Adding to one of the few ideas that is working: Empire Industries

My portfolio has been behaving poorly over the last month and a half. I’ve had very little confidence to add to positions in the face of these headwinds. That said, one of the few positions that has bucked the trend and that I have added to is Empire Industries.

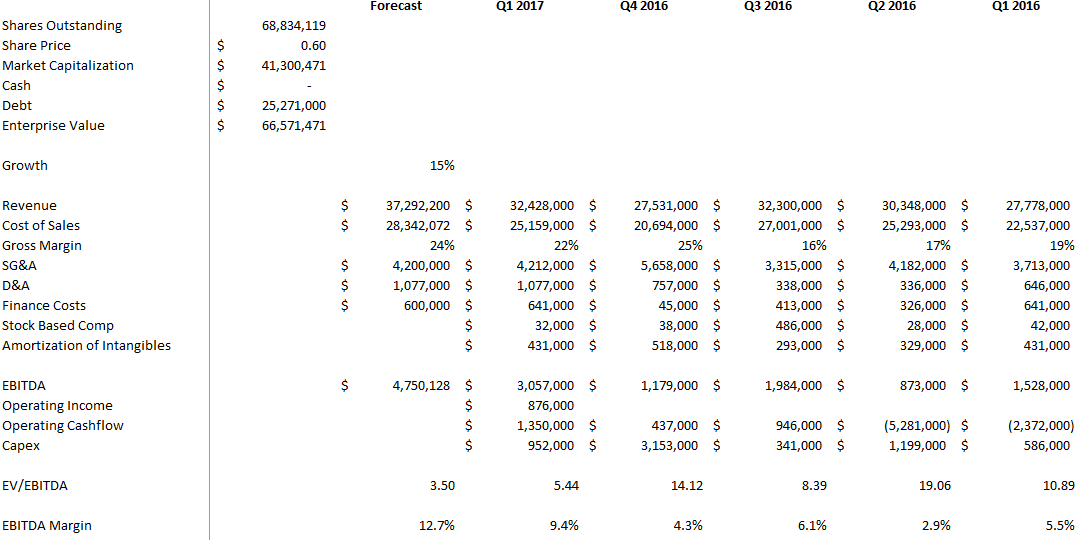

Empire reported its first quarter results at the end of May. The results were a step forward. The company had $32 million in revenue, which was up significantly from the fourth quarter but fairly consistent with the level of the previous few quarters. Gross margins of 22% were an improvement over the last few quarters, as was the EBITDA margin of a little over 9%. The gross margin number has been improving of late (they had been in the high teens up until the last couple of quarters) as the company has shifted toward manufacturing the second generation of their attractions products and moved away from custom designs. On the call management suggested that this level of margins, and maybe a little higher, would be sustainable going forward.

Along with the results the company announced the wind down of the steel fabrication business. Some of that business will be moved towards providing support for Dynamic Attractions, while the rest has been shuttered. Given that the business lost over $2 million last year and allows them to cut $1 million of overhead costs, I’m not sad to see it go.

I thought that Guy Nelson, Empire’s CEO, was particularly positive on the call. He said that the “market for our immersive attractions is growing rapidly”, the Q1 results “prepare the company for strong results in the future”, and the backlog is “indicative of how we are the supplier of choice among the world’s top theme parks”. They have “a record backlog of proposals in our pipeline” and its “safe to say that you can look forward to more contract announcements in the future”.

The big news that was announced just prior to earnings of was the $125 million four year contract announced earlier in May. This is a huge contract, much bigger than previous contracts that have been in the $30-$50 million range. They said they believed it was the biggest contract ever announced in their industry. I honestly was surprised that the stock didn’t move higher on this news.

As I already mentioned, Nelson said on the call that it was “safe to say” there would be more contracts in the future. True to his word, the company announced a $40 million USD contract with an Asian theme park operator last week. Again, the stock popped on the news, but remains more subdued than I would have anticipated.

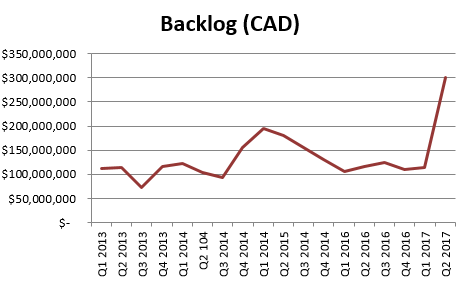

Including both of these new contracts, the companies backlog stands at roughly $300 million (CAD).

So what does that mean? Well, at the current share price (~0.60c) Empire has a market capitalization of $40 million. Add on $25 million of debt and the total enterprise value is $65 million. For that price you get a company with trailing twelve month (TTM) revenues of $132 million, so the stock is trading at a little less than 0.5x TTM sales.

In the past you’d argue back that Empire’s businesses are low margin, so the multiple should be low. But with the wind down of the steel fabrication business and the spin-off of the hydrovac business, and with the shift to higher margin second gen products for Dynamic Attractions, this is less the case now. Gross margins for Dynamic Attractions are still low, but they are no longer mid-teens. They are now over 20% and maybe can tick even a couple of points higher as they increase their second generation business and integrate the in-house manufacturing of their remaining steel fab assets.

