Week 332: More Churn

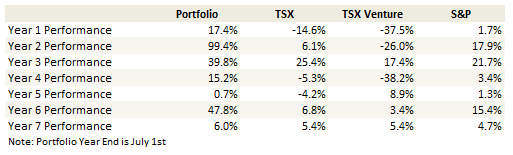

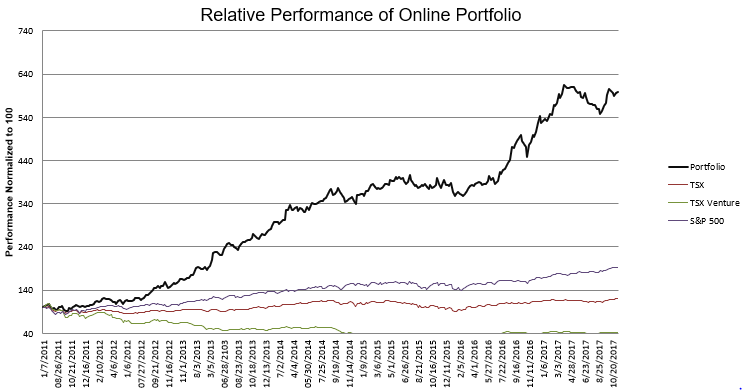

Portfolio Performance

See the end of the post for my full portfolio breakdown and the last four weeks of trades

Thoughts and Review

So I’ve been doing so-so with the portfolio. I had a big bump up in September because of Helios and Matheson, and since then have mostly been treading water, a few winners and a few losers.

My online portfolio has actually done somewhat better than my actual one. This is primarily because A. By chance I held on to a larger piece of Helios and Matheson into the high $20’s and B. I’m fully exposed to the Canadian dollar fluctuations in the online portfolio and the Canadian dollar has fallen back below 80c of late.

I’ve still failed to outperform the market for the last 6 months, and that’s been frustrating. My outperformance in the near term is going to depend a lot on Overstock, which is my largest position right now.

I added around my oil positions as it seems more likely then not we will continue to see draws through year end. I find the Canadian service companies particularly interesting, mainly because they really look cheap based even on backward looking metrics but stand to benefit further from the price and volume increases one would expect are coming. I have mentioned Cathedral Energy before, and also like Essential Energy (with the recent positive decision on the outstanding lawsuit) and Aveda Transportation, which is quite levered and has a business tied closely to drilling.

I sold out of Klondex. I had reduced my position earlier and sold the rest after a pretty so-so quarter. On the other hand I increased my position in Gran Colombia, which is a frustrating stock for me because it raised guidance and continues to show good cash flow but has these towering asks day after day that keep the stock down. Gold has been crummy through December in the past but I am pretty excited about gold in 2018. I want to keep more than my usual weighting going into the new year.

I was pretty happy with the mining results of Ascendent Resources, Largo Resources and Lynas, though none have really done much since their reports. I plan to write something up on Largo in the near future. Vanadium seems to be catching some attention and Largo is the only way to play that. Largo had a really good day on Friday, but its volatile so I don’t know if there will be follow-through. Vanadium prices are firming up though. There was a good overview of Vanadium in this blog. I plan to write up my thoughts on Largo soon.

I was disappointed in Sherritt’s results and sold down my position for now. Similarly I didn’t like what I saw with CUI Global, particularly that the odorizer technology is not ready for prime-time. So I sold that one too. Smith-Midlands was disappointing and who knows when an infrastructure bill gets passed, so I’m out of that stock. I sold Lakeland Industries, though I might buy that one back in the short term. I sold the rest of Identiv, a bunch ahead of earnings and the rest after their dismal report. I sold Daseke ahead of earnings, which turned out to be fortuitous. And I bought and sold a company called Xunlei Limited, which I quite honestly lucked into when searching for blockchain companies. I really can’t wrap my head around what they do, so I didn’t stick around after some gains there.

So there’s more churn for sure. I’m going to try to be quicker to the sell button going forward. I think that I have been slow to sell for logistical reasons, and this has been a contributor to my poor performance over the last few months.

I’ve taken a few other small, new positions but nothing with enough conviction that I want to talk about them yet.

