Waiting on my position in Bearing Lithium

I took a position in Bearing Lithium a little over a month ago. It was one of a number of positions I took when I realized the significance and inevitability of the electric vehicle. But since then it hasn’t done much. It has probably been the worst performer of the bunch.

When I compare the performance of Bearing to other lithium stocks that have risen significantly I am disappointed. Nevertheless the stock is cheap and I think over time the valuation discount will be closed. So I plan to wait on it a while longer. Here is the story.

Maricunga Deposit

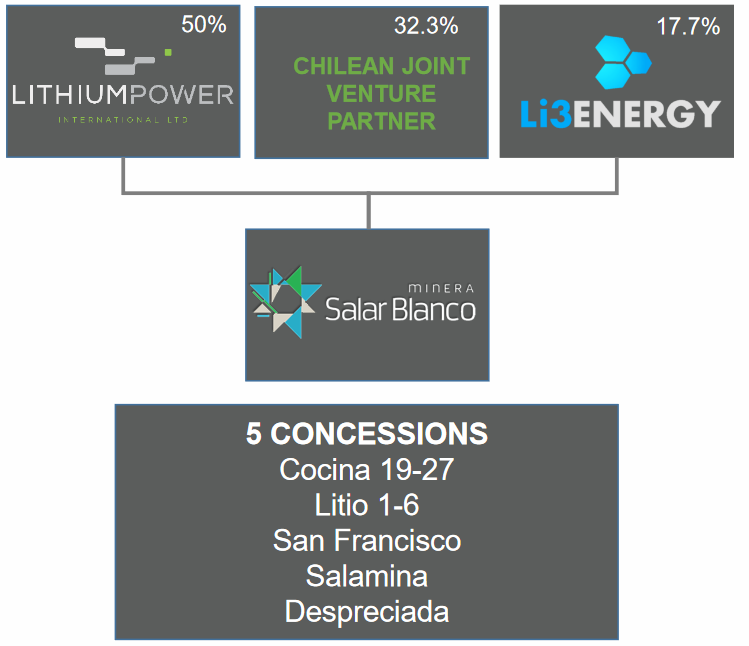

Bearing owns a 17.7% interest in a lithium brine deposit in Chile called Maricunga. Maricunga is one of the highest grade deposits in the world with a measured and indicated (M&I) resource of 1,143mg/L. The Ni 43-101 report outlines a deposit contains 1,720,000 tonnes of lithium carbonate equivalent (LCE) M&I resource.

The deposit is co-owned by Lithium Power, Bearing Lithium and a Chilean JV Partner. Lithium Power has an earn-in to 50% ownership by advancing the project to feasibility. Because of the earn-in Bearing has their costs covered until roughly mid-2018 when a feasibility study is produced.

Here is the Australian firm Independent Investment Research, who covers Lithium Power, giving their thoughts on Maricunga (note that this was before the recent resource estimate that more than doubled the size of Maricunga):

Bearing Lithium acquired its stake in the project via a merger with a US OTC company called Li3. Li3 had a 49% stake in the project until July 2016 when they entered into the agreement with Lithium Power and the Chilean JV Partner to create a JV to hold the assets.

As part of the JV agreement Li3 had their stake reduced (to the current 17%). In return Lithium Power agreed to contribute $27.5 million in cash to the Maricunga JV to cover exploration and development until feasibility.

Being an OTC junior strapped for cash, Li3 took the deal.

Still being short of cash and stuck in relative obscurity as a penny stock on the OTC, Li3 agreed to be merged with Bearing in January of this year. The merger wasn’t met with universal glee by all shareholders. As a number of posts on the investorhub board suggest, some shareholders questioned why they were diluting their stake in Maricunga.

It’s a good question. I am guessing that it came down to a lack of options for raising capital, and the hope that a listing on the TSX Venture would lead to promotion and a re-rating of the deposit.

Unfortunately that hasn’t happened so far.

Peer Comparison

I would argue that Bearing Lithium is undervalued. Below is a comparison with a number of other lithium explorers, some with a defined deposit and some without. Even companies with no firm resource hold much higher valuations than Bearing.

Why the discount to peers? There are reasons, but I don’t think any of them justifies the discount.

