I wish I had finished this write-up a day early. I do not like writing up a stock that just went up 15%. But that’s where we are with RumbleOn. I’ve been working on the research and writing all week and then the stock goes parabolic today. I see no news to speak of. Anyways it is what it is, and like all my ideas I’m in this for the long term (insofar as the thesis holds up). Having said that, buying a stock up 15% the previous day is generally not a great idea.

I got the idea a month or so ago from a search of stocks at their 3-month high. When I’m bored and looking for ideas I will go to the 52-week highs or 3-month highs or some other simple price movement screen that gives a signal of strength and I’ll dig into some of the names.

I’ll look for a name that I haven’t heard of, usually keying on one that is small, and I’ll do a bit of work to see if its worth a closer look.

Anyways that’s how I found RumbleOn.

What was fortunate about the timing was that I had just been looking at Carvana. Carvana operates an online used car business that is similar to what RumbleOn does for motorbikes. When I looked at Carvana I couldn’t believe how expensive it was. When I looked at RumbleOn, I couldn’t believe how cheap it appeared in comparison.

Having dug into it further I’m still of that mind. In fact it seems to me that RumbleOn has a better business model than Carvana. I’ll give that comparison in a bit, but first let me describe what RumbleOn does.

An Online Motorcycle Marketplace

RumbleOn operates an online marketplace for buying and selling used motorcycles. They have a website (rumbleon.com) as well as an iOS and GooglePlay app.

The company makes cash offers for bikes to individuals looking to sell. If accepted, the bike is shipped to one of their regional partners (dealers), inspected and reconditioned and then put up for sale on the site.

Anyone can sell their bike to RumbleOn. Upload the vehicle info, fill out a form, add a few pictures and RumbleOn will make you a no-haggle offer. Its good for 3 days and you either take it or leave it.

It’s meant to be the opposite of going to a dealer or selling the bike yourself. There is no haggle, no pressure tactics, and you won’t deal with tire-kickers or nitpickers.

For a while RumbleOn also bought bikes through auction and had dealer inventory on their site. However they’ve stopped both as their retail acquisition channel has become self sufficient. They do buy bikes via some auto-dealers that take them on trade but don’t have a marketplace and just want to get rid of them.

Early on the goal was to insure that the site had adequate inventory. So the company reached for it from other channels. They are now focused entirely on generating inventory through consumers.

Buying a bike on RumbleOn is geared to be just as simple. Pick a bike from the available selection and put down a $250 deposit. The full price of the bike is paid in cash or financed through an unaffiliated bank or credit union partner shortly after.

Unlike most of the online used car dealers (like Carvana), RumbleOn is agnostic to who they sell the bikes to. Most of the car selling sites are focused on the consumer channel.

RumbleOn does that, but they also sell to dealer and auction channels. At the moment dealers are most of the business (via online and through auction). They made up 91% of sales in the first quarter while consumers made up just 9%.

The company expects to build out the consumer channel as awareness of the brand grows. This is a new business, a little over a year old. Marketing of the app and website should grow the percentage of sales coming from consumers. I expect all the channels will grow but that consumer sales will grow the fastest.

Margins on consumer sales are higher so they are the preferred customer. With a dealer sale RumbleOn has to share the margin.

In the first quarter dealer sales had an average selling price of $8,874 at a 7.8% margin while consumer sales had a $12,207 selling price and 13.7% margin.

