HIVE Blockchain as a crypto-mining bet

When I started looking at the crypto-miners a month or so ago, I was pretty skeptical. I thought there was a good chance that the business was a promotion to make it sound like you were a blockchain company when really you weren’t. The company’s were all shells that had flipped the switch to blockchain overnight. It was hard to take it too seriously.

But since then I have come around.

What made me change my mind was profitability. This post, which is from an excellent crypto-blog, does a great job of describing the opportunity. If you want raw data, check out this calculator and these GPU hardware stats. A single RX 480 card has a hash rate of 28 MH/s and takes 160W of power. Using the calculator, 28 MH/s and 160 W of power at $0.10 per kWh gives you a profit of $31.26 per month from mining 0.143 Ethereum. On Ebay you can buy a 7 GPU mining rig for $3,214. 7 GPUs should pull in $2,600 worth of Ethereum per year at $450 Ethereum. It’s a pretty solid return and I haven’t even shopped around, tried to buy wholesale like a scaled player or moved my operation to a low cost power district.

You can run through a similar exercise with bitcoin. You can buy the equipment at retail and still come away with a pretty solid return on investment. If you start shopping wholesale, or assembling the rigs at scale, I imagine the payback is over 100%.

With that said I’m not getting into the crypto mining business. I have a feeling the devil is in the details, and there is a lot more to it than just buying the equipment and plugging it in.

But you get the point. The above analysis gave me a reason to look more closely at the miners and what they are trading at.

Stepping my toes into the water, at the beginning of last week I bought a little Riot Blockchain. I had lucky timing as the stock almost immediately started running. I bought Riot because on an equipment basis, when I compared it to HIVE Blockchain, it seemed quite a bit cheaper. But I was never really sold on the story, mainly because Riot hasn’t really given many details about their operation and we don’t even know if they are mining yet. As such I sold out way too early. I began selling at $11 while the stock got as high as $22 on Friday.

Thus my Riot Blockchain experience is likely finished. But it led me back to HIVE, which looks more interesting as I have dug deeper. I took a position in HIVE on Friday at about $2.80 (Canadian), for the reasons I will explain below:

HIVE Blockchain

HIVE started out as a reverse merger of a gold company called Leeto Gold (yes a reverse merger; you can pull out the red flags, I’m not going to deny they aren’t there). They got into the crypto-mining business when they acquired two data centers in Iceland from a very large private mining firm called Genesis Mining, the first in September and the second in October. I first looked at the stock after the purchase of the second data center. I struggled to wrap my head around the business, and the disclosure was (and still is) lacking. So I passed.

I watched the stock shoot all the way up to $6 (Canadian). But then it came crashing back down. With Ethereum prices 40% higher and with HIVE securing a third much larger data center to be built in Sweden (in two phases) I decided to look again.

The short report

Ironically it was a short report that cemented my interest in the stock. I don’t know who wrote this or where it came from. Someone posted a link to it on Stockhouse last week. Reading it made me reconsider my thoughts on HIVE.

The report does a really good job of weaving together the sparse disclosures from HIVE and gauging the size of their mining operation. It was very helpful to see how you can build a model (a rough one but a model nevertheless) from the somewhat detailed disclosures HIVE gave on the first Iceland data center and the subsequent minimal disclosures of how much each additional data center would increase hash capacity.

Of course the report, being a short report, concludes that HIVE is way overvalued. But I’m pretty sure this is because of one little mistake.

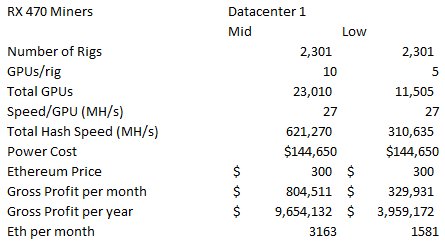

If you read the report, you will note that it references 2,301 GPU cards in the first data center. Because of the lack of disclosure from HIVE, all of the other data center calculations are factors of the known size of the first one. As the report explains, if there is only 2,301 GPUs in the first data center then HIVE isn’t going to make much money, either on the first data center or any of the subsequent one’s.

But here’s the thing. When I read the report I had done enough research to know that 2,301 GPUs is not very many for a data center. Moreover, it seemed like there was no way anyone would pay $9 million USD and 67 million shares for that many GPUs. You’d have to be crazy.

Luckily I have a subscription to Sentieo, including their Canadian data, and that makes it really easy to search for something like “2,301” and find out the context. As it turns out, the document is hidden in the obscurity of the annual report of the reverse merger parent Leeta Gold Corp. And it doesn’t actually say GPUs. Here is the relevant paragraph (my underline):

The HIVE Facility consists of 2,301 graphic processing unit (‘GPU”) mining rigs. Maintenance costs, including electrical power, to be paid to Genesis, for operation of the HIVE Facility are expected to be around US$144,650 per month. The maintenance costs will be part of the Master Services Agreement

Its 2,301 rigs. This makes much more sense and changes the calculations significantly. Its pretty easy to google “gpus per rig”. If you do you find that most rigs have at least 5 GPUs. Many rigs have more than 10 GPUs.

