretty well, which might be saying that. Anyways I’ll wait till the quarter and if it looks super rosy I’ll consider getting back in even if it is at a higher price.

What I held

So I wrote this update Monday and Vicor was supposed to report Thursday. Vicor surprised me (and the market I think) by reporting last night. I’m not going to re-write this, so consider these comments in light of the earnings release.

One stock I want to talk about here is Vicor, which I actually added to in the last few weeks. Vicor has just been terrible since late August. The stock is down 40%. I had a lot of gains wiped out. Nevertheless this is one I’m holding onto.

I listened to the second quarter conference call a couple of more times. It was really quite bullish. In this note from Stifel they mention that Intel Xeon processor shipments were up significantly in the first 4 weeks of the third quarter compared to the second quarter. They also mention automotive, AI, cloud data centers and edge computing as secular trends that are babies being thrown out with the bath. These are the areas where Vicor is growing right now (Vicor described their core areas on the last call as being: “AI applications including cloud computing, autonomous driving, 5G mobility, and robots”).

Vicor just started shipping their MCM solutions for power on package applications with high ampere GPUs in the second quarter. They had record volume for some of their 48V to point of load products that go to 48V data center build outs and a broader acceptance by data center players to embrace a 48V data center. There’s an emerging area of AC-DC conversion from an AC source to a 48V bus. John Dillon, who is a bit of a guru on Vicor, wrote a SeekingAlpha piece on them today.

I know the stock isn’t particularly cheap on backward looking measures. But its not that expensive if the recent growth can be extrapolated. I’m on the mind it can. Vicor reports on Thursday. So I’ll know soon enough.

The second stock I added to was Liqtech. I’ve done a lot of work on the IMO 2020 regulation change and I think Liqtech is extremely well positioned for it. When the company announced that they had secured a framework agreement with another large scrubber manufacturers and the stock subsequently sold off to the $1.50s, I added to my position.

I’m confident that the new agreement they signed was with Wartsila. Apart from Wartsila being the largest scrubber manufacturer, what makes this agreement particularly bullish is that Wartsila makes its own centrifuges. Centrifuges are the competition to Liqtech’s silicon carbide filter. If Wartsila is willing to hitch their wagon to Liqtech, it tells me that CEO Sune Matheson is not just tooting his horn when he says that Liqtech has the superior product. I’ve already gone through the numbers of what the potential is for Liqtech in this post. The deal with Wartsila only makes it more likely that they hit or even exceed these expectations.

Last Thought

I took tiny positions in three stocks. One is a small electric motor and compressor manufacturer called UQM Technologies. The second is a shipping company called Grindrod (there is a SeekingAlpha article on them here). The third is Advantage Oil and Gas. All of these positions are extremely small (<1%). If I decide to stick with any of them I will write more details later.

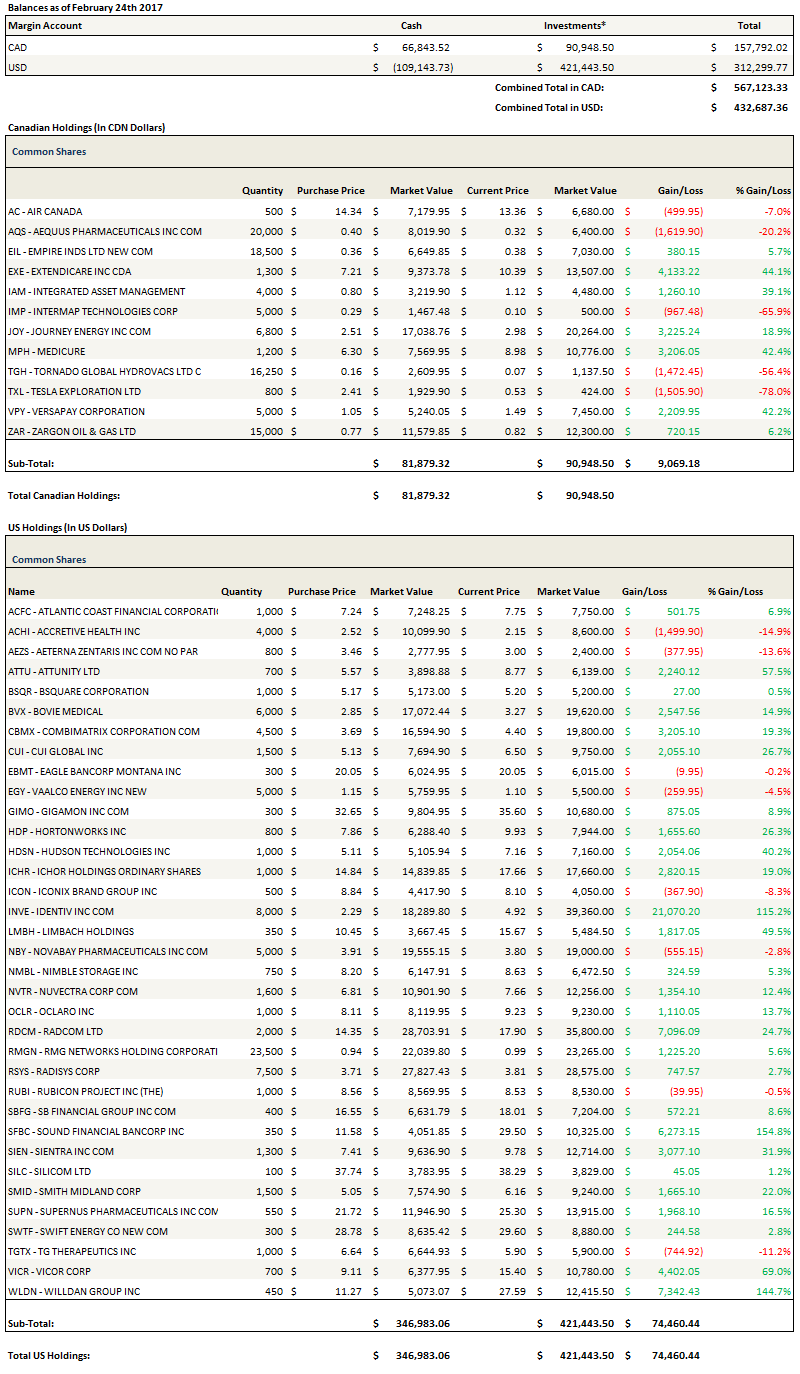

Portfolio Composition

Click here for the last seven weeks of trades.

{kind=link}

{kind=link}

{kind=link}