Radisys Fourth Quarter Update: Expected and Unexpected

I was bracing myself for a beat down when Radisys reported their fourth quarter earnings. And I was right!

There were two problems with the quarter:

- Guidance was poor

- The signs that guidance would be poor were ignored by analysts.

Let’s take a look at the signs.

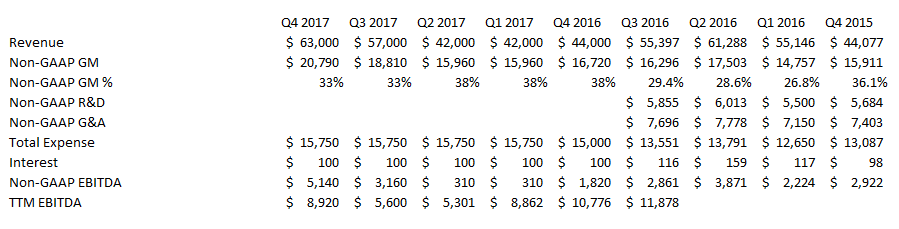

On the third quarter conference call Brian Bronson, the company’s CEO, talked about having low $40’s (in millions) of revenue in the first two quarters of 2017. In January Radisys disclosed an updated credit agreement where they made reductions to the EBITDA covenants for the first and second quarters that were consistent with a level of $40 million of revenue. Finally, if you took in the color around trials from the third quarter call and the Needham conference, you would be led to conclude that material revenue was unlikely before at least the second quarter, more likely the second half of the year.

So it was actually pretty easy to see what the guide would be for the first quarter and full year. I made the following estimates after reading through the EBITDA covenants of the credit agreement (but before the guidance was announced). I shared these thoughts in the comment section here.

My estimates turned out to be pretty close. They would have likely been even closer if it hadn’t been for the fall off in the legacy business (which I will get to in a minute).

Nevertheless analyst estimates heading into the quarter were much higher. Most had $50 million of revenue for the first and second quarter. So when the first quarter number came in lower, the estimates were slashed.

So that was a big part of why the stock has done poorly. But it’s not the only reason. The company also announced news that the legacy business revenue, referred to as embedded systems, would decline more in 2017 than previously anticipated. Embedded systems revenue is now expected to be $55 million in 2017. As recently as January Radisys had said it would be around $75 million.

Its unfortunate. But not crippling. The embedded systems business is not a reason to own Radisys. Its just a distraction.

The reason to own Radisys are the new products and services offerings. And here the company did okay, though not enough to offset guidance revisions and the negative perception around embedded.

My hope for the quarter was a firm new order for DCEngine. Given where Radisys had stated they were in trials I knew this was a long shot. Indeed, no such big announcement came to pass.

Instead they gave a positive but mostly qualitative update. Here’s a summary:

- Making progress with their North American Tier 1 communication service provider (CSP) that is in trials with their DCEngine rack – they have three DCEngine units in the lab and Radisys expects commercial revenue could begin as early as the third quarter.

- A second DCEngine trial with a customer that will be, in turn, selling to a Tier 1 customer who I am guessing is AT&T, giving Radisys a foot in the door there.

- A new FlowEngine use case for an existing customer (Verizon?).

- In Europe, an expansion of the existing hardware and services contract with the Tier 1 (this was a contract related to the open-source Central-Office-Redesigned-as-a-Datacenter or CORD initiative that I wrote about in my earlier post on Radisys)

- Also in Europe, a new Tier 1 engagement again revolving around CORD.

Overall the company said they were ahead of their plan to have 10 tier one engagements by the summer.

It’s all directionally positive, but as of yet there has been no big win to add to Verizon and Reliance Jio. And its clear that color alone is not going to move the needle unless revenue can be tied to it.

So what do you do from here?

I’ve waffled a couple of times but in the end have added a little to my position. I think the bad news is most likely out. We know from the Needham conference that the European CSP engagements are initially targeting professional services around CORD but that they will likely include a DCEngine component as well (if you go back and listen to the Needham conference again the language is pretty clear: expect that little can be announced by the February earning call but that more engagement with this CSP, around DCEngine, is to come).

We know that the new FlowEngine product will be launched mid-year and in fact a press release just came out today that it is now available for field trials (this is ahead of the end of March date they had previously suggested). We know that Verizon (and likely others?) are waiting on the new version before purchasing more FlowEngine products. Interestingly, Radisys mentioned Gigamon, F5 and A10 as competitors whose space they looked to infringe on with this new product.

There was a press release earlier this month describing a partnership with China Unicom to build open-source PODs for mobile 5G. If this is successful one would expect follow-on orders for DCEngine. China Unicom is a very large service provider.

And finally there was a second press release today describing a new 5G RAN version of Cell Engine. It is probably not coincidence that also today CORD and xRAN announced project alignment. Three large telecoms, AT&T, Deutsche Telekom or SK Telecom, are all mentioned in the release. Radisys mentioned that the new Cell Engine was “developed in close collaboration with a leading mobile operator”, likely one of the three mentioned in the CORD/xRAN collaboration.

Away from the news flow and looking at numbers, when I parse the guide for 2017 it’s not hard to spin it bullishly. We all knew the first and second quarters were going to be poor, low $40s revenue at best. But given $40/$40 (million) in Q1/Q2 the implied Q3/Q4 guide is a range of $55/$55 to $70/$70 (million). These are solid revenue numbers particularly given that they are going to be more heavily weighted to the new products than in the past.

So I’ll wait. Some more. But as so many of the other positions in my portfolio scream higher (Identiv, Combimatrix, Hortonworks, Ichor and Attunity of late) and I still sit with a decent percentage of my portfolio tied up in Radisys, I certainly hope it’s worth it.