Week 314: Trying to Digest the Dollar

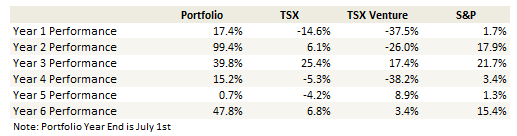

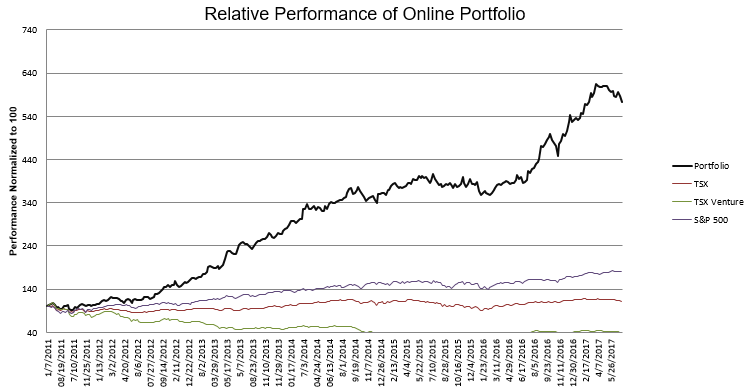

Portfolio Performance

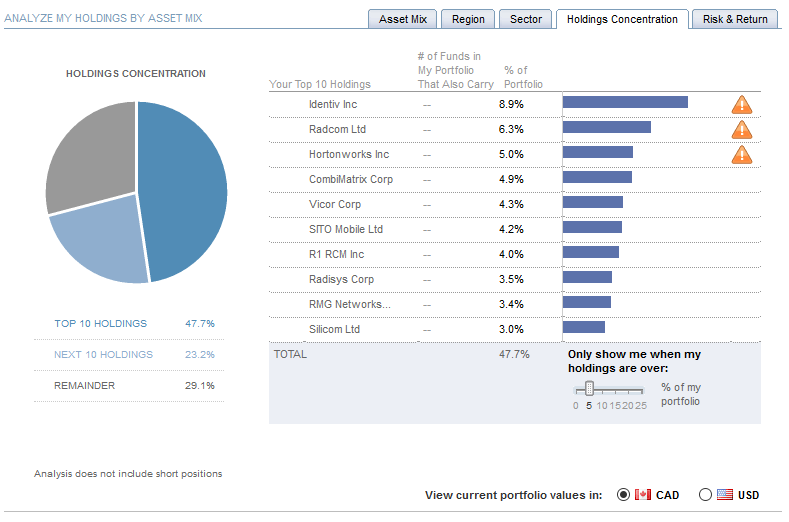

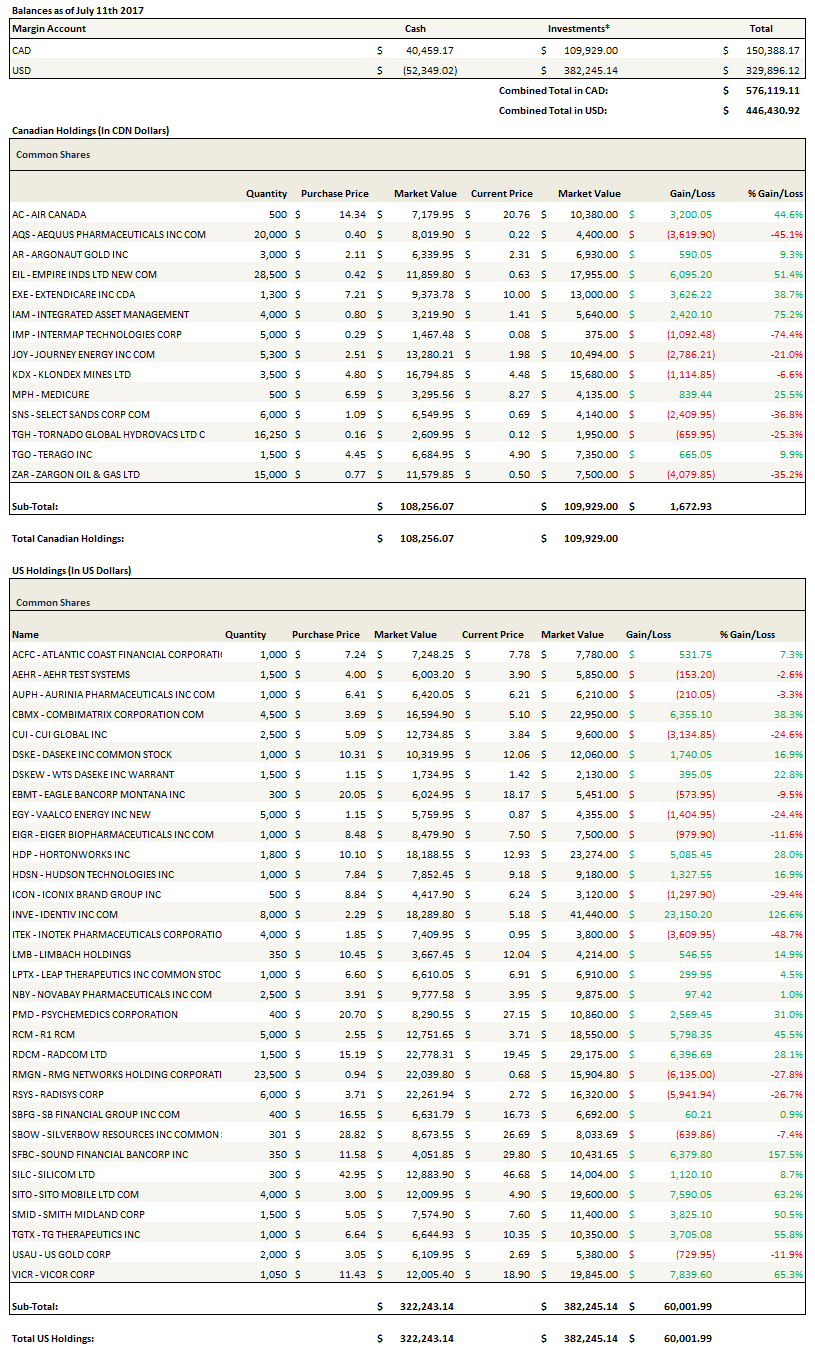

Top 10 Holdings

See the end of the post for my full portfolio breakdown and the last four weeks of trades

Thoughts and Review

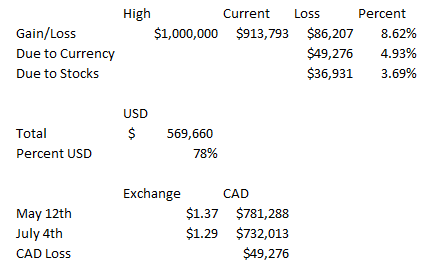

The Canadian dollar has been a massive headwind for my portfolio over the last 2 months. I created a simple little spreadsheet to quantify just how much of a headwind it has been. Below I have recreated that spreadsheet but normalized to a starting amount of $1 million so we are looking at round numbers. Since mid-May the majority of my losses have come from the Canadian dollar.

The performance of my portfolio has been poor since mid-May. Stocking picking hasn’t been great, and I am down 3.7% over that time. This isn’t totally surprising to me. I had a big run in the months after the US election and had wondered when the inevitable pull back would occur. What I didn’t expect was that the pullback would coincide with a huge currency headwind.

The rise in the Canadian dollar has taken place as oil prices have fallen. This has made the move particularly painful. In the past I have been able to offset Canadian dollar gains by trading oil stocks that have tended to rise along with the dollar. Not so this time. Oil stocks have mostly fallen along with oil as the dollar has risen. On Friday the Canadian dollar was up almost a full percent even has oil traded down over $1/bbl.

