CUI Global – what to do now?

CUI Global is a total gong-show.

When I bought stock a couple months ago I thought I was buying a lottery ticket on news that the Snam Rete tariff issue would be resolved and there would be a nice pop in the share price.

I was wrong.

I wouldn’t have thought it possible but the company managed to announce the news I had been waiting for and implode the share price in the process.

For the love of…

They pulled off this feat by announcing an a extremely large share offering at the same time. The company is offering $15 million worth of stock. There is no pricing on the stock, but if they wait a few more days maybe it will be a 99c special <rolls eyes and shakes head>.

In all seriousness, I’m underwater, the news I was waiting for is out, and the stock didn’t do what I thought it would do. So what do I do now?

I have to admit my temptation was to sell. Especially given that this event does not shine a positive light on management. I don’t know if the selling is related to the offering (Craig Hallum often seems to be associated with these sort of crazy stock moves coinciding with a placement that they facilitate) or if its just a pissed off institutional holder that wants out, but at the end of the day its on management for making a decision that led to a full collapse in the price of the stock (it was a $4 stock like 5 days ago!).

Anyways I decided to stick it out. I also added to my position yesterday and today. Here’s why.

GasPT Opportunities

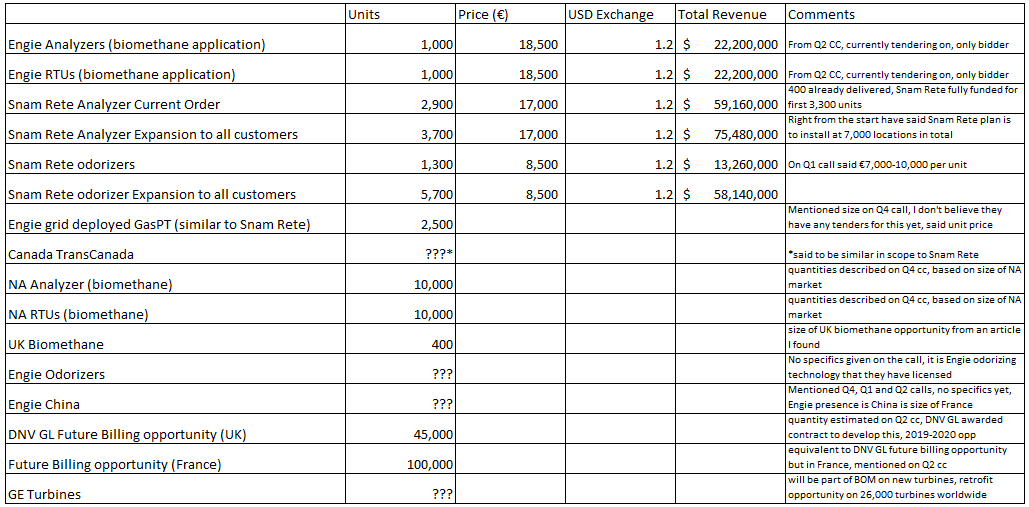

First the opportunity presented by GasPT is legitimate. And the opportunities on the radar are extensive. The following table outlines what CUI Global has talked about on conference calls and during presentations at investment conferences that I have listened to:

Potential Near-term Revenue from these Opportunities

Of these opportunities, the one’s that are most likely to be near term, or accretive to 2018 or 2019 numbers, are:

- Snam Rete analyzer current order

- Engie biomethane skids (analyzer and RTU)

- Snam Rete first stage of odorizer order

The quarterly revenue from these 3 products are in the table below. I made assumptions about monthly units based on managements (admittedly vague) comments about delivery time frames on conference calls for each project.

Of these projects, we now know that the Snam Rete analyzers will start being delivered in “early 2018”. My quote is from news that was supposed to move the stock up but didn’t.

Energy and GasPT Gross Margins

I needed to get a better handle on GasPT gross margins. Energy gross margins have fluctuated over time depending on how much engineering work CUI is doing and how much product (ie. analyzers) they are selling. Product revenues have higher margins so more GasPT sales are going to raise energy margins as a whole.

There have been enough quarters where energy revenue has been all engineering work to know that this work has margins of about 35%. Based on known Snam Rete shipments over the first 3 quarters of 2016 I backed out what gross margins are (at least roughly) for GasPT analyzers. It turns out to be 59%. I came up with this by comparing the quarters where CUI Global saw Snam Rete revenue and the quarters where they didn’t in the table below:

Earnings

Once I had an idea of GasPT margins and volumes, coming up with how this plays out into earnings is pretty straight forward. I made the following assumptions:

- CUI has over $100 million of NOLs so they won’t be paying taxes for a long time

- G&A is expected to decline $1.5 million annualized after a small restructuring in the first half of 2017

- The power business is doing well. I’m projecting 5% growth for the Power segment over the next year compared to TTM numbers

- I assume the Energy (ex GasPT) and Power segments to operate at 35% margins, which should be conservative against historical comps. The company guided to 40% Power margins in the second quarter.

I looked at two scenarios. The one that I illustrate in the table below assumes GasPT revenue is only from the Snam Rete analyzer order. This is 300 units per quarter or 1,200 units per year.

The numbers are annualized. I’m doing my per share calculation before the offering, so I am using the 20.9 million shares outstanding right now. And the trailing twelve months (TTM) are ending with the second quarter.

Conclusion

In my opinion, my biggest risk is that I don’t understand why the company is issuing stock. It doesn’t make sense. Its possible that when the reason comes out I will get to do another face plant.

At the very least we know there is going to be dilution. Its going to be significant (maybe 30% if the placement is done around the current price?). However there is also going to be a lot of cash on the balance sheet and the company will be debt free.

Its hard for me to ignore the earnings potential. The numbers I ran through in the scenario above only assume the Snam Rete order. When I looked at a second scenario that assumes all 4 of the potential near term opportunities come to fruition, I get earnings of $1 per share pre-dilution.

There is also the future billing project from the UK to consider. The company announced last week that the project was progressing into a second stage. While revenue is still a couple years off the number of potential GasPT units for this project (45,000) are staggering. I didn’t bother to work out a scenario for this one because the number would just sound stupid.

So there you go. I doubled down my bet. Sometimes that works and sometimes it blows up in my face. I put the work in to justify my decision, at least to my own satisfaction. We will see where the chips fall.

Thanks for this much needed update. I agree that now is the absolute worst time to sell. Unfortunately as far as I understood, the UK project is far away ( 2019?).

I have mentioned in another comment CleanTeQ (CTEQF). I have done some more digging. Positives are insider ownership(Friedland and a Chinese company with which they have an agreement to deliver their metals when the mine is set up) and massive potential for Scandium, Cobalt and Nickel. Huge potential. Here’s the ugly: They will need about their market cap in Capex (900M or something). So they will probably massively dilute.

I will watch from the sidelines and have a close eye on the development.