Moreover, revenues are likely to grow over the next couple of years. The $300 million in backlog is double its peak level over the last few years. Over that time Empire has operated Dynamic Attractions at a revenue level that has been about ~80% of backlog (Dynamic Attractions revenue has been about $100 million annually while the backlog, while volatile, has fluctuated around the $120 million level). Given that the backlog has now doubled, how much can we expect a commensurate move up in revenues?

It may have made sense for the company to trade at a low multiple when the steel business and hydrovac business were revenue drivers, when the media attraction business had lower margins and a smaller backlog and thus some uncertainty around its sustainability. But now, with a backlog of over $300 million (or more than two years of revenue at the current rate) and when it’s “safe to say” there are more contracts coming, it just doesn’t make sense to me.

So what’s it going to take to move the stock? Well I think that one thing holding back the stock is its accounts receivable. So far we haven’t seen revenue convert into cash. The company has accounts receivable of $37 million. This is actually an improvement over the 3rd quarter of 2016, when it was as high as $44 million. That means days sales outstanding is 111, which seems very high to me. It also means that the company has to maintain a lot of bank debt in order to balance their cash needs.

Also helpful would be one more contract to just put them over the top, and maybe a another quarter showing similar or hopefully even better gross margins and 10% conversion to EBITDA.

When I model out how the business could improve further, its not too difficult to see EBITDA getting to $5 million quarter. As I show below, assuming the same operating costs as the first quarter, a 15% jump in revenue (which shouldn’t be out of line given the large increase in backlog) and a couple basis point improvement in gross margins (brought on by the continuing shift to second gen products and the wind-down of the steel fab business), and you are almost there.

But we’ll see. So far there are sellers in the mid 60c range that have to be overcome before any move higher can take place. The stock has languished for years. The current price movement may simply be a function of a few legacy holders taking the opportunity to get out. Whatever the reason, I’m willing to bet that there is a reasonable chance that the stock moves higher in the coming months.

I am wondering why you think the hydrovac business should not trade at a high multiple? If you look at Badger, even after the short report, the stock still is trading at 17x EPS 18. It also seems like the oil patch is bottoming out. The US rig count has been steadily increasing so you would think that valuation is pretty attractive.

Well in the past the gross margins on the hydrovac business have been pretty low, often less than 10%. In the first couple quarters of 2016 they dropped to less than 5%. So when Empire owned that business, particularly through the second half of 2015 and first half of 2016 before the spin, it was pretty low margin. However in Q1 2017 GMs jumped to 15% so that is more a level that I am comfortable with. I think the hope is that this China JV can drive better margins.

Badger doesnt make trucks though. They buy the trucks that companies like Tornado make. So its not the same thing. But again, I think what they are trying to do in China is start a business like what Badger does here, so if they are successful then your comparison is apt.

Have they ever disclosed who their customers are? The strange situation with accounts receivable almost makes me believe the customer in China might be a related party to the Empire Chinese joint venture partner, and the worst case would be that Empire is being used to help the buyer’s cash flows on terms favorable to the buyer.

It is very risky for such high cost projects to be exposed to nearly four month receivables. Aside from this one issue, I just love this company’s product and positioning. If they could fix the accounts receivable, while simultaneously pushing sales north of $200M/year, this would fly.

Trade receivables have dropped significantly. How could they reduce unbilled contract receivables down? Isn’t this going to remain high as long as they are doing work? I don’t understand how they can “fix” this?

Good point on trade receivables. I guess my expectation on any capital project is that at least 40% of high-cost construction work should be prepaid, and they could defer recognizing that as revenue until the work is complete. Then at the start of each new milestone, there should be a 40% prepayment of that milestone. That covers cash flow without accelerating revenues as long as they defer revenues to completion of work.

I went over to the 2016 annual report to try to see what their practice is on prepayments, and Notes 5 and 6 do NOT seem to discuss this issue. Have you seen any discussion of their prepayment requirements before starting work?

This issue is probably critical to their ability to grow. Literally one huge contract could challenge their solvency by exhausting credit lines and putting them under a lot of financial risk if the buyer backs out. Since their growth very sporadic, they need a model where they can cover enough of their costs at each milestone to minimize their financing requirements.

I don’t understand – Their projects take 12-18 months to complete and revenue is around $120mm right? Can you show the math you used to show that there was less than 40% prepayment of a given milestone? How do we know how many milestones there even are? Thanks.

Let’s do some math and maybe you can spot my mistake. Assume a $120M run rate and they break work into four three-month parts with a 40% prepay. That’s $30M per quarter and $12M prepaid, $18M in accounts receivable for construction work.

To argue the math in favor of your point, you could break things into two six-month work cycles, in which case it is $60M per half-year, and $24M prepaid and $36M in receivables.

Structuring work into shorter cycles with 40% prepay each cycle might be enough to overcome this problem.

But rather than speculating, probably I should just ask their IR, and it would be great if they discussed this issue in depth in their reports. (Do they? Maybe I missed it?)

yeah that is exactly what I was getting at. It totally seems to depend on how they break up milestones.

The other consideration is deferred revenue which is cash they are getting for work they haven’t done. That number grew in Q2 to $22mm. So net unbilled less deferred was $14mm which is lower than its been in a while.

I think the deferred revenue jump is a big upfront cash influx from the new contracts they signed in May. But I’m guessing there.