US Gold (formerly Dataram): Hopefully another Gold Standard Ventures in the Making

In my first few years of investing many of my biggest winners were gold explorers. This was before 2008 and the financial crisis. I spent a good portion of my time analyzing drill holes, reviewing land packages, and reading preliminary economic assessments and resource reports.

In 2005 and 2006 the gold explorers hit on a bull market. The stocks ran up on drill hole hits and speculative sentiment. Miranda Gold, Endeavor Silver, Atna Resources (before they had a mine), Full Metal Minerals, Mirabel Resources, and others that I can’t remember saw doubles and triples. I remember gains of 10-20% a day in some of the names. I’m pretty sure that my first ever “quick triple” was in Miranda Gold, which went from 60c to $2 in the matter of two or three months (going off the top of my head here so don’t hold me to the numbers). It was a fun time.

However junior explorers can try one’s patience. There are long periods where very little will happen and the stocks will drift lower. They are also illiquid and constantly in need of cash. But they can be extremely fun when the sector is in favor or if one hits on a big drill intercept.

I haven’t invested in the sector in a while. Gold has been lackluster and the valuation of explorers has tended to price in multi-million ounces even when the companies had little more than a package of land and an idea. But I’m warming up to the idea. I have a hunch that January 2016 was the bottom for many gold names, and that we are in the early stages (the part where no one believes it yet) of another move higher in gold. If this turns out to be right, the juniors will have their day.

My Gold Standard Memoir

One company that I did particularly well on a few years back was Gold Standard Ventures. In 2010 Gold Standard was formed to explore a package of land claims in Nevada. The claims were very close to and on trend with large existing mines owned by Barrick, Newmont and the like. Gold Standard was pursuing a large, low-grade, sediment hosted, open pit-able deposits like many of the Nevada mines host. What made the company particularly interesting to me was that its VP of Exploration was Dave Mathewson. Mathewson had been head of Exploration for Newmont Mining for a number of years and was responsible for discovering a number of the Nevada deposits that Newmont owned. He had done this before, was well known and extremely well respected, and for some reason he had decided to shack up with a tiny little exploreco to try to find the next elephant.

As it turned out I didn’t own Gold Standard Ventures for very long. The company’s flag ship project was called Railroad. Shortly after listing they began to drill out targets at Railroad, and within the first couple of rounds of drilling the company hit on a number of very exciting intercepts. Numbers like 56.4 metres grading 4.26 grams gold and 164 metres of 3.38 grams gold. This, along with the proximity to the existing monster deposits owned by Barrick and Newmont, and the pedigree of Mathewson, created a bit of a frenzy in the stock. I can’t remember exactly what I bought and sold the stock for, but I believe when I originally bought it the market capitalization was around $50 million (which was not cheap for a gold explorer with little more than a property at the time) and close to $200 million when I sold it. At $200 million I figured the stock was pricing in more than a million ounces already, and so it was best to take the money and run.

Gold Standard 2.0

Flash forward to last month and I was listening to a weekly podcast that I tune into. Its hosted by a newsletter writer who periodically invests in gold exploration stocks. He is describing a new pick that he is very excited about, a gold explorer with massive upside potential. Of course before you get the name you are going to have to subscribe.

But throughout the podcast he gives a few clues. He says he recently traveled to Nevada for an exciting new idea, and while he didn’t link that directly to the gold explorer it wasn’t difficult to deduce the two might be one in the same. He said that the explorer had a very experienced management team who had done this sort of thing before. And he said that the company was flying under the radar because they had recently took over a shell of another company, had yet to change their name, and so very few knew they existed.

It took me about 15 minutes of googling to figure out who he was talking about.

Mathewsen’s latest vehicle for discovering a large, sediment hosted, Carlin style deposit in Nevada is a company that, at the time, was called Dataram. Dataram, somewhat surprisingly, actually seems to have operated a real business pre-Mathewson. They manufacture memory modules. While they are a small company, they did have $30 million of revenue in the last twelve months.

While it seems a little odd that this memory module manufacturer would be used to host Mathewson’s new gold explorer, I don’t know if delving into the details is really relevant to the story. At the time of the reverse merger a clause was included regarding the distribution of net proceeds of the legacy memory business such that only holders of the stock prior to the acquisition date will participate in any proceeds from the sale of the memory business. So when you are buying Dataram today you are only buying the gold assets. And you aren’t actually buying Dataram any more. They changed their name to US Gold, the company they merged with, a couple of weeks ago, ticker symbol USAU.

