Week 286: On being wrong a lot

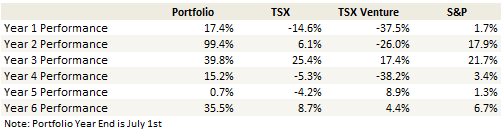

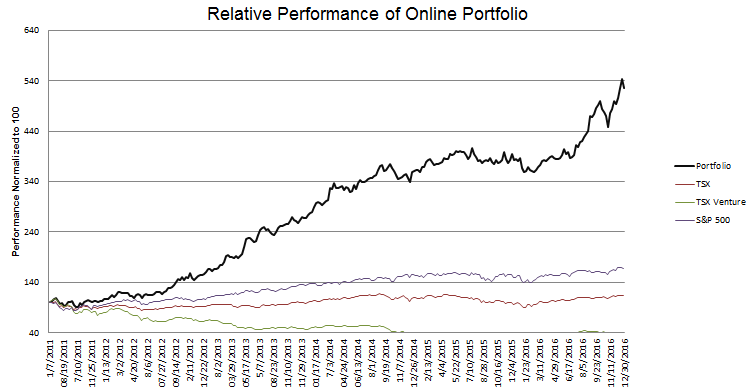

Portfolio Performance

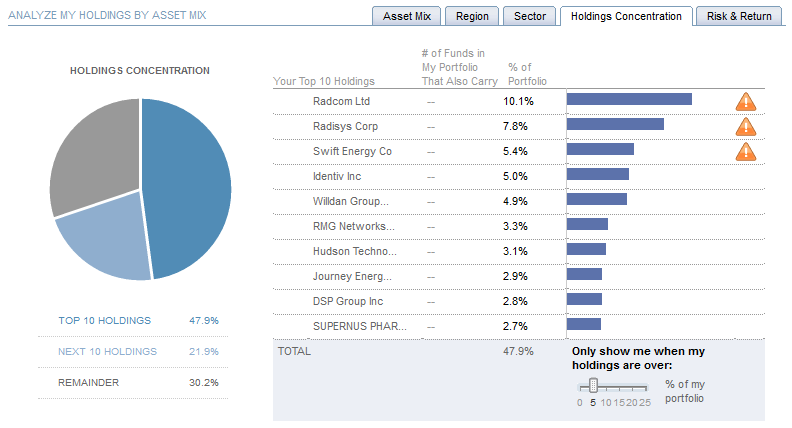

Top 10 Holdings

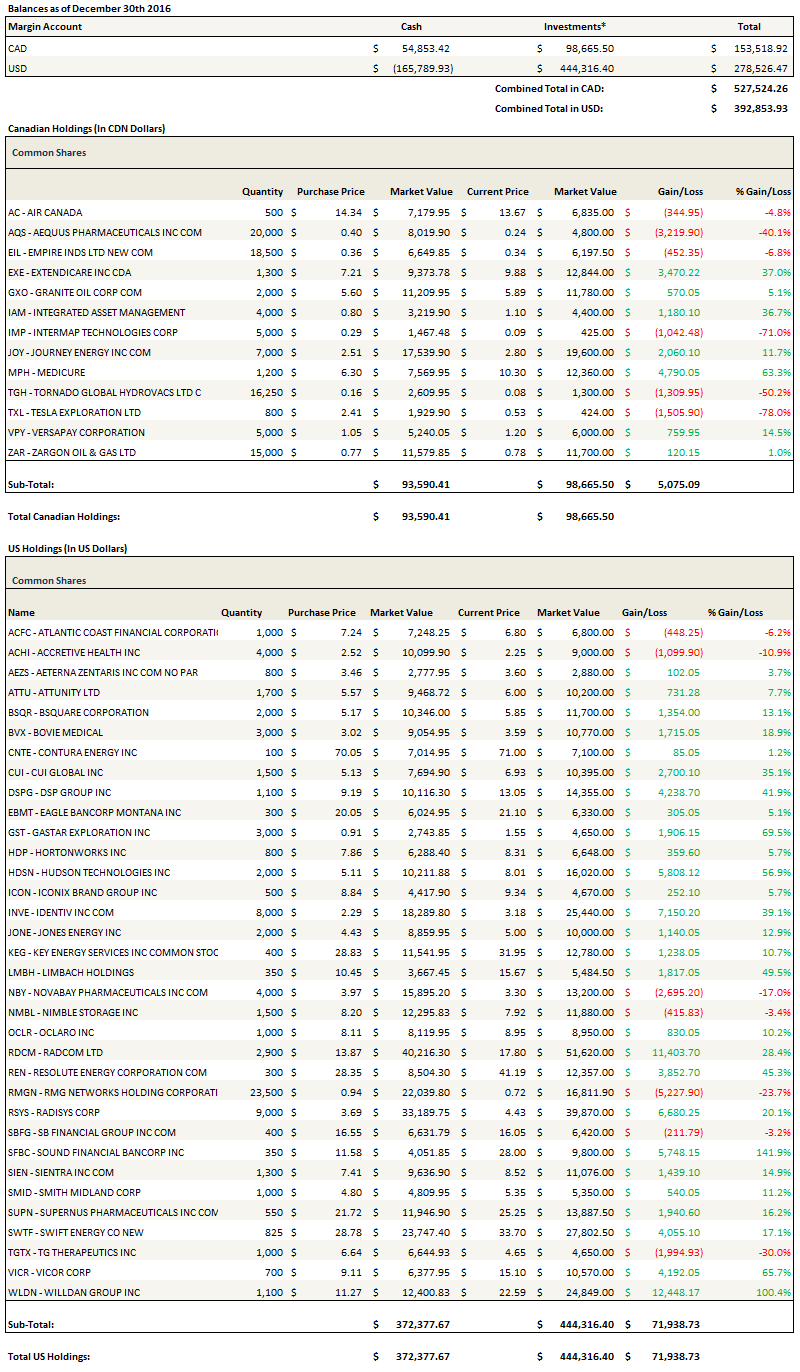

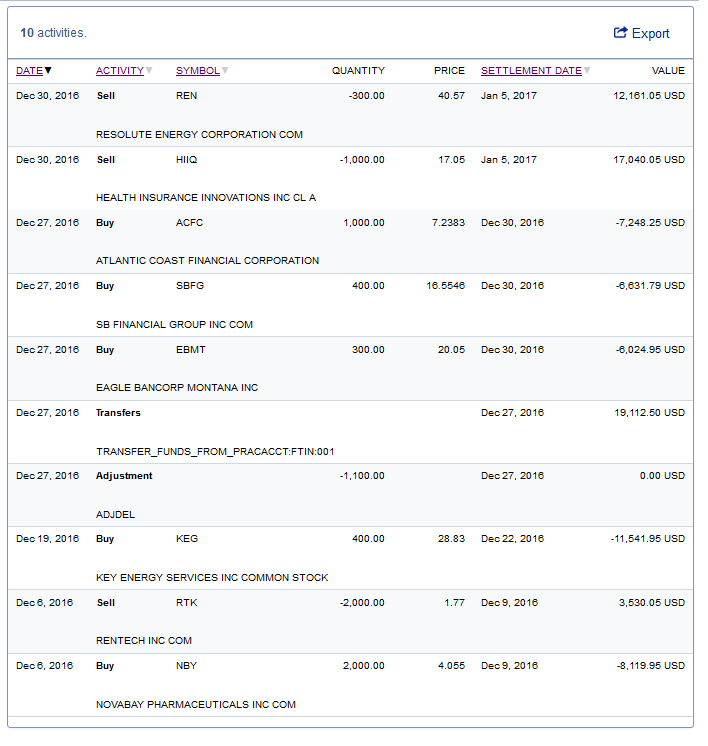

See the end of the post for my full portfolio breakdown and the last four weeks of trades

Thoughts and Review

The other day I was considering posting an article on SeekingAlpha. I couldn’t muster the energy. I wasn’t sure why, but I felt a strong resistance against it.

So I put it aside and in a couple of days it came to me why.

Take a look at my SeekingAlpha history. I’ve written a few articles for it. The list of names is, at best, uninspiring. Hercules Offshore went bankrupt not long after I wrote about them.

The fact is, I’m wrong a lot. At least a third of the time I pick a stock it doesn’t even go in the right direction. In a bad market that number is likely well north of 50%. And even when I’m right, I often miss by degree. The last couple of months, while my portfolio has done pretty well, it would have done much better if I was not weighted most heavily in two positions that have done absolutely nothing (Radcom and Radisys). My biggest winners are often afterthoughts where credit should only be taken with qualification.

If there is one redeeming feature about my strategy it is that I am fully aware of my own limitations. I am never certain. In my blog write-ups I try to phrase every position in terms of what might happen, both the positive and negative, with the expectation that I may have the thesis totally ass-backwards. If anything, the limitations of the medium (writing) convey more conviction than I generally have.

This doesn’t play well when writing an article that is trying to convince others about what a great idea you’ve just found. It might be, it might not. Who knows. What I can say is that as long as I cut my losses quickly, it presents a pretty good risk/reward. But I have no particular insight into whether its going to pan out or not.

It doesn’t make a compelling narrative.

Nevertheless after another pretty successful year, despite a whole lot of mind-changing and almost constant self-doubt, I can say that it worked pretty well once again. To summarize:

- I freaked out in January when my portfolio lost over 10% in a couple of weeks.

- I only tentatively added back as the market bottomed.

