TeraGo Networks: Inexpensive with Potential Upside from a Hidden Asset

The Straightpath Analog

A few years ago I owned a company named Straightpath Communications. I didn’t buy the stock directly; Straightpath was a spin-off of another company I owned called IDT. To be honest I did not even know IDT had these assets when I bought the stock.

The two assets being spun-off into Straightpath were obscure and hard to value. Neither generated any revenue. One of the assets was IP for various telecom patents. The second was license spectrum for very high frequency telecom bands.

It was not clear whether either of these assets would ever be worth anything. I don’t think investors understood them. I likely would have sold my shares immediately if it were not pointed out to me by a friend that Howard Jonas, IDT’s CEO, had put his son in charge of the business. Why would you put your son in charge of a junk business? So I thought maybe there was something there.

Straightpath did pretty well in the coming months, mostly on speculation that something might come out of one of these assets and not really because of any particular news or development that I could see. Because I did not really understand what I owned, I decided to sell the stock when it doubled. I believe I sold my shares for $15 or $20.

Flash forward 3 years and Straightpath was taken over by Verizon after a bidding war with AT&T. The price tag was $190 per share! Talk about leaving money on the table.

So why recount this depressing little tale of money not had? Because the Straightpath conclusion is relevant to a little Canadian company that owns similar high frequency spectrum licenses major metro areas through-out Canada. TeraGo Networks.

Terago’s Business

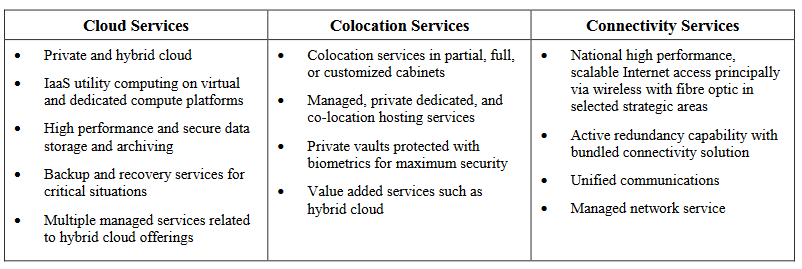

Terago Networks operates two lines of business. They provide data center services (see Cloud and Colocation services below) and they provide data and voice communications (Connectivity services below).

The business that owns the spectrum assets is the data and voice communications segment. The company offers internet access, unified communications redundancy to small and medium businesses across Canada. It does so by operating a wireless and fiber network within a number of large metropolitan areas. This is the weaker of the two businesses, as it revenues have been declining for the last couple of years.

The wireless access service they provide is in part via high frequency spectrum, for which they own the license to. TeraGo owns spectrum in the 24GHz and 38GHz range. I will give a more detailed breakdown of their spectrum assets a little later on.

A new Use Case High Frequency Spectrum

TeraGo kind of backed into ownership of this potentially valuable asset. Because the spectrum is high frequency, it has traditionally only been used for short distance communications, like fixed wireless, which is what TeraGo uses it for. TeraGo bought the spectrum to fill out their WIFI network in commercial and industrial parks so that its small business customers could have an alternative to purchasing connectivity services from a large communication services provider (CSP) like Shaw or Telus.

However because of the continuing growth in data traffic, CSPs are looking for ways of increasing their capacity for data transfer. Rather than deploying more fiber and network equipment into densely populated areas, an alternative is to leverage technology advances that have allowed for high frequency spectrums to be used for short distance mobile wireless capacity.

Take any downtown core. More office occupants are using their cell phones to watch videos and use apps. As more internet-of-things functionality takes off this will be compounded by additional data streaming from smart devices. Service providers have to add capacity to deal with the increase in traffic. One of the ways they can do this is by adding small cells, which are low powered radio access nodes that provide coverage over short distances. These small cells use the high frequency spectrum (like what Straightpath and TeraGo have licenses for) to transmit both “last mile” services to devices, and to “chain” together and relay data to base stations without the CSP’s having to lay costly fiber.

Before the Straightpath acquisition there was a lot of uncertainty about the value of high frequency spectrum. In fact there was a very high profile short-seller called Kerrisdale that wrote multiple articles (this one for example) on why Straightpath’s spectrum assets were worthless. Reading these articles in retrospect is informing. Its clear that there was a case to be made that technology limitations would make high frequency spectrum uneconomic. Nevertheless it was also clear that large telecom players were spending significant research dollars to determine whether this was the case. When Verizon bought Straightpath for such a large premium, and when both AT&T and Verizon were involved in a bidding war for the assets, it gave a very positive answer to those questions.

What this suggests to me is that in this respect TeraGo’s assets are significantly derisked from where they were a few months ago (I italicize “in this respect” because other concerns remain, as I will get to shortly). It’s the same technology up here in Canada, the same spectrum, and populated Canadian areas are going to run into the same bottlenecks that their US counterparts are.

