SB Financial: Like watching paint dry

This is the first of some short write-ups on the community bank stocks that I have invested in over the last month. I mentioned in my portfolio update that I had thought the community banks taken a basket approach, buying 5 names (some of which I had already owned a small amount of in some accounts for a long time). I’m not sure if I’ll write-up all of them, but I’ll try to do a couple.

My thoughts behind the trade are that pretty much all the community banks are going to benefit from a few tailwinds over the next year. These are:

- Higher interest rates leading to higher net interest margin

- Lower taxes (most community banks pay over 30% in tax)

- Reduced regulations (reduced compliance costs)

- Better economic growth and a better environment for loans

I want to preface this write-up, by saying I don’t really know if any of the banks I have invested in are the best way to play a rise in community/regional bank stocks. There are so many bank stocks out there. I can’t possibly go through them all. I have a list of about 40 that I looked at and I picked 5. 20 were small and 20 were larger names that I was looking at for baseline. The stocks I bought were those that compared the most favorably. They also seem reasonably priced to me. But there may be (likely are) better ones out there that I just haven’t heard of.

I’m starting with SB Financial (SBFG), which is the new name of a long time holding of mine Rurban Financial. I actually wrote about the stock first here, almost 5 years ago! Its probably the name I like the best out of all the stocks I bought.

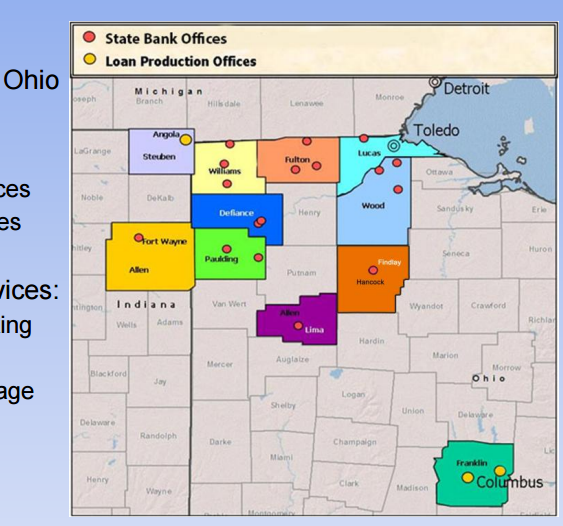

SB Financial operates primarily in Ohio with 18 branches, though it does have a branch and loan office in Indiana and another loan office in Michigan.

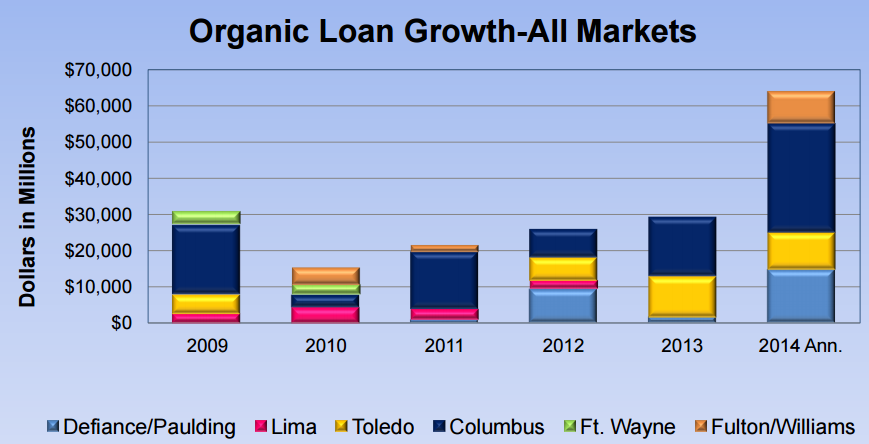

Overall loan growth in the last few quarters has been in the mid-teens year over year:

In a 2015 presentation they describe their growth markets as Defiance, Columbus and Toledo:

I haven’t found any newer data describing loan growth by market.

SB Financial is not as heavily into residential loans as some banks. Only about 22% of loans are residential. Most of their loans are either commercial, commercial real estate or construction loans. I know that construction loans are typically riskier, and the company does not break-out construction loans from commercial real estate from what I can see, so this might be seen by some as a flag.

Nonperforming assets are only 0.6% of total assets. So at least their history is one of prudent lending.

SB Financial generates a fair bit of non-interest income. Apart from the usual fee income, they have a mortgage origination segment that has been growing originations over the last year (up from $86 million to $117 million year over year in the third quarter). While rising rates will have an impact on this business, on the third quarter call the company said that 88% of originations were new money, so refi’s are only a small part of the business. The company also holds a position in mortgage servicing rights that will perform well as rates rise, offsetting the impact of reduced refinancing.

