Radisys – Taking Advantage of Early Stage “Lumpiness” in the NFV Build-out

It’s been a while since I gave a single company write-up. For the last couple of years I’ve kept to monthly write-ups that are mostly short introductions to new positions and piecemeal updates of stocks I own. This write-up started out as a summary of an investment idea to a friend. It became an involved description of my second largest position, Radisys (it is second next to my biggest position Radcom, which is also a play on NFV uptake). So I decided to post it.

Radisys has been around for a long time providing networking solutions. They have a pretty mundane history of very little growth, mostly fluctuating between the $200 to $300 million of revenue mark for the last number of years.

The unexciting legacy business is a host of networking products (a segment they refer to as embedded products) such as blades, COTS racks, and COM boards. This segment has a declining revenue profile that is expected to deliver around $85 million this year and $75 million next year. It is expected to stabilize thereafter at around that range.

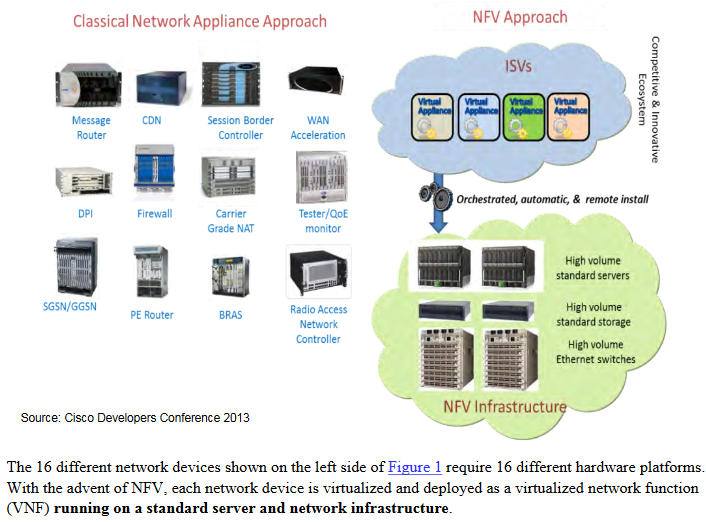

The legacy products aren’t the story. The story instead revolves around 3 new products that are designed to serve the next generation telecom build-out. Integral to this build-out, and to the differentiating features of the products, is a new way of designing and deploying telecom equipment, called network function virtualization (NFV).

The Network Function Virtualization Opportunity

NFV decouples hardware from software. Rather than purchasing proprietary hardware/software packages to fill specific tasks (and getting pigeon holed under a single vendors product umbrella), communication service providers (CSPs) can populate their central offices with off the shelf “white box” equipment. Software functions will be “virtualized”, installed and deployed off of the generic hardware as required.

I took the slide below from the EZchip white paper on the NPS 400 network processor (which happens to be the processor being used by Radisys in the hardware enabled version of the next-gen FlowEngine). It illustrates the range of proprietary telecom equipment that will eventually be replaced by virtualized functions.

The decoupling of hardware from software affords a number of benefits. First of all, upgrading is made easier, as swapping out software is a lot faster than swapping hardware. Second, adding capacity means acquiring additional licenses and installing additional software, not the physical installation of more appliances. Third, costs should come down, as the physical appliance is a cheap white box brand and it doesn’t have to be replaced with each upgrade.

There is no question NFV is gaining acceptance among Tier 1 CSPs. AT&T, which has led the charge this year, expects to have 30% of their network virtualized by the end of the year and to be 90% virtualized by 2020. A number of open source initiatives to standardize architecture have been started with names like CORD and ECOMP.

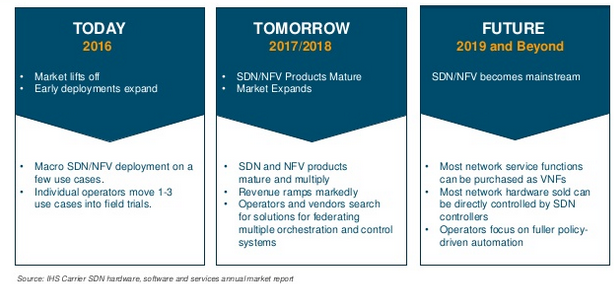

But we are still in the very early stages. IHS provided the following evolution roadmap over the next 5 years.