Approval of Spectrum for Mobile

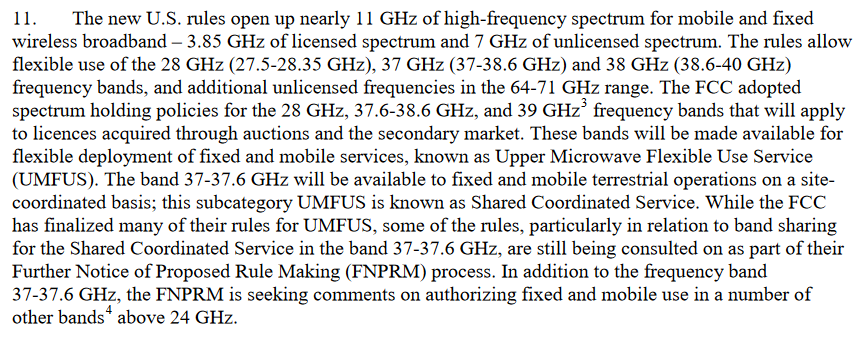

So the Straightpath acquisition derisks the technology, but there is still a hurdle remaining. The two spectrum ranges that TeraGo owns aren’t approved for mobile services in Canada. The United States is ahead of Canada, having already made approvals in July of 2016.

But Canada is moving towards approval. Innovations, Science and Economic Development Canada (ISED) released a consultation paper, “Releasing Millimetre Wave Spectrum to Support 5G”, in the last couple of weeks (the paper is dated June and I just found it a couple weeks ago so I think this is quite recent).

The paper is a first step toward getting spectrum approved for mobile services in Canada. It specifically requests for comment on the 38GHz band that TeraGo owns licenses to.

The 24Ghz spectrum, which is the other spectrum range that TeraGo owns licenses for, is not mentioned directly. This is because Canada is following the lead of the US, and there the two ranges approved so far for mobile usage are the 28GHz and 38GHz ranges:

But all is not lost for the 24GHz spectrum. The 24GHz band is one of a number of bands with an open for comment period by the FCC. Given the need for bandwidth, I wouldn’t be surprised if its approval just lags a little behind these other bands.

What will the ISED do with legacy spectrum?

So the ISED is open to restructuring the usage for 38Ghz spectrum and, as it follows the lead of the US, would presumably do the same with 24Ghz if the United States decides to open up that spectrum. But what happens to TeraGo’s legacy licenses in such a scenario?

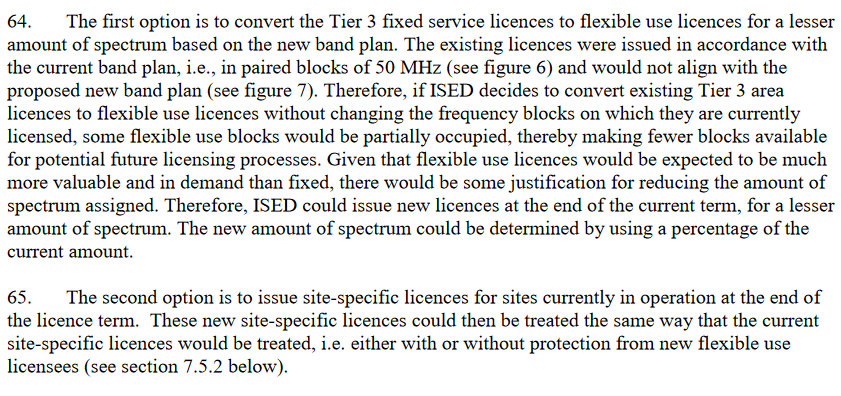

Right now Terago is licensed for its spectrum assets until 2025. That license is currently limited to fixed use wireless (as it was, until recently, the only use case for the spectrum). In the request for comment paper the ISED addresses what they are considering. They propose two alternatives.

The first option is by far the preferable one for TeraGo. They will lose a percentage of their spectrum on any rule change but still be able to keep the majority of it, which will be suddenly much more valuable.

The second option would see little benefit to TeraGo, but also is unlikely to be implemented in my opinion. It would be complicated. Protection means that Terago gets to keep the areas that it currently uses those bandwidths for WIFI, and other carriers could purchase licenses around those fixed sites. Having a network with gaps would be messy, and the ISED admitted in a later comment that they believe it could hold back 5G development. If there is no protection, TeraGo would basically have to compete with wireless signals in their areas which would likely not be good for performance for either them or the wireless providers. I simply don’t think this second option is going to be favorably received by anyone and I think its far more likely that the first is accepted. Also, the United States has set precedent by choosing a solution along the lines of option 1 though from what I can tell they made no clawback of existing spectrum in their decision.