Gaining Traction with Consumers

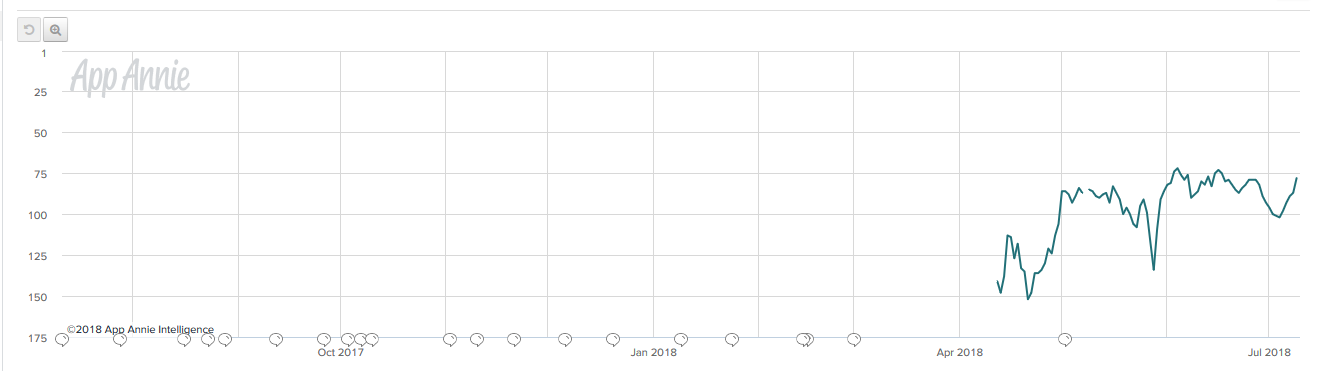

The website and app are only about a year old. Consumer momentum takes time. AppAnnie and Alexa show that both the website and the app are growing in popularity.

AppAnnie Ranking

Alexa Traffic Rank

Bringing retail owners and buyers to the site is all about experience. RumbleOn needs to make the experience, both for buying and selling a bike, as painless as possible.

Buying or selling a bike is not a lot of fun. The alternatives to RumbleOn are selling your bike yourself or selling to a dealer. If you sell yourself then you will inevitably “suffer the tirekickers and hagglers and deal with shaky payments”, in the words of one Harley rider commenting on a forum about the service. Selling to dealer likely means haggling, waiting onconsignment or a lower price than what RumbleOn can offer. Buying a bike offers the same problems in reverse.

What RumbleOn has to do is make the experience so effortless that its worth your while to give up a little margin.

It’s a trade-off to bike enthusiasts. Reading the reviews of RumbleOn and reading through forums where bike riders talk about buying and selling their bikes, its something that potential bike sellers are very aware off.

The most common complaint you hear about RumbleOn is that their offers are too low. But most bike owners also understand what they are getting in return for the margin they lose (which amounts to maybe $1,000). They get guaranteed cash and no hassle. They do not have to live for weeks or months with strangers coming over to their garage, trying to push a lower on price, and dissing their bike on minor issues. They also recognize that the offer price is usually better than what they’d get from a dealer.

Sales Growth

So far the model is working. Bike sales went from 355 in the fourth quarter of last year to 878 in the first quarter. The company said they expected that to double again in the second quarter.

I was a bit worried about how they could double sales when the website/app bike inventory seemed to be stagnating. At the end of the first quarter inventory was a little above 1,000 units, whereas now it is slightly below that number.

But it turns out this isn’t the case. Inventory has been rising. The appearance of stagnant inventory is because of the removal of dealer listings.

Adding Bikes

If you go back to the first quarter call management was asked about the disappearance of the dealer listings:

And then just as a follow up, it looks like you’ve taken the dealer listings off the site, is that a temporary thing or is that a permanent change?

Marshall Chesrown

Yes, I wondered if someone is going to say that. We have a plan – we’re getting ready to launch as we said some really, really interesting enhancements, I will be interested to get everybody’s feedback on them with regards to the website and we do see a huge opportunity to be a significant listener of vehicle both for consumers and dealers but we want to do it in a different format and I won’t get into all the details of it but I would tell you that before the quarter you will see what that plan is as it’s rolled out.

Excluding dealer listings, inventory has grown from ~125 in November of last year, to ~300 in March and now to a little over 1,000 today.

My take is that inventory procurement is the gating factor. The company has said that themselves. On the fourth quarter call CFO Steve Berrard had this to say:

This is really a buying product challenge. It’s not selling it. We proved we can sell it by the fact you know, when is the last time you heard a vehicle retailer have days-turns in the 20s, because the market is there to sell it. It’s buying of it, that’s the bigger challenge for us.

A key metric to watch will be how well they continue to acquire inventory. The ramp over the last 3 months as well as the confidence they showed by removing dealer listings are positive data points.