Thus, when I looked at the short report conclusion and saw that they projected $750,000 per month in revenue, I was like, wow, its actually more like 10x that much. And that’s at $300 Ethereum!

Time to buy.

Conflicting Disclosures

If the short report is off by a factor of 10x then HIVE is a no brainer. To get a levered play on the direction of cryptocurrencies at a cheap price is a steal. Unfortunately as I have done more work to make sure the details align, things have become a bit muddled again.

To reiterate what I said earlier, the tricky thing about evaluating HIVE is that:

- There isn’t a lot of information about each of the data centers. In fact every subsequent data center has to be based off of the known information about the first data center

- The company has provided two fairly different estimates of the profitability of the first data center

So what do we know about the first data center? Well, we know there is 2,301 rigs. But we don’t really know how many GPU’s each rig has (though I’m pretty sure its more than one).

The other information we sort of know is the profitability of the first data center. Unfortunately, I say sort of because HIVE has given us two numbers for this and they aren’t that close to one another.

On June 14th, in this press release, HIVE said the following (my underline):

Based on the computational capacity of the first Data Centre, the historical prices, and required hash rates, and using a mine and immediately sell strategy, the trailing 12 month EBITDA would have been approximately US$7 million.

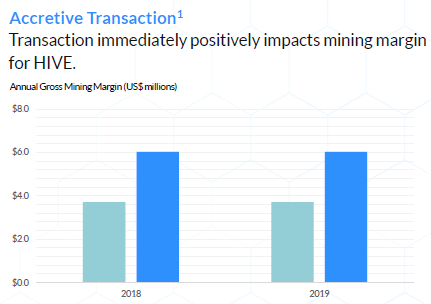

Later, in their October presentation, HIVE provided this chart on slide 18 (light blue represents the first data center only and dark blue represents two data centers in Iceland).

There is a big difference between $4 million of “gross mining margin” and $7 million of EBITDA. Because the $4 million number is more recent, I’m going to assume it’s the correct one.

I wanted to try to get to the number independently. With the disclosure of 2,301 rigs and a reasonable assumption of GPUs per rig its pretty straightforward to use a cryptomining calculator to come up with gross profit, which is likely the equivalent to what HIVE describes as their “gross mining margin”.

But how many GPUs per rig? I would have expected at least 10. From what I’ve read, a big miner like Genesis should have at least 10 GPUs per rig. You’d think Genesis would be using the most efficient GPUs in their stack.

The problem is that the numbers don’t work out with 10 GPUs. I’ve tabled two scenarios, one with 10 GPUs per rig and the other with only 5. I actually also had a third scenario with 15 GPUs per rig (the “high” scenario), but given the results that one seems unlikely so I didn’t include it in the table.

Surprisingly, it’s the 5 GPUs per rig scenario that matches a data center generating $4 million of margin at a $300 Ethereum price.

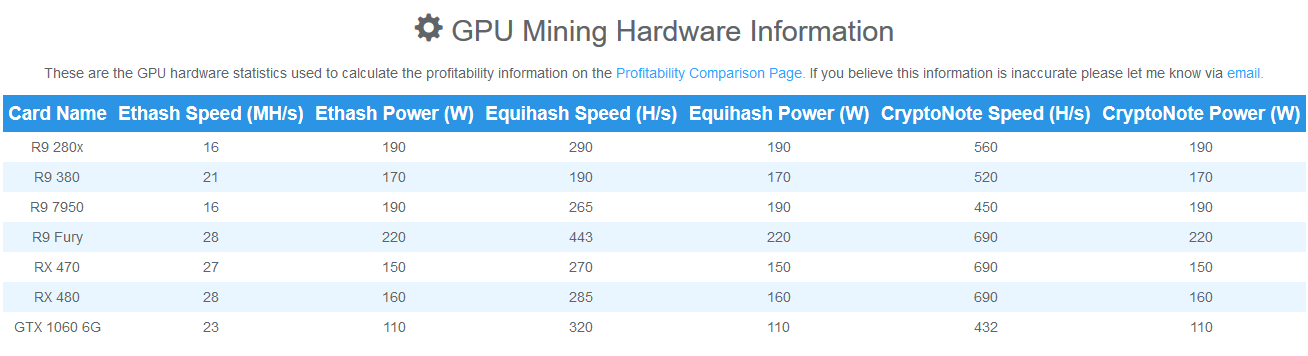

One other possibility is that there are indeed 10 GPUs, but they are lower end processors. My assumption above was based on the RX 470 card, which has processing speed of 27 MH/s. I’m told this is one of the most efficient cards. But maybe the Iceland data centers use R9 280s, which would have a little more than half the processing power as the RX 470s (see the table below). That would get us closer to 10 GPUs per rig while still staying within the $4 million gross mining margin range.

Of course the other wildcard is that if the earlier $7 million EBITDA number is correct, then my mid case is likely closer to the truth. But like I said, given the dearth of information I am forced to believe the later number is more accurate.