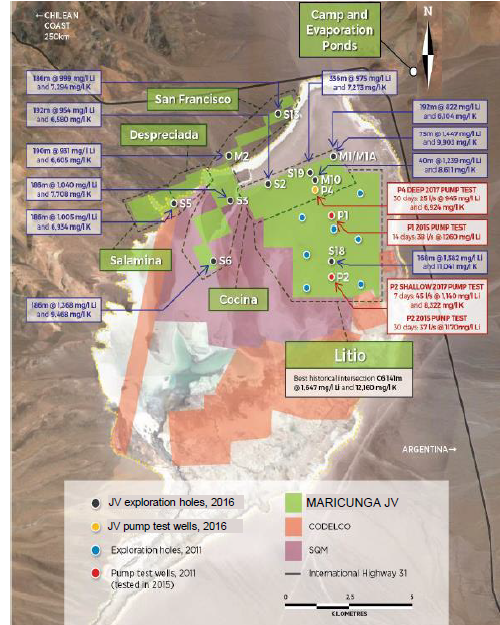

First, the majority of the lithium resource exists in the Litio 1-6 concessions (I provide a map that outlines the concessions below). These concessions do not have a mining permit yet and are not grandfathered like Cocina 19-27 concessions. In their current state they can be explored, but not mined. There may be some concern about getting a permit.

Mitigating this concern are comments from the mining minister in Chile, who came out and was in favor of maricunga (according to this interview):

If I was to choose anywhere in Latin America, one, two and three, it would be Chile, Chile, Chile. But saying this, moving forward, Aurora Williams, who is the mining minister of Chile, announced at PDAC only last week that Chile’s main goal is to find foreign capital to develop the Maricunga.

While permitting, at least with the current government, will require negotiations, when it comes time to go to the table I don’t expect that Bearing Lithium and Lithium Power will be the one’s to take the deposit to production. I think Maricunga gets picked up by a bigger player. The map below shows how the concessions are surrounded by neighbouring concessions owned by Codelco and SQM.

Consolidation into a single large operation makes sense. When that occurs, I suspect that the larger company will be able to negotiate permits for the entire district.

The second reason for the discount might be that Maricunga is in Chile. Chile has a far more left leaning government than Argentina. The government has feuded with SQM over the company’s leases in Chile. They have been renegotiating terms of Albemarle’s royalties where they have asked for a 60% royalty if lithium prices rise over $12,000/t USD.

There is an election in Chile in November so a change of government is possible. Early polls suggest a change in government might occur.

The third reason is ownership structure. The ownership was a problem before the merger because Li3 was listed on the OTC, was a penny stock (like literally a 1c stock!) and thus it received zero exposure. It’s a bit better now that Bearing holds that stake, but I wonder how many investors are dissuaded by the relatively small minority interest Bearing has.

It doesn’t help that Lithium Power trades on the ASX. I don’t think there are many lithium-brine plays on the Australian exchange. Australia is all about hard rock lithium mining. I don’t know of another that is primarily a brine-only play (please tell me if I’m wrong?). Lithium Power is a bit of a fish out of water.

As well, Lithium Power has a huge warrant overhang of 72 million shares at 55c. Because Bearing Lithium and Lithium Power trade to a similar valuation, the ceiling on Lithium Power impacts Bearing as well.

The fourth reason is promotion. Whether or not you think all these tiny little lithium explorers are going to turn out golden in the end, you have to admit that their stock movements lately have had more to do with speculation than anything fundamental to the individual names. So far there isn’t a lot of promotion around Bearing and the Maricunga deposit. For example, if you go through the Seeking Alpha articles on lithium you will find all kinds of tiny juniors referenced, some with only some hectres of land and no resource, but there has been nothing written about any of the Maricunga players.

So there are some reasons. None of them are particularly compelling to me. None make me want to sell my position.

Conclusion

Its been a disappointing investment so far. I’ve watched a couple of other tiny positions I have in lithium juniors (International Lithium and Nemaska Lithium) give me more profits than my larger position in Bearing (I’m down on my position in Bearing so far).

Nevertheless I am going to stay the course. The Maricunga deposit is world class, its higher grade than almost all its peers, its relatively advanced and has not shown any features that would handicap it. I think eventually the superiority of the deposit will win out and I’ll hold on for that to happen

Sounds promising…

Do you still own US-Gold (USAU)? They have issued new shares and I am massively down.

I sold out of that one a while ago. They didnt hit anything on their announced drilling and like you said the stock started dropping.

Thanks. I hope you don’t mind me asking about certain positions.

Because I do respect your opinion.