Acquiring inventory is all about making lots of offers and getting the owners to accept them. To expand inventories RumbleOn needs to:

- ramp offers

- improve acceptance rate

The ramp of offers is all about using technology to streamline the process:

We already which is very early in the cycle earlier than we anticipated we already do not have data people but data is being produced by our system and the data that we have we simply have a supervised whether it is released in those vouchers if you will, those cash offers. We have gone from being able to do about 20 an hour with the new technology enhancements, a single supervisor can do about an 100 an hour

Cash offers were 3,900 in the fourth quarter. That improved over 200% in the first quarter to 12,000. On the last call they said they were on pace to double cash offers in the second quarter.

Acceptance rates on those offers have been trending in the right direction as well. Acceptance rates were 12% in the fourth quarter rising to 14.9% in the fourth quarter. Chesrown thinks they can get this as high as 20% over time.

So all good signs. Even so I feel like obtaining the right inventory at the right price is going to remain the big challenge for the business.

Reviews

Case and point: if you look for negative reviews of the company, what you find will almost inevitably be a bike owner complaining that the offer RumbleOn made for their bike is too low.

The business is based on the premise that you are saving enough in terms of time, hassle and getting a guaranteed cash payment to make you willing to give up the $1,000 that you might get if you sold the bike yourself. And this is an equal or better price, all with less hassle, then you’d get if you went to your local dealer to sell.

You can find reviews of RumbleOn on BBB, Facebook, GooglePlay and on the Harley Davidson forums.

Other than the complaints about the offer prices the reviews are almost all positive. Customers get paid for their bikes on time, they receive their bikes quickly and they are consistent with what was ordered. The app is easy to use, it’s a simple process to get an offer on your bike and likewise it is easy to purchase a bike.

Guidance for the year

The company reiterated their full year guidance. They expect $100 million of revenue in 2018 and “in excess” of 10,000 units for the full year.

They changed the way they are getting to the $100 million from what they said on the previous call. Management had previously guided to $100 million but on 8,100 units sold. Their mix has changed. Rather than expecting sales would be dominated by Harley’s they now expect a better balance between Harley’s and non-Harleys. Harley’s are higher price, lower margin units.

This is a really new business and I don’t feel like management (led by CEO Marshall Chesrown and CFO Steve Berrard) know exactly how all the levers will play out. They’ve been surprised by the number of non-Harley’s, surprised by the number of dealers buying, and surprised by the strength and margins they are getting from the auction channel.

Nevertheless I’m pretty confident that Chesrown will navigate his way through this. The guy has a impressive background.

Management

Chesrown started off selling cars first in San Diego and then in Colorado, where he was managing 17 dealerships by the time he was 25. He started his own dealership chain soon after which was eventually bought out by AutoNation for $50 million. He has been called the “best used car salesman in the country”. There is a great biography of his early life in this article in the Inlander.

After making a fortune in the auto business Chesrown tried his hand in real estate development and lost it all in the crash of 2008. But not to be deterred he went back to his roots and founded Vroom in 2013.

Chesrown was COO and a director of Vroom until 2016, when he left to start RumbleOn. Though Vroom has hit on harder times this year, it was valued at over $600 million last year.

There are some similarities between the model used by Vroom and RumbleOn but there are also differences. I get the feeling Chesrown learned there and the learnings are now being applied. There have also been a number of executives that have left Vroom for RumbleOn.

Steven Berrard, the CFO, also has a pretty crazy history. He was the CEO of Blockbuster in the 90s, left there to work with (his friend?) Wayne Huizenga as COO of AutoNation, and from there took over Jamba Juice and eventually became CEO. He also led Swisher, which eventually ran into accounting problems but that was all after he left.

It’s a little nuts to me that these guys are leading an $80 million market cap company.

The management team and directors own a lot of shares. Together its about 75% of the Class A and Class B shares. Chesrown and Berrard own 36.5% between the two of them, and together the two own all the (1 million) Class A shares, which have 10:1 voting rights and effectively give them full control over the direction of the company.

Profitability

Buying and selling motorbikes online is new but buying and selling vehicles is not so much. In addition to publicly traded Carvana and Vroom, there have been Beepi, Shift, Fair, Auto1, Carspring and Hellocar and a bunch of others.