Its important to point out that NFV is not in the best interests of the incumbent telecom vendors. Part of the value of NFV is that it will lower capex and opex, and make the network more open, meaning that existing vendors will lose leverage in both volume and pricing. Mike Arnold just provided a great post parsing through the color provided by many vendors on their third quarter calls and how it illustrates the early stages of this trend.

Radisys offers three point solutions, DCEngine, FlowEngine, and MediaEngine that fill niches in the NFV world. They offer professional service specifically for the implementation of NFV solutions. And they are a member of the NFV initiative CORD (central office redefined as a datacenter), where they can influence NFV evolution and cultivate a position of technical leadership in the process.

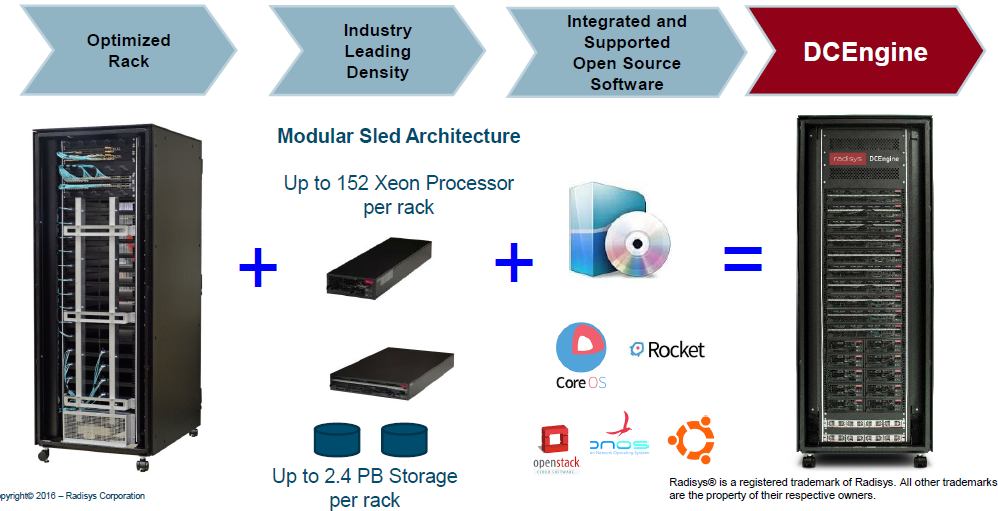

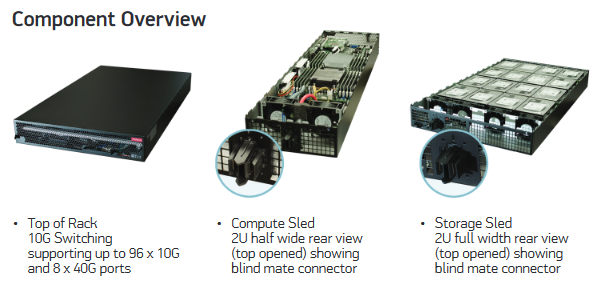

DCEngine

DCEngine has the most revenue potential of the 3 products. DCEngine is also the most straightforward of Radisys’s offerings to talk about. It’s basically a rack populated with white box hardware. This presentation, given at the July CORD summit, provided a nice illustration of what the rack is:

The hardware is mostly off the shelf. It includes switching, compute and storage sleds though some proprietary hardware may still be required for more complex use cases.

Radisys hopes to act as a system architect on many of its DCEngine implementations, meaning that they would be responsible for the procurement and implementation of the software (note that this expectation is very closely aligned with their CORD participation, which I will discuss below). Depending on the application, Radisys expects that software integration could be up to 25% of the DCEngine selling price.

Radisys hopes to act as a system architect on many of its DCEngine implementations, meaning that they would be responsible for the procurement and implementation of the software (note that this expectation is very closely aligned with their CORD participation, which I will discuss below). Depending on the application, Radisys expects that software integration could be up to 25% of the DCEngine selling price.

DCEngine is designed to perform high end workloads, give a high density footprint, and fill the new central office environment that will be performing more (virtualized) computing tasks at a faster pace. The opportunity is filling out these central offices with racks, and taking a 20% gross margin in the process.