- I sold out of the years big winner, Clayton Williams, about $100 too soon.

- I mostly missed anticipating the Trump rally apart from a position in Health Insurance Innovations and a couple of construction plays I bought in the days immediately following the election.

- (As I will describe below) it only donned on me that community banks should be firing on all cylinders in the last few days.

Yet I’m up about 35% since July (my portfolio year end) and about 40% in 2016 (though with the asterisk that it is with far less than $50 million in capital 😉 ).

Most occupations don’t tolerate excessive uncertainty. I am fortunate to be involved in one of the few that reward it.

The last Month

Last month most stocks in my portfolio stagnated. The gains I had were fueled by a few oil names (Gastar Oil and Gas, Jones Energy, Resolute Energy) as well as Health Insurance Innovations, Identiv, DSP Group, and a last day move back up by Radisys.

Health Insurance Innovations has been a big winner for me. If only I had bought more! The stock has more than doubled since Trump took office. I sold some of my position in the last days of the year (I mistakenly sold all of it in the practice portfolio so that is why it doesn’t appear in the list below).

The second big winner has been Identiv. Unlike Health Insurance Innovations, I have not taken anything off the table. Identiv remains quite cheap, with only a $35 million market capitalization. There is a rumor that after a presentation given at the Imperial Conference the company suggested some recent business with Amazon, which, if done in mass, could be quite a big contract for the company. I have no idea if its true though. The stock has pulled back in the last few days, but I’m not too worried. As long as business continues along its current trajectory, the stock should do well in the coming year.

Key Energy Services

In mid-December I took a position in an oil services firm, Key Energy Services (KEY). I was given the idea by someone in the comments section of the blog. Key Energy operates a number of well services rigs, as well as having businesses in water management, coil tubing, and wireline services. This is a tough business, and has been a disaster over the last two years. At least 3 competitors in the space have been through bankruptcy.

At the time I bought the stock it was still trading in bankruptcy. Similar to Swift, existing shareholders received a piece of the new company and warrants.

Since exiting bankruptcy in late December the stock has traded up quite a bit but I think there is still some value there as oil services demand rises. What I remember from past cycles is how leveraged these companies are to improving fundamentals. They gain on both pricing and volume. With both natural gas and oil moving up, this may be the first time since 2012 where Key Energy has had pricing of both commodities as a tailwind.

The company has reduced its G&A, reduced interest expense via the bankruptcy process, and is the first of its brethren to make it through the restructuring process.

On the negative side, its a low margin business, I don’t get the sense that management was particularly astute heading into the slowdown, and in the current pricing environment even after restructuring they are still EBIDA negative.

Nevertheless I am willing to see if I can ride the cycle here. Its probably no multi-bagger, but I am looking for a move into the $40’s where I would sell.

Community Banks

The last thing worth mentioning is that after a month and a half of rallying, and the astute comment of Brent Barber asking me why I wasn’t looking at them, I finally spent some time on the community banks. Its soooo obvious, its painful to think that if I had spent a few hours on November 9th I would have quickly realized the same conclusion and ended up a number of dollars richer as a result.

Nevertheless, a good idea is a good idea. Though the names I bought are up between 10-20% in the last month and a half, I still think they have much further to run. I added positions in SB Financial (SBFG – former Rurban Financial, which I’ve talked about in the past and owned a small piece of of for some time), Sound Financial (SFBL – another bank I’ve owned for years), Atlantic Coast Financial (ACFC – which I have owned and written about in the past), Home Federal Bancorp of Louisiana (HFBL), Parke Bancorp (PKBK), and Eagle Bancorp of Montana (EBMT). I took a basket approach because all of these namess are illiquid and difficult to accumulate in too much size. I will write these up in more detail shortly.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

I am currently reading a book (Your Money & your brain by Jason Zweig). This blog would be a perfect illustration of of some of the main thinking of the book. My best ideas or concentration of the portfolio often gave me heart aches.

I really enjoy reading your blog and thank you!

Baiyang

Thanks, I actually have read that book, it was a couple of years ago though. I really enjoyed it at the time but don’t remember the specifics. It wouldnt surprise me if I’ve subconsciously integrated some of his ideas into my own thinking.

just bought myself some novo nordisk, expect to make 100% spread over a few years, since they still are the 800pound gorilla on insulin medicine (diabetes), owning 50% of the global market in volume and 30% of the global market in sold $ turnover, while sitting on 10 Billion plus in spare cash and no debts and 30% plus net operating margins and 70% plus ROE. Having a 4.5 Billion share buy back program started in early November, while the share value has collapsed from $50 to $37 in six months because of FDA changes that will impact it’s USA growth prospects, is a nice plus to enter it right now. Market over-reacted, and now it is close to a price-to-book of 1, and the right time to get into a market leader noting at bargain prices in a sector that will double in users in a decade (diabetes can’t be cured, you must absorb insulin for the rest of your life at current medical levels). Novo nordisk is globally active, and as such not dependent on one country.

