Swift Energy as a Post-Bankruptcy Recovery Story

Heading into the OPEC meetings I owned small positions in a number of oil and gas stocks. After the agreement was reached I significantly ramped up those positions. As I wrote on the weekend, in the days following the OPEC meeting I added back Granite Oil (GXO) and added to Resolute Energy, Journey Energy, and Zargon Oil and Gas. But my biggest add was to Swift Energy.

I have talked about Swift before here. I took a position in the spring as the company was coming out of bankruptcy. They had agreed to a pre-packaged bankruptcy deal that would give existing shareholders 4% of the new company. In addition to the equity, existing shareholders received warrants.

It was the warrants that caught my attention. For every share that you received you also received 7.5 warrants. The warrants were way out of the money ($80 and $86), but they also had a long dated expiry (2019 and 2020). It seemed like a good leveraged bet on something going right.

Since that time the company has emerged from bankruptcy and the stock has traded up from around $20 to $33. So that’s pretty good, but remember the distressed levels that many oil and gas companies were trading at in February-March. Swift has really market performed at best.

I think that’s because the stock has been stuck on the grey markets, and only recently began to trade on the OTC market. On a third rate exchange and without liquidity, Swift has seen little interest from investors.

Peer Comparison

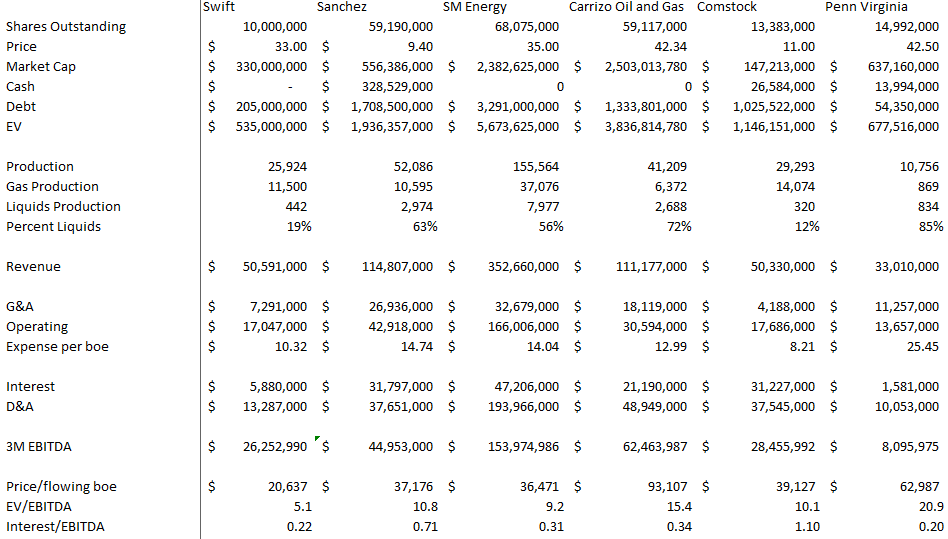

Below is a comparison I made between Swift and a few other comparable oil companies. I picked companies that operate in the Eagle Ford and where I could that have a natural gas weighting. Its difficult to find ideal peers to Swift because most Eagle Ford operators are oily. Swift is gassy because they found a sweet spot in the gas window in Fasken and have been exploiting it. But as I will describe, its not wholly accurate to describe Swift as a pure play on gas and they have more in common with their oil peers then their oil weighting suggests. I know this comparison isn’t perfect: I just took the data directly from the last 10-Q, so it doesn’t account for recent transactions from SM Energy or Sanchez Energy, and all of these companies are bigger than Swift; its difficult to find public oil and gas companies in the Eagle Ford that have an enterprise value on par with them. I’m open to suggestions.

Perhaps the closest comparison is Comstock Resources. Comstock is gas weighted, has Eagle Ford land in the same counties as Swift (McMullen and LaSalle counties) but also has a lot of gassy acreage in the Haynesville. Comstock trades at twice the valuation of Swift, based on both flowing boe or EBITDA.

I made a comparison based on EBITDA because it was simple, but if anything it understates Swift’s value because coming out of bankruptcy the company has a relatively low debt level. Swift pays far less in interest than most peers, so more EBITDA drops to cash flow.

Thinking of Swift as a pure gas player is misleading. The history of the company shows that it has typically had an equal oil/gas weighting. It has only been in the last couple of years that gas production has dominated.