DCEngine has a large total addressable market. Verizon was the first customer to order DCEngine from Radisys. They have placed 3 orders over the past 9 months. Those orders, which were described as being for “one application” and were for less than 200 racks, brought in $65 million of revenue this year so far. I have heard that each rack sells for around $300K.

The application that Verizon used DCEngine for was described as “a rounding error in the context of what they need to build out” by by CEO Brian Bronson. Radisys gave more color at the B Riley conference (I have a copy of the audio if anyone wants it), saying “AT&T for example has 4,500 central offices with 100 years worth of gear stocked on top of each other, working with them to build out telco version of a datacenter, 2x as dense as typical rack providers, 50% cheaper than competition on storage side of things”

As sales of DCEngine begin to pick up, and as it begins to be sold in conjunction with their professional services for more specific NFV use cases (again I will talk a little more about this below when I discuss the CORD initative), the product will start to pull through other products, in particular FlowEngine and MediaEngine, in some applications.

On the third quarter call Bronson said that DCEngine was already “beginning to provide opportunities to pull-in FlowEngine and MediaEngine”. You won’t see FlowEngine and MediaEngine slotted into every DCEngine rack, but in appropriate applications Radisys will have the authority to choose their own solutions.

FlowEngine

FlowEngine provides flow management, high performance switching, load balancing and routing. Radisys put up a pretty good video (embedded below) describing how FlowEngine is used in an NFV architecture to facilitate network flows of all the various types (video, audio, internet, streaming, etc) and distribute those flows to the proper virtualized network function (VNF). The VNF then processes the flows before returning the packets back to FlowEngine to be passed back down the proper network path.

FlowEngine is specifically designed to direct packets in an NFV environment. As this article describes:

Network traffic distribution today typically requires a complex integration of discrete load balancers, edge routers, and data center switches. As service providers virtualize more of their data plane applications, they find themselves having to choose between suboptimal fixed-packet processing rules, or incurring higher capex and opex costs to deploy load balancing products that can’t handle high data plane traffic volumes.

Providers need service-aware traffic management where SDN capabilities orchestrate data traffic and NFV resources process it. FlowEngine uses service function chaining under open SDN policy control to classify millions of data flows, then distribute the flows to thousands of virtualized network functions (VNFs) or physical network functions (PNFs). Specifically designed for the challenges of large NFV deployments

Radisys gave the following example of the price advantage of FlowEngine at the B.Riley conference back in May:

We are in the middle of bidding a deal in Asia with an operator and in this example it is for FlowEngine and the traditional competition incumbent is providing a product that clearly is capable, we think we have better technology, but let’s just say we are the same, it’s a seven hundred and fifty thousand dollar box and we are selling it for two fifty. We’re not short changing ourselves but the point is that telecom equipment manufacturers have been gouging the operators for decades, software and hardware acceleration have brought disruptive products to the point where we can deliver a solution that is as good or better at a fraction of the price.

Verizon was the initial customer for the product, as announced in June. Verizon used FlowEngine for “new services that have large and small traffic flows, including cloud-based applications, video optimization and IoT”.

On the third quarter conference call Radisys announced that a US Tier 1 had agreed to further FlowEngine orders that would commence in early 2017, and importantly that the orders were not through channel partners, meaning Radisys will have a more direct line of site and hopefully influence into the CSP implementation. I am assuming this Tier 1 is Verizon though its strange that they didn’t name them, since Verizon has been a named customer for FlowEngine in the past and I wasn’t aware they had done so via a channel. It’s possible that AT&T is the Tier 1 and that they have previously ordered product through a channel partner. If anyone knows the answer to this drop me a note.

Radisys also announced that they have a FlowEngine proof of concept (POC) underway with another Tier 1 service provider and expect to be able to announce other POC’s in the fourth quarter.

The company also announced that the next-gen FlowEngine appliance and virtualized software is in beta trials at service providers right now and will be ready for general availability mid-2017. This next gen version will be highly scalable, SDN enabled and will deliver twice the throughput of the existing FlowEngine product. As I alluded to at the beginning of the post, the hardware enabled version of the new FlowEngine will use Mellanox’s (formerly EZChip) NPS 400 processor, which is expected to deliver 3x the through-put at a third the price. The virtualized version will continue to run on 3rd party Intel x86 platform.