Other non-interest income is generated by the asset management business. Assets under management (AUM) grew to $376 million in the third quarter, which is up 11% year over year. Fee income was $700,000 for the quarter, so their fees are around 0.7-0.8% of AUM annualized.

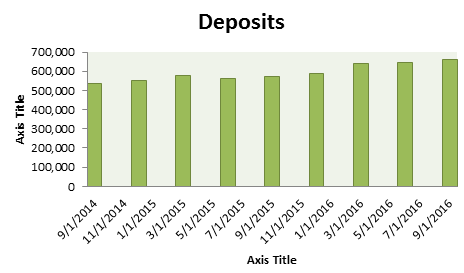

To fund their loan growth the company growing its deposits by adding branches. At the beginning of 2016 they expanded full service banking into Columbus. On the second quarter conference call, they have pointed to a strong start for deposit growth in Columbus, up $5.8 million in first 6 months, 43% since the beginning of the year. The company is planning a similar full service entrance into Bowling Green in the fourth quarter of 2016.

In the past few quarters deposits have been growing at a similar rate to loans, 15% year over year.

SB Financial trades at 146% of tangible book value. They have some goodwill on the balance sheet, which makes their price to book a little lower, 130%. The P/TB is the highest of any of the banks I bought. However they have been the best of the bunch at allocating capital. Return on assets in the third quarter of 2016 was 1.28% and was 1.1% for the first 9 months of the year. Return on equity was 11.9% and 10.3% respectively. I have read that if ROA is above 1% and ROE is above 10%, the bank is doing a pretty good job.

The addition of new branches has likely been a drag to earnings. The company’s efficiency ratio (this is the ratio of their operating expenses to revenue) was 68% in the first 9 months, which is average at best. However as they build the branches I would expect this to come down.

The company reported $1.01 EPS in the first 9 months and 40c in the third quarter. They trade at a little under 12x earnings on an annualized basis of the 9 month numbers. That doesn’t seem unreasonable to me given the 15%ish growth that they are producing.

I’ve owned this stock for 5 years and its given me no surprises. I don’t expect one going forward. Its like watching paint dry, and that’s OK.

I expect the company to keep on generating returns on assets similar to the past, continue to build out its deposit base into new markets (first Columbus, then Bowling Green) and grow fee income through asset management and mortgage originations. Simple story. Hopefully with an additional boost from a federal government policy revamp the stock can trade up to 2x tangible book.

Building new physical branches sounds kind of weird to me. We seem to be heading towards more digital payments: Venmo, PayPal, etc. I personally hate going to the bank. It’s a pain in the butt. You have to take time out of your day to drive to a special building, then wait in line, just to access the resources that you have already earned and own.

It seems to me that scale would also serve as an advantage for the major banks, but I have trouble seeing how the local community banking model can survive. What gives you confidence that a lot of these local banks are not going to feel the pain from online financial tech companies like Sofi and LendingClub? I would think that less regulation would make the incumbents more vulnerable to disruption from companies with the scale and capital resources to touch every potential customer digitally.

I read your blog pretty religiously, but I have trouble getting excited about local banks. Am I missing something here?

Thanks,

Forrest

I understand your point with respect to branches. Nevertheless, these community banks, not just SBFG, are adding branches and those branches are growing deposits. Keep in mind they aren’t typically building a branch, just occupying space in an existing building. When I think about it though, if I’m a consumer Im either going to fall into one of two categories, there is your sort of category, in which case I am probably not even going to look at a community bank, because they aren’t going to have the web services that I want and so really you aren’t a prospective client anyways, and then there is a second category of customer that wants higher touch, and one of the first thing these customers are going to look for is where the nearest branch is. So I can see the value of having the branch. The other side of it is on the loans, where you want a presence in the area to be able to make loans to local businesses.

Why won’t they feel pain from online lenders? I guess my answer would be why haven’t they yet? And if they haven’t yet, what is going to be different in the next year to make them suddenly feel pain from these lenders?

Finally, this isn’t really an exciting idea. But if you start running numbers on what happens if these banks see their tax rate slashed and their NIMs inch up, their earnings get a lot better. I cant quantify the effect of lower regulations but its something. Meanwhile you are seeing takeovers at 2x+ book and these guys I am looking at are all well under that, most are 1.2-1.3x book. So if the value is seen we might expect some consolidation of these smaller players.

Very helpful thanks. PKBK had popped up on a couple of my screens so I was intrigued to see that you bought it as well. Keep up the great blog!

This article seems to support what you were alluding to. Thanks for the response.

https://ftalphaville.ft.com/2017/04/12/2187388/small-businesses-hate-fintech-lenders-more-than-big-banks/