OOPS, the price to book is wrong, it is 15. Meant the PEG ratio is near 1, which indicate a strong grower with outstanding financial profitability conditions.

http://www.gurufocus.com/stock/NVO

Hi Al, PEG is far above 1. NOVO has downgraded their Growth expectations a couple of months ago to something like 5-7% if I reacall correctly. 15% grown was what they expected a year ago ;o)

Casper, PEG is still 0.97 according to gurufocus, which reviews quarterly, and morningstar is saying it is 2.4, who is right ?

http://www.gurufocus.com/stock/NVO

http://financials.morningstar.com/valuation/price-ratio.html?t=NVO®ion=usa&culture=en-US

That being said, Novo officially said in February 2016 that they have decreased their growth rates from forecast 10% to now officially 5% for the long term, which led to a share price collapse from $57 to now $35, with lowest point $30 reached in between.

Wall Street value investors think it is fairly valued at $30 right now. I bought at $33 mid December 2016, or 10% above estimated fair value.

Given that diabetes is still incurable right now (sorry for the ones suffering from this issue) and more people are getting diabetes every day because of unhealthy food intake habits (too much sugars and fats), I am not really focused on a sales growth rate. I ain’t that morbid, you know. Prefer to see many healthy people around.

I try to invest in corporation with a decent dividend payout % (which novo has) and that won’t go bust at the first serious market crash (which novo won’t), while providing a decent margin of safety under any scenario (which novo provides, given that this corporation is still market leader in it’s sector, share price has now gone down 40% before I bought, while novo is now still sitting on 18 Billion plus in cash, has less than 1 Billion in short term debt and zero long term debt on it’s balance sheet).

http://financials.morningstar.com/ratios/r.html?t=NVO®ion=usa&culture=en-US

Add to this already potent mix some 4.5Billion recently being spent in buying back some shares and a ROE above 70% even with zero sales growth rates, means I sleep very well.

The 5% growth rate is still a very nice figure for a market leader in incurable diabetes medicine supply, and a ROE above 70% certainly will lead to better valuation ratios down the road if share price doesn’t move up in the future. And given that I intend to keep this one for the very long haul, having entered at a much lower price, I am patiently awaiting this ROE to do it’s work, while cashing in the 3.8% in dividends year after year after year.

The 3.8% dividend certainly beats the 0.1% in interest rates I receive on my savings account right now… (I live in Europe).

Of course everybody does what he wants with his money, and of course, novo now only represents 5% of my stocks portfolio, as a start. I will see what happens in the future, before eventually increasing this %.

I merely shared on this site, since I also get free advise from this site. Everyone has to do his homework before investing, and sharing stuff creates a virtuous circle, since this blogger also put up time to write his blog, and I am merely returning the courtesy with my comments….

What you need to know from the 20-F document page 3 year 2015 with link here under:

From 2011 to 2015, evolution:

. # shares outstanding from 2900 to 2600 million (share buyback program in place)

. net sales from 66 to 107 Billion

. net profit from 17 to 34 Billion (30% plus NET profit margins…)

. earning per share from 6 to 13,5

. dividend per share from 2,8 to 6,4

Click to access Form%2020-F-AR2015.pdf

http://www.novonordisk.com/about-novo-nordisk/novo-nordisk-in-brief/facts-and-figures.html

Thanks I will take a look at it. I’ve been looking for biotech names as we end the wash out in that sector.

hereby a link to another set of good recommendations for 2017, hope you find it worthwhile. Read the 2 pages to get a good overview.

http://roadmap2retire.com/2017/01/top-investment-picks-2017/

I think the way you describe feeling is the way most successful investors feel. It’s just part of the cost for being successful in the field. People who are supremely confident in investing either are talking history or usually end up broke.

I am still long all of my regional banks and think this is a multi-year trend.

If you want to buy cheap really financials now, you might want to take a look at the European ones. Europe seems to be turning up and theirs are much cheaper. I am currently long AEG, NNGPF, ING, DB, SCBFF. All are far under book value (except ING, which is more of a GARP pick), and are cheap on earnings or have the potential to be very cheap on earnings, and they mostly pay good dividends.

I’ve never really been a big financials investor, but seems like such a good risk/reward sector compared to the market right now, I think due to people’s continuing fear from the financial crisis.

Thanks Brent – I’ll take a look at these names. I agree that this is a multiyear trend. It probably will slow here for a few months though given the big moves in the last couple.

Good post. I wish more people thought this way about building a portfolio of undervalued stocks and looked at the expected value of their investments.

If you’re looking at community banks because of a rise in interest rates, you might also want to take a look at insurance companies.