FlowEngine will do around $10 million of revenue this year and it pulls in about 60% gross margins. This is up from $5 million in 2015.

When talking about where they want to see FlowEngine in the next year, on the second quarter conference call Bronson said what he expect was:

It’s at least half a dozen if not 10 operators that we’re doing business with on the FlowEngine side of things in one way, shape or form. They may not be as big initially as Verizon but it’s our job to just get the door open with one particular application. The nice thing about FlowEngine is there is many, many use cases for FlowEngine.

At the B.Riley conference in May Bronson said that FlowEngine “has the opportunity over time to be a hundred million dollar business”.

MediaEngine

MediaEngine facilitiates the processing of new digital data stream protocols such as VoLTE, VoWIFI, and WebRTC (the coding of these streams into a protocol is called a codex). Importantly it also provides backwards compatibility between older codex’s and newer one’s so that all parts of the network can talk to one another. This process is called transcoding.

Past MediaEngine orders, which of note have been to Reliance Jio, which is an Indian carrier, and to a North American Tier 1 which I’m not sure but I think might be AT&T, and have been deployed to some degree in over 30 networks. These deployment have generally been to free up spectrum by providing processing for VoLTE. Mitel, for example, has been a key channel partner for MediaEngine, and they sell the product for VoLTE processing to facilitate their video and audio conferencing products.

Based on the language Radisys has used to describe the Reliance Jio wins, it appears that Reliance is using MediaEngine in a function beyond simple VoLTE, though I’m not entirely sure what the use case is (there is however a good SeekingAlpha article on this win here). Radisys has shipped over $20 million of MediaEngine product to Reliance.

As a VoLTE product MediaEngine has never been that exciting in terms of growth potential. The product did about $45 million of revenue in 2015 and is expected to do about the same in 2016. Most of the recent revenue has come from Reliance.

However that may be about to change. As I mentioned earlier, at the core of an NFV deployment is the desire to break up previously proprietary system hardware solutions into their constituent software components, in other words their network functions. One proprietary component is called a session border controller (SBC). The session border controller performs two functions, call control processing and transcoding. Depending on the type of networks that are talking to one another the capacity of these two functions does not always align. In particular, the call handling capacity can often exceed the transcoding capacity. The result is that the CSP has to purchase more SBC’s than their call capacity warrants to achieve the transcoding that they need.

MediaEngine essentially provides a cheap transcoding centric solution. In the NFV world, where MediaEngine is not tied to hardware, a CSP simply deploys the product as required at network boundaries as additional transcoding capacity is required.

This is a new use case for which Radisys has only recently announced a new MediaEngine version, called TRS. As far as I know they have yet to win business for this. But management alluded to the potential on the third quarter call, saying it “has a much bigger market opportunity than the current construct of MediaEngine”. In a bit of candor later in the call saying that in “transcoding what we’re trying to do is trying to beat the shit out of the SBC guys”.

Radisys put out a video that does a good job describing the disruptive nature of MediaEngine in the transcoding market.

Also on the third quarter call Radisys did announce a Tier 1, NFV based, win for conferencing services using MediaEngine. I believe that the carrier is AT&T, and the win is significant as it was a direct sale not through channel partners, which will allow Radisys to influence further business more easily.

CORD

Radisys is not an incumbent equipment provider to Tier 1 CSPs. So as the company tries to capitalize on the NFV opportunities, getting a foot in the door is an important first step.

CORD stands for Central Office redefined as a data center. Radisys gave the following description of CORD on its third quarter call:

The mission of CORD is to advance an open source service delivery platform that combines SDN, and NFV, and elastic cloud services to service providers. Or said differently, the mission is to facilitate the replacement of telco central offices and the big, proprietary, expensive equipment that gets installed in them with new solutions that leverage data center economics and cloud flexibility across the entire network.

