Oclaro Second Quarter Update: No sign of the inflection yet

I’ve owned Oclaro since last spring, first wrote about the company here, and subsequently here. Oclaro has their year end in June, so the company recently reported their second quarter results.

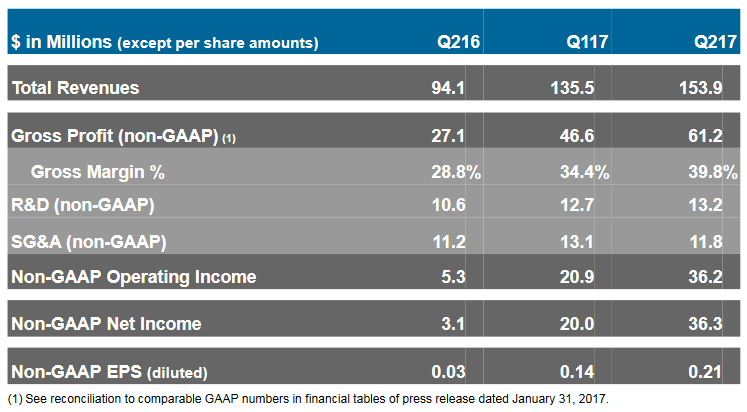

Oclaro had another very good quarter, which had been expected after a preliminary announcement two weeks prior. Revenue grew 14% sequentially and 64% year over year. I calculate that adjusted EBITDA was $41 million in quarter, more than double what it was in the first quarter.

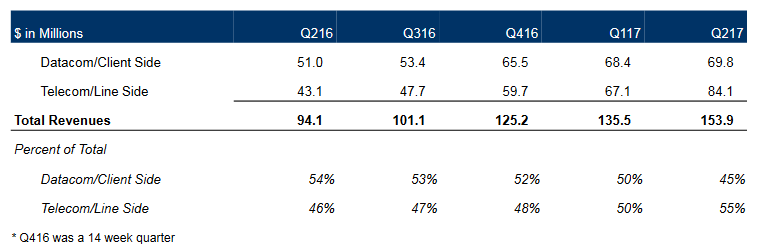

Digging a little further, the growth came almost entirely from the telecom/line side of the business. Just to recap (see my earlier posts for more details), Oclaro makes transceivers and laser components that are used for optical data transfer. Oclaro divides this business up between a client side, which consists of shorter length lasers (they have names that start with CFP or QSFP 28), and line side, which consists of longer length lasers of which the most significant is their new CFP2-ACO product. Below is the breakdown between the telecom and datacom sides.

Growth coming from telecom/line means that the aforementioned CFP2-ACO product was responsible for much of it. This is a relatively new transceiver (see here for a bit of background) that was pioneered by Oclaro. Being first to market, they are enjoying a window of 100% market share as the competition races to develop their own versions of the transceiver. The CFP2-ACO was expected to be the growth driver in the quarter.

Competition is going to come into the market beginning in 2017, as the company conceded on the conference call. Acacia, Finisar and Neophotonics is are developing their own CFP2-ACO products.

Still Oclaro has a significant lead and has used their head start to lock down customers for this fiscal year (ending June) and their fiscal 2018. From the conference call:

[We] negotiated or are completing negotiations of several multiyear contracts or extensions contracts for some key product like the ACO that run as long as through calendar year 2018

The CFP2-ACO sales have centered on North America and Europe so far, but Oclaro did say on the call that they are seeing sales from China begin to pick up. China buys a lot of Oclaro products (40% for the quarter), and in the past these have been lower end of the spectrum transceivers (the modulators and lasers that go into the transceivers). China revenues for Oclaro grew 9% sequentially in the second quarter.

While the telecom side drove growth last quarter, the client side products continued their strength of prior quarters but are constrained by production limitations. The lower end CFP product remains sold out (probably in part because of China?). Oclaro hasn’t gotten as much traction on the higher end products (CFP2, CFP4, QSFP28) but they expect this to pick up, and they “do expect to shift [to] the CFP2, CFP4 and QSFP28 transceivers to accelerate through the summer”.

Its worth noting that the CFPX and QSFP28 will have lower average selling prices (ASPs) than the CFP, which could be a drag on top line revenue, but that margins for these products will be higher than the CFP, so the bottom line should improve.

At the Needham conference in January (here is the replay) Oclaro said that the growth of their business relied on 3 end markets: Datacenter, Metro 100G and China. There wasn’t anything on the second quarter call or in the guidance Oclaro gave to suggest any of these 3 markets have slowed yet.

For the third quarter Oclaro guided $156 million to $164 million, which is another sequential increase from the $154 million in the second quarter. To a large degree growth is being driven by the sold-out conditions of many of their products. Management gave some color around how they would like to ramp production faster than they have been able to.

I’ll continue to hold Oclaro. I’ve expressed my concerns in the past about not knowing when this cycle is going to peak. The color I get from listening to the company and its competition is that we are still at least a few quarters off. There is much talk of consolidation in the space, and I would hate to sell just before an offer comes in for the company. So I will continue to management my uncertainty via a reasonable position size, and hold out for a selling price in the mid teens.