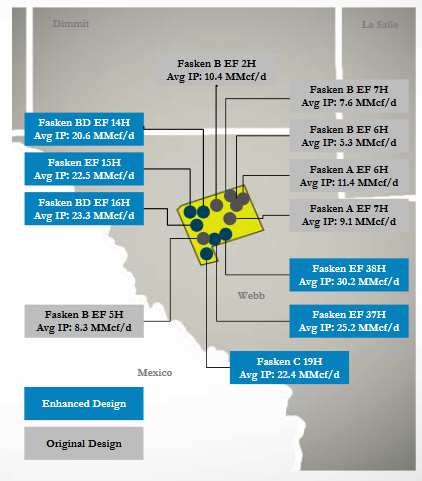

Fasken Gas Acreage

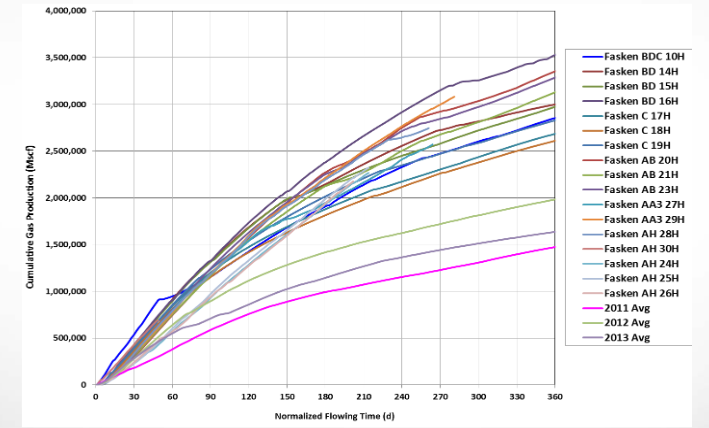

This shift to gas is because of the Fasken acreage. In 2014 the company made changes to their completion techniques at Fasken and achieved a dramatic improvement in their results. Below are well results before and after.

Swift has focused its drilling on Fasken since it went into bankruptcy in early January. In early 2015 the gas weighting was around 60%. In the third quarter it had risen to 81%.

While being gassy is often inferior to having a more oily weighting, the Fasken wells generate strong returns. Most of the new wells are have produced over 2.5Bcf (over 400,000boe) in the first year:

At $3 gas the company says that Fasken wells generate over 100% IRR at $3 gas.

Other more Oil Weighted Properties

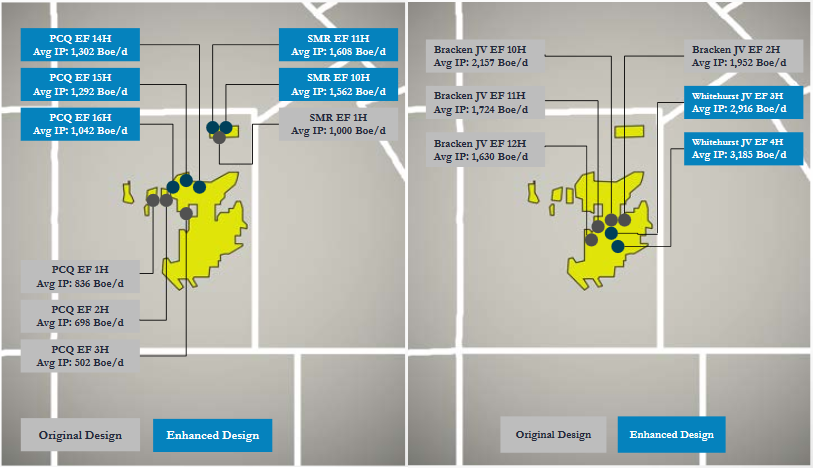

While the company has focused on Fasken and become a gas-weighted producer as a result, their remaining acreage is more balanced. In particular in McMullen County (their AWP acreage) they have over 200 locations in their oil and condensate windows:

In fact, apart from their newly acquired and untested acreage in Oro Grande and Uno Mas, Swift has far more oil acreage than gas.