These companies haven’t all been successful. From what I can see Beepi, Carspring, and Hellocar all ran out of money. Shift and Fair seems to be doing ok, though Shift has had some bumps in the road by the looks of it. Auto1 is a German company that seems to be doing well.

I think the basic problem with theses businesses is what you see in Carvana’s financials. It takes a long time to get cash flow positive. Carvana has already been around for 5-6 years and yet when I look at the estimates it doesn’t look like they are expected to generate positive EBITDA until 2020.

So these companies need a source of funds to keep themselves going. When those funds dry up, like they did for Beepi, the business goes away.

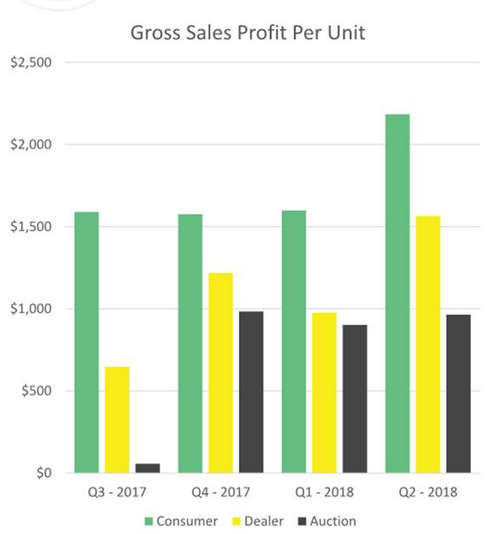

RumbleOn has similarities and differences here. This is low margin and always going to be. In the first quarter RumbleOn had gross sales profit, which is defined as the difference between the price RumbleOn bought the bike and the price they sold it at, was $1,132 per bike, or 12.3%. Gross profit, which includes costs associated with appraisal, inspection and reconditioning, was $788 per bike, or 8.6%.

The average margin on a Harley was 7.5% while for non-Harley Davidson’s it was 13.1%. Non-Harley’s seem to have a higher gross margin than Harleys, which has to do with their lower price point.

So it’s a low margin business and always will be. So RumbleOn needs to be tight on expenses and focused on volume.

That’s why I think the thing I like best about what I hear from Chesrown and the RumbleOn management team is their focus on getting to profitability and inventory turns.

They want to get RumbleOn to cash flow positive quickly.