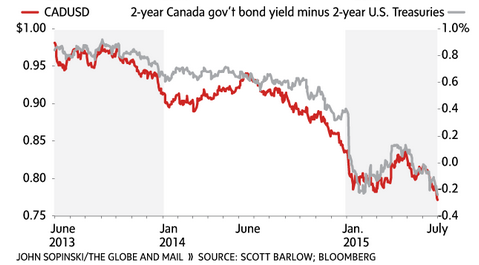

Scott Barlow, who is a writer at the Globe and Mail, had an interesting piece on the Canadian dollar a couple of years ago. In it he pointed out that there was a strong correlation between the Canadian dollar and oil, which is not surprising, but also an even stronger correlation between the Canadian dollar and the yield spread of the US 2-year Treasury and the Canadian Government 2-year note. He presented the chart below.

While the Canadian dollar/oil relationship has went out the window over the last two months, the yield spread relationship has not. Below is a table taken from the Financial Post website that shows Canadian and US Government bond yields. I tried to find a chart to update the one above but could not. Nevertheless, looking at even just the last 4-week data in the table, its clear that Canadian yields have risen substantially while US yields have only risen modestly. The spread has risen from -0.592 to -0.236.

Comparing that to the historical spread chart from the Globe, we can see that a spread of -0.236 is pretty much in line with a Canadian dollar in the 77-78c range. In this context the move in the Canadian dollar is no surprise. The dollar is just moving along with yields.

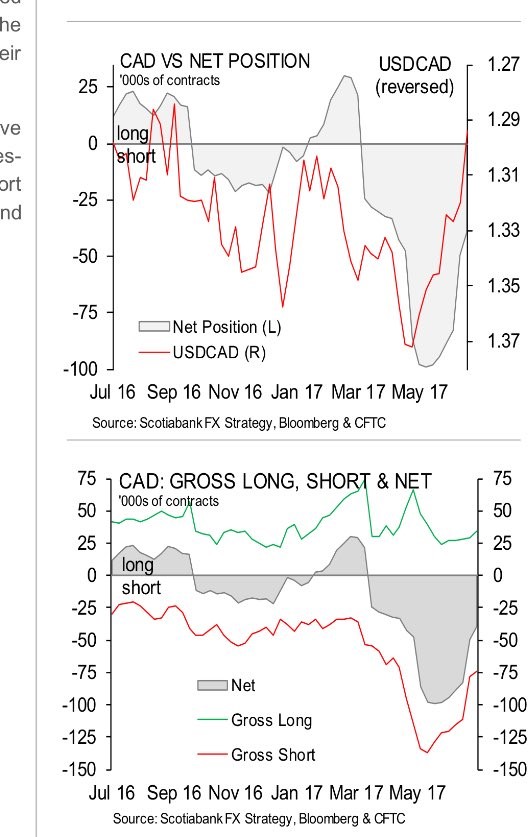

The other factor at play right now are the short positions. I read back in May that Canadian dollar short positions were at an all-time high. It worried me, but I didn’t react to the news, incorrectly assuming that the short covering might send the dollar up a couple cents and I could handle the blow if it occurred.

The shorts have begun to unwind. Below is a chart posted by Frances Horodelski.

We aren’t quite at a level where the Canadian dollar is overbought. The net position remains short. It is still larger than it has been over the past year. But much of the froth has been worked off.

The last consideration is what the Bank of Canada is going to do. The rise in the dollar has coincided with hawkish comments from the Bank of Canada. The market is now 95% convinced there will be a rate hike this week.

So it seems like much of the coming rate hikes has been (painfully) priced in. The rise in the Canadian 2-year yield has been 43 basis points. This pretty much prices out the 50 basis points of rate cuts expected this week and in October.

I would think that for spreads to rise further there would have to be evidence that the Canadian economy is actually stronger than the US economy. While the Canadian economy is showing strength at the moment, so is the US. The jobs numbers in Canada were strong (though a lot of it was part time work) but so was the jobs number in the US. Historically, the only times that the Canadian economy has outperformed the US economy were during times of commodity price strength. This isn’t one of those times.

Meanwhile so much of the Canadian economy is being driven by housing right now. I know many will disagree with this, and I know I have been wrong about this for some time, but I still do not think this is healthy and I do not think this is going to end well. I read over the weekend that transaction costs on housing make up 2% of Canadian GDP. That seems incredible to me. It is but one example of how important housing, and buoyant housing prices, have become to the Canadian economy.