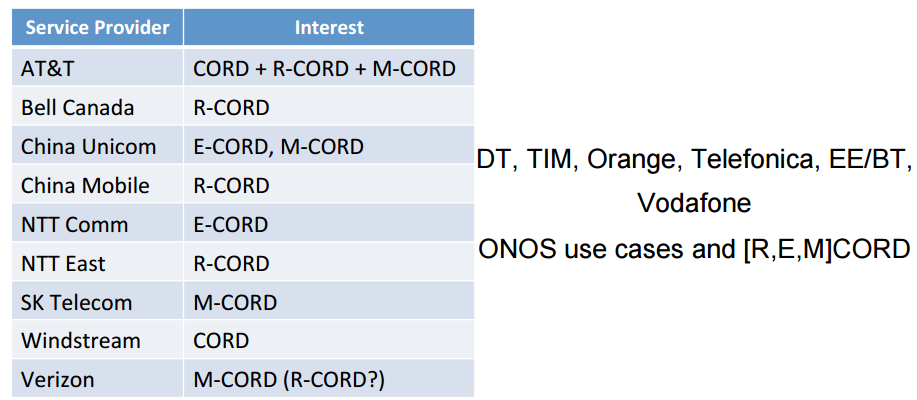

CORD actually consists of three distinct flavours, mobile (M-CORD), residential (R-CORD) and enterprise (E-CORD). Radisys is primarily involved with R-CORD and M-CORD though they do have some involvement in E-CORD, I’m just not sure what.

The involvement in CORD has the potential to drive a lot of customers to Radisys. Many of the Tier 1 telecom players are involved in CORD. This presentation, given at the CORD summit in July, gives an excellent overview of what the initiative is trying to accomplish. It also provides a list of the major CSP’s involved in the initiative:

For more detail on how the CORD initiative is redefining individual hardware components, see this presentation by AT&T.

In March, when Radisys announced that it was collaborating on CORD, they described their role as a “leading system integrator”. In particular Radisys would:

…help service providers and the community turn Residential, Enterprise and Mobile CORD proofs-of-concept into deployable carrier-grade solutions by offering end-to-end world class support for CORD integration and commercial deployment on Radisys’ DCEngine™ hyperscale data center product.

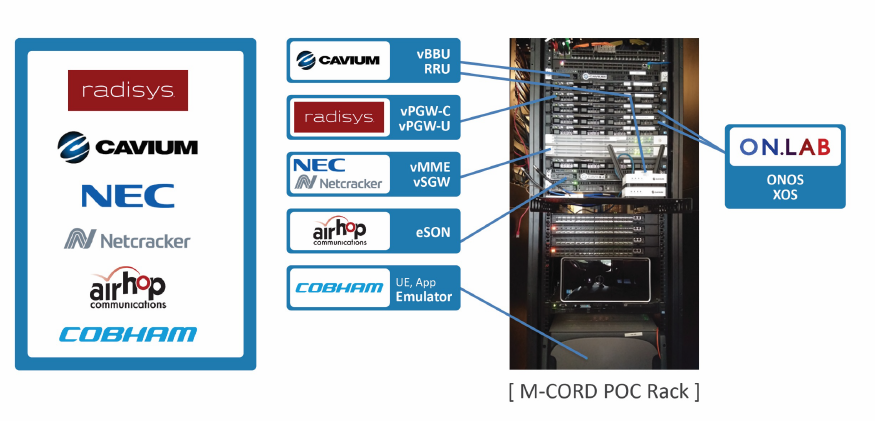

The CORD involvement also encompasses FlowEngine. FlowEngine has been offered “as a key data/forwarding plane component” into the mobile version of CORD, known as M-CORD. Below is a slide taken from this presentation that shows FlowEngine being used within the M-CORD proof of concept rack (vPGW-C and vPG-U describe dataplane component that FlowEngine will be providing).

With CORD Radisys can establish itself as an NFV expert, and cultivate expertise deploying NFV use cases and cultivate a closer relationship with CSPs. We began to see the first fruits of this in the third quarter, as they announced they had “entered into our first CORD integration proof-of-concept with a European Tier 1 service provider.” and that the “same thing is going on with other customers that we have in the funnel that I can’t talk to you guys about right now”.

To sum up the opportunity in CORD and how Radisys is using it to position themselve as the vendor of choice for NFV implementation, I will turn to one last short comment provided by Bronson on the last call:

…someone has to bring all this largely open and accessible software and hardware together to deliver a pre-integrated and tested solution. And while our competition is motivated to continue to push their own proprietary solutions, Radisys is embracing the infrastructure revolution and positioning to provide service provider with open source set of integrated solutions.