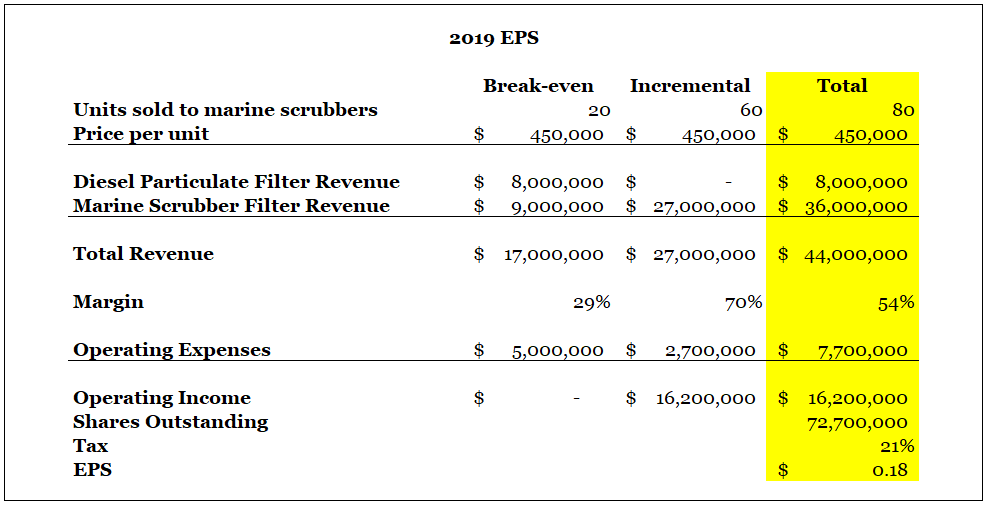

Breakeven

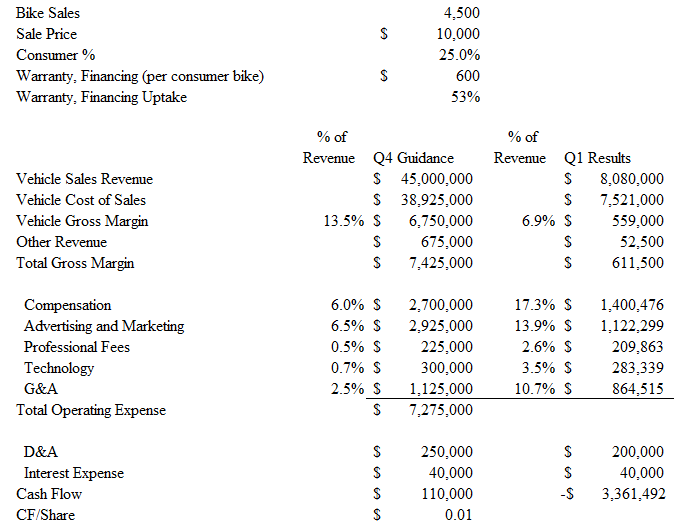

Berrard laid out where they would be in terms of costs by the fourth quarter. They also said the goal is to be cash flow positive by the fourth quarter. Guidance for the year is $100 million of revenue, 10,000 bikes sold.

To get to the unit sales guidance they need to sell 4,500 bikes by the fourth quarter, up from 878 in the first quarter. I’m assuming they hit their second quarter guidance of doubling bikes sold in the second quarter.

I took all the guidance information and made a few assumptions around consumer sales (expecting it to rise from 9% in Q1 to 25% in Q4) and their warranty financing (expecting uptake/dollar value to rise from 35% in Q1 to 53% in Q4), and I came up with a break-even model (thanks to @teamonfeugo for helping me work the kinks out of the model).

So I don’t know if this model with be accurate. The business is new, there’s some guessing on my part and I’m just going on what we know from the calls. But what is clear is that the growth is significant and if they can get there by Q4, then 2019 should be the year of cash generation.

It’s also worth noting that margins so far are primarily driver by the vehicle margin. Companies like Carvana are generating about half their margin from financing and warranty sales.

Comps

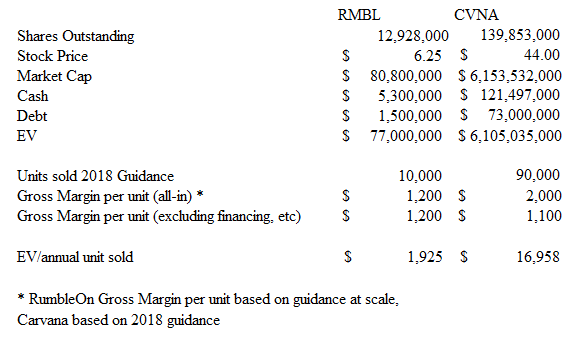

RumbleOn has 12.9 million shares outstanding. So at $6.25, which is roughly the average price I bought the stock at (I know its ran up the last couple days but I don’t want to redo all of this again), the market cap is about $80 million.

Compare that to Carvana, which has a market capitalization of over $6 billion. Carvana is of course much bigger. But on a per unit basis, RumbleOn looks very reasonable.

Carvana has higher gross margins per unit than RumbleOn but that is because of financing, service contracts and GAP waivers. As sales to consumers grow RumbleOn can expand these other offerings.

On just a pure selling price minus purchase price basis, once scaled RumbleOn has pretty comparable margins to Carvana. It also took them a lot less time to get there (Carvana vehicle unit margins were only about $600 as recently as last year).

It’s hard to look for comparisons from the other online car companies. Vroom, Shift and Fair.com are all private and I can’t find much information on valuation or how many cars they sell. The only somewhat interesting observation I can make is that in terms of unit inventory (this of course being cars for these three companies versus bikes for RumbleOn), they do not appear to be significantly larger. Vroom has about 2,500 cars on their site, Fair has a little over 7,000 and Shift only has about 800. RumbleOn was a little over 1,000 at last glance.