There was an interesting BNN interview last week with John Pasalis, president at Realosophy Realty. Pasalis said that over the last couple of months the “Toronto housing market turned on a dime”. June home sales were down 37% year over year and prices declined 14% from the April peak.

I am sure that the response of the housing bulls is that this is just another buying opportunity, and they will point to Vancouver, which quickly recovered from its dip last year. Maybe so. But what is going on in housing has every earmark of a bubble. When I read about the foreign ownership, about the domestic speculation, and about prices exceeding traditional metrics of income as debt piles up, it sounds so familiar to other speculative bubbles I’ve read about. I’ve read Extraordinary Popular Delusions and The Madness of Crowds multiple times, as have I read Manias, Panics and Crashes multiple times. All of the lessons I tried to learn in those book rhyme with what I read about Canadian housing.

I have no idea when Canadian housing plays out in the way I expect it to. But being short the currency of such a bubble does not make me lose sleep at night.

Could I lose more because of the Canadian dollar? Most definitely. I can see a path to 80 cents. There are more shorts that need to be unwound. If the Bank of Canada raises rates and strikes a hawkish tone this week, the market will likely push the dollar up.

But I am not going to try to trade this for a couple of cents. My belief is that the only thing that is going to move the Canadian dollar sustainably higher is higher commodity prices. If we get those, then the stocks I own should more than compensate me for any rise. Unless that happens I will take the lumps that I am getting from this move, try to focus on maximizing the performance of the stocks I own, and not focus on what the short-term movements of the dollar are doing to my portfolio.

Portfolio Changes

I’m going to be brief with my transactions this last month and a half.

Radisys has been a disaster and I have reduced my position some in my actual portfolio but I have not in the portfolio tracked here. As usual I was a bit slow to the trigger with the online portfolio and by the time I got around to it the stock had sunk to a level that I believe is too low, even given the reduced guidance and lowered debt covenants.

What led me to reduce my position were the changes to the credit agreement amendment that they filed. There was a change to EBITDA, which was consistent with the change in guidance and therefore not unexpected. But there was also a change to the expected restructuring charges in the second and third quarter. Total TTM restructuring costs are expected to be $9.5 million by the end of the third quarter. This compares to $1 million in the previous amendment. I’m a little worried what precipitated this and until the earnings call, its impossible to know. If this is restructuring of the legacy business, then no problem. If its something to do Software Systems or DCEngine, that would be bad. And until we get to earnings, we won’t know.

With that said, the credit agreement also implies decent revenue in the third or fourth quarter. Below I have recreated what their minimum EBITDA covenants, which were just amended in the new agreement and therefore presumably at levels that management is comfortable with, imply about the third and fourth quarter.

They are still predicting a revenue ramp, albeit not as significant as they had been suggesting previously.

At $2.75 the stock is kind of in no man’s land. It seems too low to me to sell (its essentially back to the level it was at before they even had Verizon as a customer). However I find it impossible to be a buyer until there is some clarity around the restructuring and what constitutes the delays.

The other portfolio change that I will mentions is that I added a few gold stocks, Klondex Mines, Argonaut Gold and US Gold (which I already wrote about here). I like how beaten up the junior miners are, and I will write something up shortly describing how changes to the GDXJ have impacted these stocks. Apart from that early in the month I sold out of a number of names which in retrospect, for the most part at least, turned out to be a mistake (GIMO, ATTU, SUPN, SIEN, BVX and OCLR) as many of these names are higher now. I would have been better off selling Radisys!

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

What do you think about Radisys? Do you think this is a buying oppurtunity based on the low stock price while the management expect the revenue is coming in later quarters?

I’m done with it. I blew it, made a bad call. I could easily have dumped the rest at the bottom but at this point I’m so disgusted I don’t care. I dumped RDCM too.

You may like Wireless telecom, lot’s of operating leverage in that one. And will get a lift from 5g cycle.

Ok, thanks. I will take a look at it.