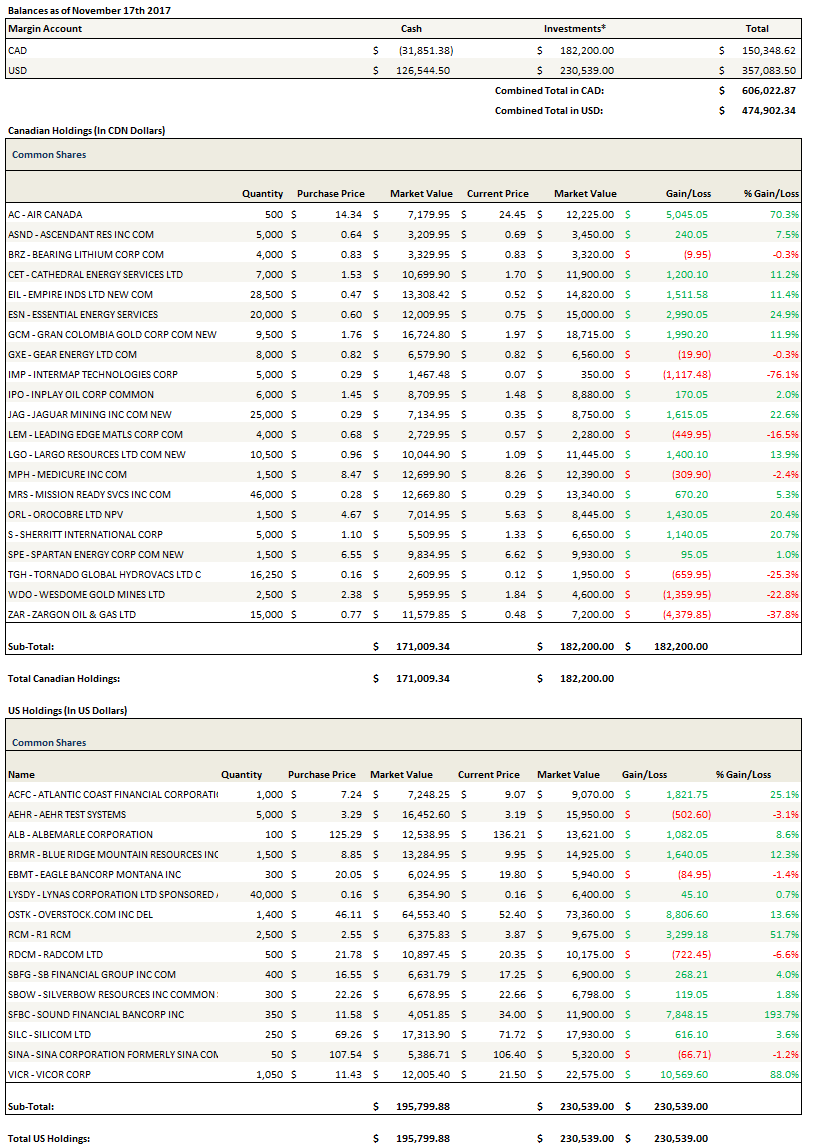

In fact that’s about all I want to say about the portfolio right now. Here is my portfolio as of Friday.

Portfolio Composition

Click here for the last eight weeks of trades

{kind=link}

Hi

Thanks for all the analysis you do. Curious what gives you so much conviction in OSTK to make the position so large. Are you sizing based on limited downside / tremendous possible upside?

Hi

Thanks for all the analysis you do. Curious what gives you so much conviction in OSTK to make the position so large. Are you sizing based on limited downside / tremendous possible upside?

I think matching the market when the market is maybe going against your style (which, to be sure, shifts) is pretty good.

Separately, have you ever looked at QTRH (the former WILN)? A very lumpy patent troll which took its large cash stash and paid a full price for a high-quality, small, profitable “smart road” company (IRD) and a small industrial software biz I don’t yet know much about.

They are an odd creation, hard to value, and I’m still trying to work out the range of possible values. But it seems they may be a quality company trading for less than they’re worth.

I have a new Cobalt/Nickel/Scandium play for you:

Australian Mines Limited ASX: AUZ

They have just done a financing round at the current price and seem to be cheap right now especially compared to pears like CleanTeq. According to my estimates they would be worth much more even at current commodity prices just if they get their projects in production.

Also they don’t rely on Lithium prices, which I am a bit careful about after reading this article:

https://seekingalpha.com/article/4110963-lithium-big-short

Thanks I’ll check it out.

Okay, I have gone now from A to Z for all cobalt names I could find.

I am thinking about a kind of basket approach as I have now at least 10 companies on the radar, which look all promising to me. Meaning recent financing, high exposure to especially cobalt (and nickel).

I have to do more work here, because I think the sector is currently coming.

One thing I noticed is that almost all of these stocks have started to climb after doing nothing for a year or more.

I would also appreciate your opinion on Northern Oil & Gas Inc.

http://ir.northernoil.com/stockquote.cfm

Despite recovering oil prices they have declined from 4 to 1$ per share in the last year.

Their production is strong and the well seem to be getting better and most importanltly they have recently don some refinancing so their debt is due 2020 and beyond.

MRS released some nice news relating to a shipment. What would be your price target on that one? Assuming it could appreciate in value with more orders, but perhaps today 60 cents is fair?

Also, OTSK is very interesting. Looking forward to the 18th to see how the ICO goes. OSTK is one of my main holdings after first hearing about it from you. I feel like there is a solid margin of safety built in with retail business and lots of optionality in the blockchain side. Additionally, I appreciate the quantitative factors such as low ev/ebit as well as excellent 6mo price momentum. What would be your fair valye for OSTK today? 90?

Respectfully,

Mitch