Revisiting Zargon after the debenture amendment

I wrote about my position in Zargon in my September update. I bought the stock because, after a large asset sale of their Saskatchewan properties at a favorable price, the company seemed poised to recover with an uptick in the price of oil.

As an aside, what a long post that update was! I really was cramming a lot of information into the monthly updates I used to focus on. Hopefully having the updates dispersed into smaller chunks will make for easier reading.

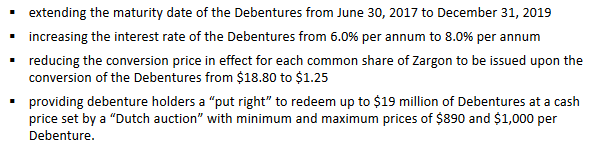

On Friday Zargon announced that their 6.00% convertible unsecured subordinated debentures due June 30, 2017 would be amended, pending approval of holders. The amendments are as follows:

When I looked at Zargon in the fall I did so with the assumption that they would have to dilute to raise capital to pay back the debentures. I was optimistically thinking that would happen at around a 80c share price.

With this deal Zargon is using the cash it has available to pay what of the debenture it can, and then, rather than issuing equity at the current level, its saying give us 3 years and we will issue equity at a 50% premium.

So its much less dilutive than I had been anticipating.

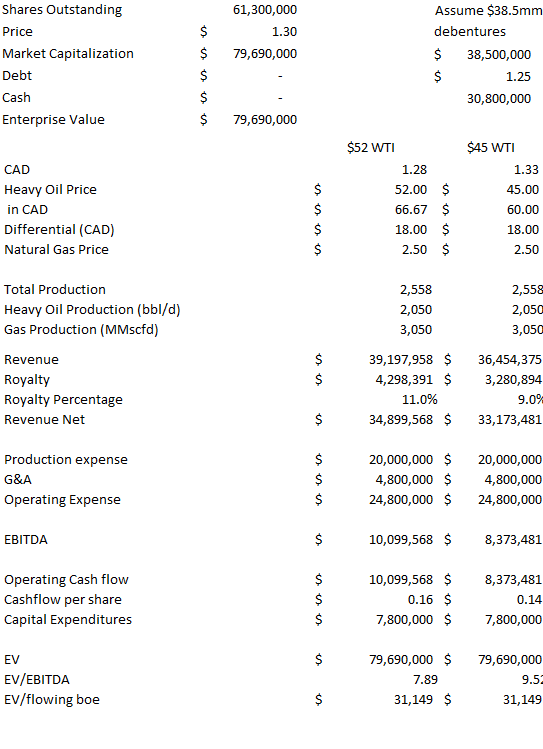

I took a look at what Zargon would look like if the debentures are converted. This happens at a stock price of $1.25, so I took a look at the company at $1.30. That implies over 50% appreciation from the current level. What I’m doing here is asking the question “is this is a reasonable valuation for this company?” – if it is, then there is a lot of upside in the stock.

If I assume that Zargon uses the $19 million to purchase the debentures at par (as opposed to 89% of par), which would be the worst case outcome of the put option, they end up diluting 31 million shares with the rest of the debentures (at $1.30 the debentures would be in the money). The capitalization and metrics look something like this:

(Note that my $52 scenario assumes a 1.28 CAD/USD exchange whereas my $45 scenario assumes 1.33 exchange. I am trying to be conservative by using an $18 differential between WTI and what Zargon realized. This differential was $10/bbl in the third quarter)

(Note that my $52 scenario assumes a 1.28 CAD/USD exchange whereas my $45 scenario assumes 1.33 exchange. I am trying to be conservative by using an $18 differential between WTI and what Zargon realized. This differential was $10/bbl in the third quarter)

Total market capitalization is still only $80 million. There is no debt. And you have a company with a best in class decline rate of ~10%, producing 2,500boepd that is 75% oil.

On traditional metrics it looks reasonable. Even after the large price appreciation the company would still be trading at $31,000 per flowing boe and at a little under 8x EV/EBITDA, which is in-line with peers once you account for the fact that the resulting company has no debt. At $52 oil ($66 Canadian), they can keep production steady with capital expenditures of $6.3 million (in the recent corporate presentation they breakdown the $7.8 million of capital expenditures they expect to incur in 2017 and $1.5 million of it is for land retention). This leaves around $4 million of discretionary cash flow for growth.

I think Zargon could turn out to be a good idea in a rising oil price environment. It wasn’t, and isn’t a great company at $40 oil. Its barely treading water. At $50 it gets its head above. In the high $50’s there is real value there. I thought we were moving into a rising price environment in September and I am more convinced of that now. So I think there is more chance Zargon moves higher than lower.

don’t forget about the tax assets. history of M&A in the Canadian oil patch suggests these have at least ~C$20M of value if Zargon is sold in its entirety or just continues as a going concern (and possibly less value if assets are sold piecemeal)

Lane,

There is a recent bear commentary about RSYS in this article.

http://seekingalpha.com/article/3819526-catching-wave-cloud-networking-next-big-wall-street-buzzword

Wondering how you look at the amended credit agreement? Also I noticed you increased your stake in RDCM. I remember reading your post about how RDCM has limited TAM than RSYS. What made you change your mind?

Thanks.

I never know what to think about comments like these – whether they are sincere or not. I mean if you model out the Q3 CC revenue color that Bronson gave for the first couple quarters of 2017 (low-$40s) , their expense increases ($15mm quarterly run rate in Q4 followed by an extra $3mm annualized in Q1), and 38-40% non-GAAP GMs (which may even be optimistic) its pretty easy to see their adjusted EBITDA hitting just above the covenant range in Q2-Q3. So the amendments didn’t seem like a big surprise to me.

I guess what I wonder is if the commenters really didn’t know that? The one guy is short so you would think he’s basing that decision on information like the guidance (in fact that is probably THE reason to have been short RSYS over the last few months), the other is reading through SEC filings so he’s clearly looking into the details, yet they commented like they hadn’t modeled out the company guidance and q3 commentary. It seems odd doesn’t it?

I’ve been assuming the reason the stock has done nothing for the last 2+ months is because everyone has been pricing in this guidance and those not comfortable with it have been getting out.

But maybe I am missing something. Wouldn’t be the first time.

My expectation is that RSYS is going to move based on the color around the trials. So if RSYS comes out with Q4, announces Q1 guidance that is inline with above but says we have 1-2 more trials on DCEngine, another on FlowEngine and maybe another win with one of those or MediaEngine (which they seemed to be saying at the Needham conference), I don’t think the guidance is going to matter that much. But if the trials are stalling and there is nothing new to report,then the stock is going to do poorly.

I reduced RDCM back down since. There has been a couple of times where I have tried to time the swing on RDCM between the high-17s and 20. It seems stuck in this range and probably will continue to be until there is some announcement.

Thanks for your feedback. I agree the SA comments don’t seem deeply researched. You and Mike have done a great job bringing the company to the public’s attention.