TeraGo’s Spectrum

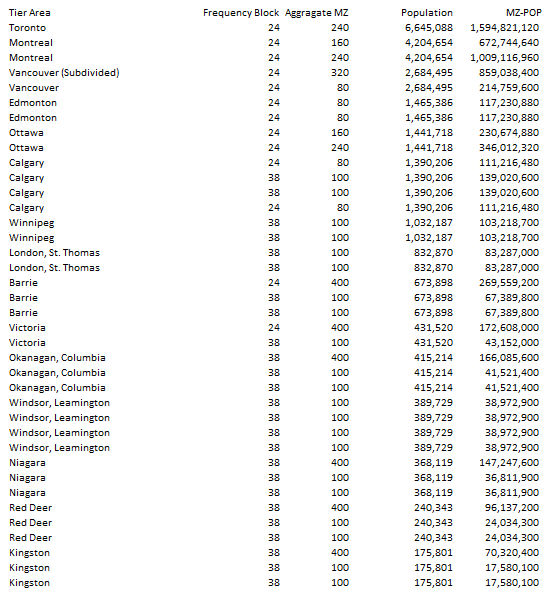

TeraGo owns spectrum in both the 24Ghz and 38Ghz range. Unfortunately it appears that the most valuable spectrum lies in the 24GHz range. Below is their entire spectrum holdings. Note that MHz-POP column is simply the previous two columns multiplied together. When Straightpath was acquired, many analysts valued their assets on a MHz-POP basis.

With its $3.1 billion bid for Straightpath, Verizon paid $0.017/MHz/POP for StraightPaths spectrum assets. A similar valuation for TeraGo’s assets would value the 24GHz spectrum at $100 million and the 38GHz spectrum at $29 million. The consolidate spectrum assets, if valued at the same level as StraightPath, would be worth over $9 per share. The 38Ghz assets alone would be worth a little over $2 per share. Then you need to start discounting that based on what spectrum you think will get approved and how much TeraGo will have clawed back.

Putting it all together

Terago has 14.3 million shares outstanding. Their market capitalization is $65 million at the current stock price of $4.75. They have $9 million of cash and $39 million of debt.

The $9 per share number is exciting. Of course there is a lot of uncertainty around that number. There is uncertainty about what ruling the ISED will make, uncertainty about when and if the 24GHz spectrum will be opened up for mobile use, and uncertainty about the attractiveness of spectrum in less dense populations like Windsor and Red Deer.

While obviously the uncertainty dictates that a significant discount be made to the $9/share number, I think the optionality of this playing out in TeraGo’s favor has to be worth something, particularly given the positive momentum already seen in the US and by the ISED.

Also worth noting is that the spectrum is really only marginally related to the existing business. The data center business has no dependency on the spectrum assets. The connectivity business has some dependency, however there are ways for TeraGo to provide alternative connection services if their spectrum assets are coveted by a CSP.

Meanwhile TeraGo’s valuation is not out of line when only its existing operating businesses are considered. The company trades at 7x trailing EBITDA and 12x trailing free cash flow. One third of their revenue comes from data centers that they operate and offer all the standard compute, storage and disaster recovery services from that other data centers around the world offer. Their data center revenue is derived from 7 owned centers throughout Canada. Revenue grew at 13% in the fourth quarter of 2016 and 8.5% in the first quarter of 2017. TeraGo’s larger peers in the data center and cloud services business (most of them in the United States), trade at between 16-20x EBITDA. Shaw just sold data center assets a couple weeks ago for 16.2x EBITDA.

The connectivity business has had some setbacks, but it still generates significant cash flow and has a reasonably stable customer base. Revenue has been declining in the 8-10% range over the last year. The company has been intentionally churning its low value customers and has also had headwinds in Western Canada because of commodity prices. On the first quarter conference call management suggested that recent marketing initiatives were beginning to take hold and revenue should be expected to stabilize.

While TeraGo doesn’t break out the business costs by segments, based on the color I have gathered margins for the businesses are reasonably similar. Therefore I’m assuming in the following that I can break out costs for each segment proportionally to revenue. If I do, I get about $4 million of EBITDA from the Cloud business and $8 million of EBITDA for the connectivity business. Even assuming a low end multiple for the Cloud business (15x EBITDA) and a fairly low multiple for the Connectivity business (6x) I come up with an enterprise value of $108 million, which would value the shares at around $5.50.

Its worth noting that these multiples work favorably over time as the cloud business grows and becomes a larger part of overall revenue and EBITDA. Also, given the recurring nature of the Connectivity revenue, if the business can be stabilized I think its reasonable to assume it deserves a much higher multiple than 6x EBITDA.

The point here is that the current price arguably doesn’t cover the value of the existing businesses, let alone any spectrum value that might be hidden in the assets.

So that’s why I own the stock. There’s probably no rush on this one, so I have added when the stock has been weak. Because the ISED is in comment period, a change of the rules is still some time off. The comment period lasts until September. I would expect another 3-6 months before we hear anything back from them on the matter. The next quarter is as likely to be weak as it is strong. So its probably not a big rush to get into the stock. Nevertheless I would add more on a pullback into the mid-$4s. I am hopeful that in the next 18 months, as we see more clarity from the ISED and hopefully some movement on the 24Ghz spectrum, the market will begin to price in some of the upside from these assets.

Excellent write-up. Only thing that needs changed is the first “Terago” should be Straightpath in this sentence…

With its $3.1 billion bid for TeraGo, Verizon paid $0.017/MHz/POP for StraightPaths spectrum assets. A similar valuation for TeraGo’s assets would value the 24GHz spectrum at $100 million and the 38GHz spectrum at $29 million.

Thanks for pointing that out