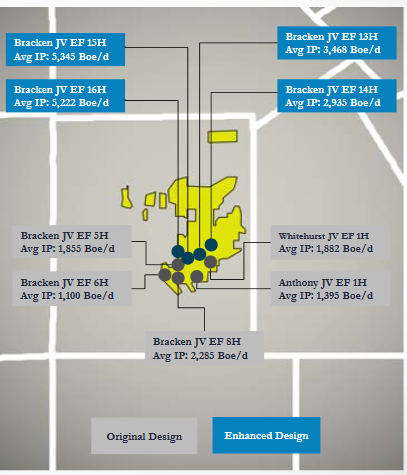

Much as they “cracked the code” in Fasken and achieved a step change in results, Swift appears to have had a similar breakthrough in AWP.

The PCQ wells are typically 90% oil while the Northern Bracken/Whitehurst wells are around 50% condensate. In the south Bracken where it is gassy, Swift has had success not far different from Fasken, with Bracken wells IP30s exceeding 5,000boepd and cumulative production that looks like it will exceed 2BCF in the first year. Below are IP30’s from this area:

Capital Expenditures

Swift has curtailed their drilling and completion activity since entering into bankruptcy. In the third quarter 10-Q, they described their 2016 operating activities at Fasken:

At our Fasken field in the Eagle Ford play, eight wells were placed into the system during the first nine months of 2016. Seven wells were placed into the system at rates between 15 – 20 MMcf per day of natural gas and one well had mechanical issues and was placed into the system at a restricted rate of 9 MMcf per day of natural gas. The Company resumed drilling operations at Fasken in October 2016 and expects to drill four wells by the end of the year. These four wells are expected to come online in early 2017.

And in the second quarter 10-Q they described their AWP activities:

The expenditures were primarily devoted to completion activity in our South Texas core region as we completed four wells in our AWP Eagle Ford field and also initiated completion work for four wells in our Fasken field.

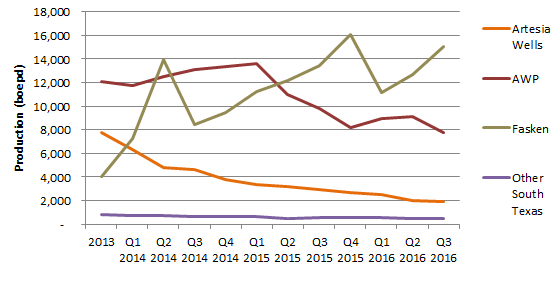

Prior to October, the company had not drilled any wells in 2016. They completed 4 AWP wells in the first quarter, and completed 8 Fasken wells in the second and third quarter. The impact of these activities can be seen in an area breakout of production results:

Artesia has seen no drilling activity for the last couple of years and the wells in the area have been declining naturally. In 2015 the company drilled and completed only one well at AWP and so the decline there is close to natural. The flattening of production in the first and second quarter at AWP coincides with the 4 well completions during that time. Fasken saw the majority of activity in 2015, followed by a lull in the first quarter of 2016 and a corresponding drop in production that recovered once the 8 new wells were completed in the second and third quarters.

A few implications can be drawn. First, two wells per quarter at AWP seem sufficient to maintain production levels there. Second, 4 wells per quarter at Fasken increased production by 2,000boepd. Third, production declines at Artesia are moderating and should be fairly insignificant to overall corporate production going forward.

The company has spent $60 million on capital expenditures this year. In the 10-K the company said they would spend $12 million on corporate and regulatory costs. That leaves $48 million that has been spent completing 12 wells and starting drilling on maybe one or two of the 4 wells being drilled at Fasken before year end. Given that completion costs at Fasken are around $3.5 million, tie-in is another $0.2-$0.3 million and that costs are AWP are slightly higher, the numbers line up.

Production Going Forward

At current production rates, $3/mcf gas and $50 oil Swift should be able to generate EBITDA of $130 million and be able to cash flow around $115 million. That would be enough cash to drill and complete 4 AWP wells and another 11-12 Fasken wells. That level of drilling should be enough to grow production, with my guess being by about 10%.

This compares favorably to a number of other E&Ps that I have looked at where I have difficulty seeing how they can maintain production levels at $50 oil while remaining within cash flow. In many of these cases its simply the debt burden and interest payments that bog them down.