Project #1: Keystone

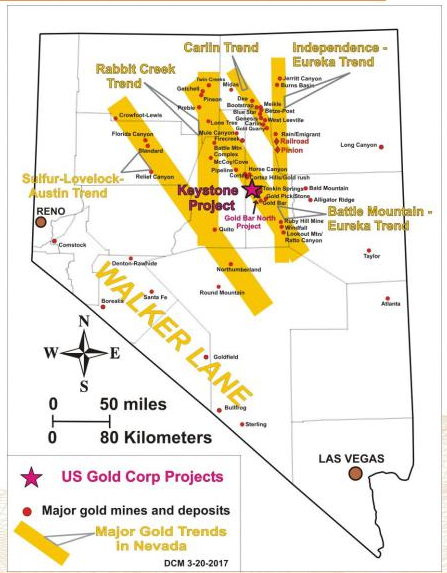

US Gold has two assets. The first, what you would call the flagship asset, is called Keystone. Keystone is very similar to what Mathewson started with at Railroad. Its located in Nevada along one of the major fault trends (called the Cortez Gold trend) about 10 miles south of the Barrick Cortez Hills mine. It is in the middle of a number of elephant deposits, along a major fault and close to other faults. This map of Nevada, from the company’s presentation, shows where Keystone is in relation to other discoveries and mines.

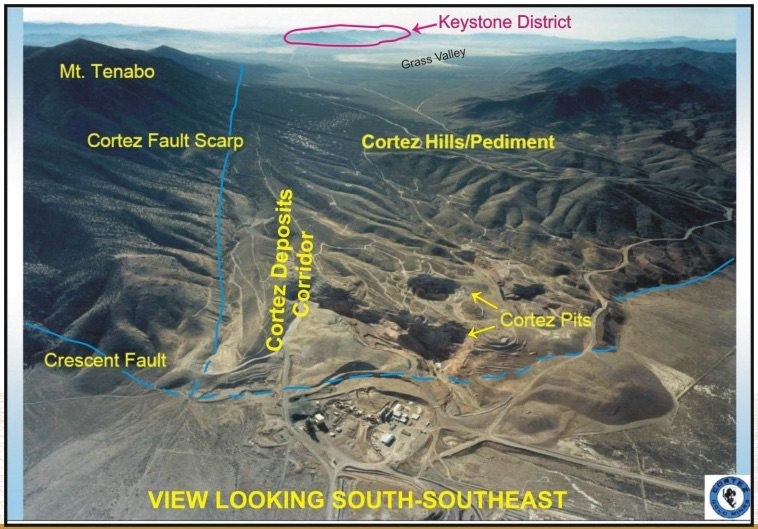

As depicted on the areal view below, you can actually see Keystone from high above the Cortez Hills mine.

US Gold provides background in this 8-K filing. The history of the Keystone is pretty much what you would want to have in a gold exploration target. There has been “no comprehensive, modern-era, model-driven exploration has ever been conducted on the Keystone Project.” What drilling that was done occurred before other Carlin style deposits were discovered and generally targeted formations that aren’t consistent with the large, low-grade, sediment hosted deposits that characterize the elephants in the region. US Gold described it as such in a June press release:

“most of the historical drilling going back to the 1960s appear to have been largely focused on exploring for massive sulfide within skarn and hornfels adjacent to the Walti Springs pluton.

The more recent history of ownership is marred with fits and starts that prevented any serious exploration. In 2004, after the area potential of the Carlin trend was well recognized, the Keystone land package was bought by Nevada Pacific Gold. Given that this was at the height of the last gold exploration boom, one might have expected a big drill program to ensue. But fate and a takeover intervened as Nevada Pacific’s joint venture partner, Placer Dome, was bought out by Barrick. Barrick subsequently did house keeping by dropping all of Placer Dome’s exploration and joint venture projects. Eventually in 2006 the package was bought by McEwan Mining, and 35 holes were drilled before the financial crisis put another hold on exploration.

The consequence is that very little drilling has been done on the project, and what drilling has been done has mostly targeted the wrong formations. After acquiring Keystone in May of 2016, US Gold undertook a review of the historic drill holes, geology, surface geochemistry, and geophysics. In the same June press release I referred to earlier the company said:

Large target areas prospective for potential Carlin-type deposits are beginning to emerge as a result of synthesis from the historical data and the newly obtained detailed gravity survey data and geology.

They concluded that:

A thorough review of all the available data, in addition to some historical holes that included economically significant gold, strongly suggested that Keystone comprised a very large gold-bearing mineral system. US Gold Corp.’s assessment further indicated that this opportunity had potential for high-quality Carlin-type gold deposits. The rock units appeared, now confirmed, to be very much like the same package of stratigraphy and lithologic rock types as is present as host rocks in the Pipeline, Cortez Hills, Goldrush, etc., of the Cortez district within the apparently same northwest-trending Cortez-Keystone structural corridor.

Its expected that they will begin to drill Keystone early in 2018.