The Opportunity

Radisys has about 37 million shares outstanding. At the current share price the market capitalization is a little over $150 million. Their debt and cash flow about cancel each other out. Revenue this year is going to be around $215 million, which means they trade at less than 1x EV/Sales.

Analyst revenue estimates for next year are $229 million. But in my opinion this number is not worth a lot, as I will describe below.

NFV is in an early stage and, as such, is advancing in fits and starts. Apart from AT&T, which expects to have 35% their network virtualized by the end of 2016, other CSP’s are still in the lab running tests or at best looking at single use cases in the field.

The stock sold off heavily after earnings because of this lumpiness. It is leading to good quarters, precipitated by a big Tier-1 order, followed by lulls as new trials and proof of concepts are completed.

As such, while Radisys made it clear on the third quarter call that its in the middle of trials and proof of concepts, they are unable to provide definitive guidance for 2017. Orders from the next line of trials are still a few quarters off.

The size of these orders is also difficult to pin down. But the potential is for some of them to be very large.

Take for example DCEngine. Orders in the first 3 quarters of this year totaled $65 million. Remember that this was “one customer” (Verizon) “deploying one application” (likely storage) and this application is “a rounding error” compared to their overall network requirement. As I mentioned earlier, DCEngine is being tested by two other CSP’s, and the language Bronson used around these trials was ”when successful”. Next year, if these trials are successful, it does not seem unreasonable to expect at least similar deployment levels from these CSP’s as what Verizon has done, nor does it seem unreasonable to think Verizon will have more orders at a similar level to this year. If all that came together it would mean more than $150 million in revenue from DCEngine alone. That would blow out of the water any of the current analyst estimates of revenue in 2017. Radisys has also said they have a full funnel for DCEngine, and on the second quarter call said they expect at least 6 Tier 1 customers by the second half of 2016.

So the problem with estimating Radisys revenue for next year is that its more of a probabilistic exercise than is usually the case. We are too early to know just how big these products can get. Yet analysts are constrained by their job requirement to provide a quantitative estimate of the future. They have to come up with revenue numbers for 2017 when the reality is that even the company can’t come up with a reasonable revenue estimate right now.

When asked to give some revenue color on the third quarter call Bronson said he didn’t want to “put bounds on it”. I think the language was intentional, that the number could be absolutely huge if you get, for example, DCEngine orders from AT&T (who I am guessing is the North American Tier 1 in trial) Verizon and the Asian trial customer, maybe others, and additional orders from the new FlowEngine, or MediaEngine TRF orders from CSPs looking to virtualize more of their network.

Yet an analyst can’t create estimates based on conference call color, trials and “the funnel” of potential customers. They have to put out of firm model with numbers. And so Radisys growth looks rather mundane for the next year.

I think there is a reasonable chance its explosive. The company is in the right place at what is probably a bit too early time. This makes the business lumpy, but the stock an opportunity.

Nice post Lane!

How come Mike Arnold has no position in the stock? Tells me this is 10ft hurdle lottery type opportunity.

Do you know who the competitors are in the cloud space?

Mike doesn’t like to over-diversify. In general they are competing against the big incumbents, so think HP, Nokia, Cisco, etc, MediaEngine is going to compete against SBCs so there are also small players there like Sonus and Audiocodes, FlowEngine against the load balancers, Im not sure what the direct comparable would be against the next-gen FlowEngine, DCEngine I believe only has pod competition in CORD from Ciena

Thanks for your reply. Passes the sniff test, will dig deeper now.

So I read up on the Radisys and this does seems like a good opportunity. Virtualization of hardware systems is the logical next step and I like that these guys already got street cred delivering to big telcos ATT and Verizon.

I don’t like the exec compensation. $5million for a company that has a gross profit of $52m is excessive.

What are your thoughts on the sales cycle of these telcos? They are notoriously slow on boarding new vendors. I remember owning Ubiquiti Networks (UBNT) last year. They ran into the same issues after they got into enterprise sales.

Good find nevertheless. Thanks.