Nothing is Perfect

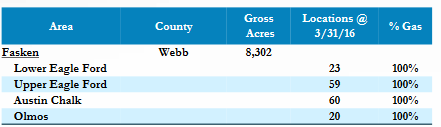

Swift is not without risk. One risk with Swift is that their remaining drilling inventory at Fasken is modest. Swift only has about 8,300 acres at Fasken, and in the lower Eagleford, where they have focused their drilling, they only have about 20 locations left. It remains to be seen whether the upper Eagleford, Almos or Austin Chalk can produce as prolifically.

I’m also not sure about the upper management. After emerging from bankruptcy a new Chairman of the Board was appointed, Marcus Rowland. Rowland was an original member of the Chesapeake team being with the company from the early 90’s until 2011. I’m sure he had a lot of successes at Chesapeake but he has also been known for steep executive compensation.

A month before Rowland was appointed, a number of Swift’s original executive team left the company, including Terry Swift. I have mixed feelings about that. I know that many think these guys were incompetent. They totally mishandled the balance sheet and then blew it by not hedging anything heading into the 2014 downturn. But they also were very good operators. They unlocked Fasken, and showed continual improvement in drilling efficiencies and performance. I hope that the engineering teams remain intact.

At any rate there is a void that needs to be filled. They appointed the COO as the new CEO on an interim basis. But we will have to wait for the longer term plan.

Swift also some lower priced hedges. They have about 20-25% of their gas production in 2016 hedged at around $2.80 per mcf and another 25% collared between $3-$3.90 per mcf. They have about 20% of their 2017 oil production hedged at $48 per barrel.

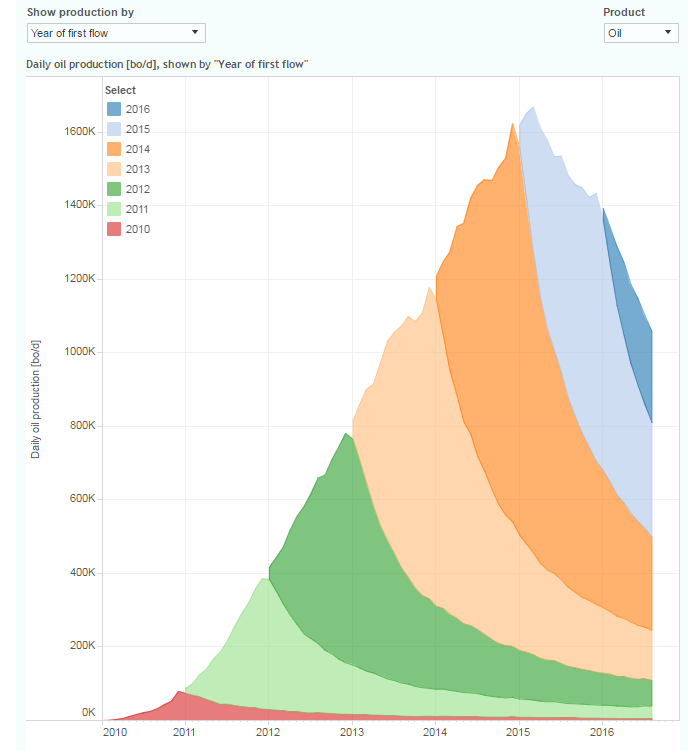

Finally, the Eagleford is not the premier basin that it was a few years ago. That spot has been taken by the Permian. As pointed out in this tweet, $50 oil is not bringing back rigs.

#Eagle_Ford is struggling to add rigs @ current prices. Additional $5-$10 is needed to have a clear reversal #OOTT pic.twitter.com/yi6vKKmXrw

— Anas Alhajji, Ph.D. (@anasalhajji) December 8, 2016

//platform.twitter.com/widgets.js

This post, from a blog that provides good information about shale production, illustrates the declining trend the Eagleford has experienced:

Have you looked at Key Energy to see if interesting post-BK?

I haven’t but I just did and it looks pretty interesting. I wish I would have seen it a day earlier!

I just want to thank you again for the comment – KEGXQ/KEG has turned out to be a great idea. If you have any others please let me know!

Lsigurd, you might find Lilis Energy interesting. Prime location in the Permian and virtually unknown.

Thanks, I have looked at Lilis, it was a while ago though, I subscribe to Schaeffers letter (that is where I got REN from too) but when I ran the numbers on Lilis it seemed similarly priced to REN and yet they didnt have much in the way of drilling results on their acres yet. So I stuck with REN. But I haven’t looked since. Has the story moved forward?