Project 2: Copper King

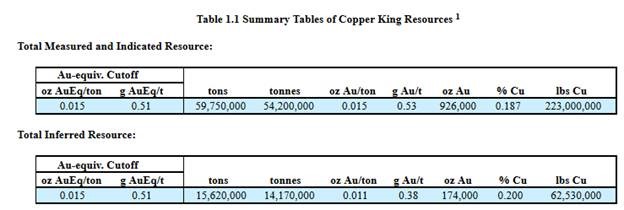

While Keystone has to be considered the focus for US Gold, the company also has a second project that is interesting. The Copper King project – located 32km west of Cheyenne Wyoming, with 5 square kilometers of land claims, is intriguing in that it has had significant drilling in the past and already boasts a measured and indicated resource estimate (from this 8-K filing).

In total there are 1.5 million gold equivalent ounces in the resource. 80% of that resource is sulphide rock, which means that it won’t be amenable to heap leaching and therefore will not be as cheap to process. One thing I have learned in my years of gold exploration speculation is that low-grade sulphide projects are not ideal. Nevertheless in 2012 a preliminary economic assessment was completed on the resource. At $1,100/oz gold and $3/lb copper the project had a net present value of $159.5 million. And it was bought by Mathewson, which counts for something.

I haven’t delved into Copper King but I can tell you already that its true economics is going to greatly depend on those details. Things like: how easily is the ore processed, how much overburden is there, is the shape of the deposit well-fitted to an open pit design, and is there a higher grade oxide zone that can boost the economics by being mined first (20% of the deposit is oxide ore) to name a few. Given Mathewson’s pedigree, I suspect that the answers to many of these questions will be favorable.

Its expected that in the coming months US Gold will review and update the PEA on Copper King, initiate the permitting strategy and further delineate the resource.

Summing it up

US Gold has 8.1 million shares outstanding, but there are also preferred shares outstanding that are convertible into another 4 million shares. At 12 million shares and a $3 stock price the company has a market capitalization of $36 million. They have $7 million in the bank.

The cash should be enough to get them started on Copper King and Keystone, but they will undoubtedly have to raise capital in the next 12 months (all gold juniors are serial capital raisers, it just comes with the territory). I’m not too worried about that though. Given the pedigree of management and the location of the Keystone project, I think they can raise cash without crashing the stock price.

Quite honestly, the $36 million market cap does not seem unreasonable to me. While it was years ago and exact details evade me, I am pretty sure that when I bought into Gold Standard it was with a $50 million market capitalization. And Gold Standard did not have a second property with an M&I resource and PEA assessment valued at more than 3x its market capitalization.

On the other hand, $36 million is not incredibly cheap in an absolute sense of what you want to pay for an early stage exploration company. I am positive you can find scores of gold juniors trading for a few million bucks. But none of those companies boasts the team or location that US Gold has and none of them are going to be able to raise capital with the ease that I am sure this team will. I am inclined to agree with my podcast host that the stock has thus far been overlooked by investors.

Nevertheless the fact is that this is a pure speculation. Keystone may not work out. The probability of failure for the initial drill program even if there is a deposit somewhere under the ground is likely greater than the probability of success. Consider that they are going to punch 20 or 30 4” holes into a 15 square mile land package. Its easy to miss.

In the face of such odds you just have to look for situations where there are as many factors in your favor as possible. US Gold has a lot going for it. It has a management team that is very familiar with the area, Mathewson has already discovered a number of deposits with the exact geology they are prospecting for here in the same area and on the same trend, and they have a land package bearing favorably geology to these other discoveries. You can’t line up your target much better than this. It still might miss, but those would just be the breaks. And if it hits, there is no question it will be a multi-bagger.

Hi Lsigurd, I asked a Q about USAU over on your newest article, but probably should have asked it here.

Is their memory products subsid providing or subtracting cashflow for the USAU parent?

Have had trouble finding financials for USAU, get blank pages on sites. such as https://finance.yahoo.com/quote/USAU/financials?p=USAU

Ah found it on their website:

Revenues year ending Apr. 30, 2017 $ 17,402,000

Apr. 30, 2016 $ 25,182,000

Net cash used in operating activities 1yr ,000s

(218) 2017 (489) 2016

OK so it looks like memory part has $17 mill rev and is a little below breakeven. So you’re mentioned $30 million seems to be for 2015? ending in April?

That seems a big deal if it was making a million a year in cashflow that would be great for overall company. Do you have any opinion of whether memory side can make a profit?

You mentioned you saw it on a stock promotion. I have read other places that even though geologist Mathewson is obviously for real and good, that this is a promoted stock and the other upper management is sleazy stock promoters. Any thoughts on that?

Concept wise this does sound good, and I do have geology background. However sleazy management is something try and avoid.

You recently bot Gran Colombia, which is large position for me. JMHO the most overlooked gold miner there is, could 5 or even 10 bag.

For a company similar to USAU suggest looking at GRG.v. Made a 27 bagger off of Claude Res, and this is same mang team next company after selling to SSRI. have a small position as they are a few years from production, but trust the team and deposit looks good.

Thank you for doing this blog. Like you am thinking the market may be topping, but still some good values out there.

Cheers