Multiples

Here’s a table of what RumbleOn’s market capitalization looks like at different revenue multiples and $100 million of sales. The 3.4 multiple is based on Carvana’s forward 2018 revenue multiple.

I realize the numbers are high, but it is what it is. I’m using the company’s guidance and Carvana’s multiple. Consider that RumbleOn is growing faster than Carvana at this point.

What sort of multiple does RumbleOn deserve? I’m sure you can make an argument that because the margins are low, the multiple should be low. That’s one perspective. But they are also growing like a weed. And then there is Carvana. If Carvana gets almost a 4x multiple, I don’t see why RumbleOn shouldn’t get at least something above 1, probably more. That multiple should grow as they become more established.

I realize that the used car market is way bigger and so maybe there is a premium for that. But used bike sales aren’t exactly small themselves, especially compared to RumbleOn’s size. According to their S-1 there were 800,000 motorbikes sold in 2016 and 50% of those are done on a peer to peer basis. Then there is the eventual expansion into other sports vehicles. RumbleOn also doesn’t have the 5-10 online and gazillion bricks and mortar competitors fighting with them for share.

What to look for

First, I want to see the website inventory continue to expand. Offers should continue to grow and acceptance will hopefully increase. At the same time their days sales are equally important. That number was 42 in the first quarter versus 38 in the fourth quarter. Carvana days to sale were 70 in the first quarter, down from 93 year over year. RumbleOn has focused on turns and needs to continue to do so.

Second, I want to see consumers comprise a greater percentage of sales, and (ideally) I want dealer sales to take place more and more through the website. But most of all I just want to see sales grow.

Third, I don’t want to see their costs blow up. Costs are going to increase as the business scales but they should also come down to their targets in terms of percentage of revenue.

Fourth, at some point I expect they will expand into other sport vehicles. They’ve mentioned expansion into ATV’s, UTVs, snow machines and watercrafts as other targeted areas.

Conclusion

Online used vehicle selling is a tough space to be in. Carvana has a great chart this year but there was a lot of skepticism (and a high short interest) when it went public.

A lot of other players have ran out of cash. Beepi, Carspring, Hellocar and now Vroom have all struggled.

But all these guys are all selling cars. I think RumbleOn has some advantages selling bikes.

- They are much easier to transport.

- They are a niche market compared to used car sales and thus more difficult to sell yourself via Craigslist or Kijiji.

- They don’t have the same level of competition online. And their traditional dealer competition is arguably less savvy than the used car dealer incumbents (remember that a lot of used car dealers take bikes on trade but don’t want to sell them, so they are actually a source of inventory to RumbleOn).

They are also offering a quick cash, no haggle, simple model for buying and selling bikes in a business that has traditionally relied on squeezing extra margin by making the process as difficult and opaque as possible.

The other advantage here is that RumbleOn is 100% online. On the last call they talked about how they can scale without adding to headcount outside of marketing and technology. They basically operate out of a single building. They aren’t even touching the inventory themselves.

The other advantage RumbleOn has over most (not all) of the online car players is that they’ve involved the dealers. Like I said earlier they are agnostic on the distribution channel. They will sell to consumer, dealer and auction.

This allows them to ramp sales (albeit it at a lower margin) much faster than if they had to rely exclusively on consumer marketing of the app and website.

Finally, I think these guys have the right idea by focusing on inventory turns. They don’t care who they are selling to, and they aren’t trying to squeeze every last bit of margin out of the sale. They just want to get that inventory in and ship it out as quickly as possible.

When they get into power boats, snow machines and ATV’s I think most of these advantages are amplified.

If I’m thinking about this right, growth is gated by how quickly they can acquire inventory. Given the rate at which cash offers and acceptance are increasing, I think that is well under control.

So it looks pretty interesting. Nevertheless its a tough business because gross margins are guaranteed to be low. Its all about driving volume, keeping costs down and where possible upselling through warranties and financing.

So far they doing all of this quite well.

As you know I usually take a small position (usually 2% or a little higher) in a stock and then if it works I start adding as it rises. With RumbleOn, I’m excited enough about the idea to make that higher right from the start. I think if this works it will have some legs. So we’ll see.