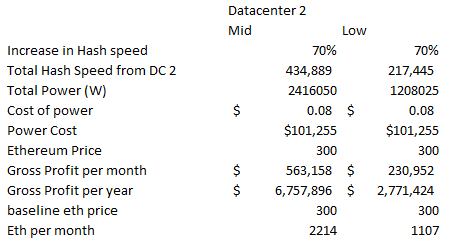

Once you get the first data center pegged, its easy to figure out the contribution of subsequent data centers from the increases in hash power that HIVE has disclosed for each.

The second data center is said to “increase hashpower by 70%”. From this information, and assuming a similar power consumption agreement as the first data center, its easy to calculate its contribution. Keep in mind that it’s the “low” number in the table below that is the one I’m assuming is most accurate.

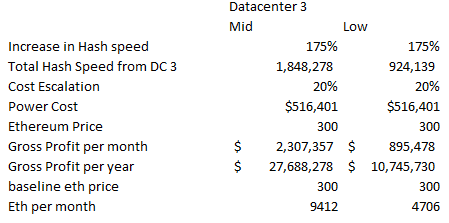

The third data center (in Sweden) was said to increase hash power by 175%. Note that I also added a 20% cost escalation for power and maintenance costs on top of what HIVE is paying for the Iceland assets.

For the fourth data center, the company said the following about its Swedish operations on November 14th:

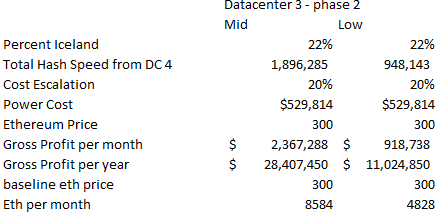

The Sweden Data Centre will consist of newly constructed GPU mining rigs using the latest hardware, custom-designed by Genesis. Each phase is expected to represent approximately 6.8 MW of electricity consumption for a total of 13.6 MW in Sweden. HIVE and Genesis are evaluating expansion potential in Sweden as well as Iceland. In Iceland, HIVE’s current operating facilities represent 3.8 MW in electricity consumption. Completion of the Sweden Data Centre is subject to a number of conditions, including but not limited to, Exchange approval.

To calculate the hash power of the second phase of the Swedish data center I used the same method as the short report, which noted from the above disclosure that Iceland would be 22% of power consumption and Sweden was 78% of power consumption. Since we already know the hash power from Iceland as well as from the first data center in Sweden It just takes a little bit of math and isolate the second phase in Sweden:

Conclusion

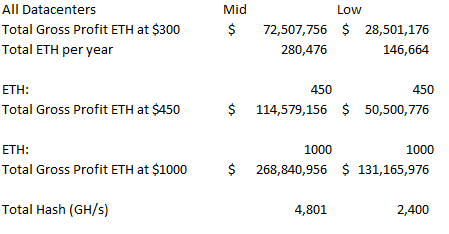

So where does this all leave us? Well HIVE may not be super cheap, but neither does it appear to be outrageously expensive. I actually think it’s a pretty interesting way of playing the rise in the Ethereum price (this is something I never would have expected to say a month ago!). Below is the summation of the profitability of all of the 4 data centers at 3 different Ethereum prices. Again, remember it’s the low case column that is the likely one, at least given the information that is available.

Of course the numbers above don’t include G&A and taxes so some adjustment has to be made for that. With 280 million shares outstanding HIVE has had a market capitalization on Friday of $650 million USD. That capitalization doesn’t seem all that out of line with the low case profitability at $450 Ethereum even adjusting for some G&A and tax. Especially given the upside blue-sky potential for crypto-currencies and the probability that their relationship with Genesis will lead to more data center deals in the future.

With that said there are plenty of questions remaining. How long before the profitability drops? How quickly does the equipment need replacing? How old are the Iceland data centers? Is the business actually sustainable over a longer period of time, in particular if the proof of stake changes are implemented?

I don’t have firm answers to those questions yet. I bought the stock Friday and there is still a lot of digging to be done. But in the short term, I’m not even sure how relevant those answers are to the primary question, which is where the stock price goes from here. Its already moved big time today (Monday) and I added a little more at the open this morning. I suspect we are relatively early on in the speculative excesses of blockchain technologies. If HIVE can show the above level of profitability and more investors begin to clue into that, I think there is a better chance the stock price moves higher than lower. And that’s ultimately what we’re all in this for.

Overstock took some back today.

sure did.

Though derivative plays are a sucker’s bet, I made just that with GROW, an investment manager which owns a large slug of restricted HIVE shares and has more in its managed/affiliated accounts. I like that it has a pretty pristine balance sheet and is both a primary and secondary derivative play on HIVE. On the downside, it’s a subscale company with mostly ho-hum offerings.

Also, that’s an excellent point about equipment replacement. It really is like mining!

Not blockchain related, but check out yangaroo, trades at 10% yield (after restructuring kicks in next year). 90% of costs are fixed. they are looking to take ad market share of 10%, that would be $40 million of revenue.

If you are looking for a potential multibagger this one is probably it 🙂 It is my largest position now.

Thanks I looked but it looked like revenues were leveling off a little in Q3. Do you think revenues accelerate again or is it more of a story driven by cost reductions?

See my analysis on this. My opinion is that the stock could go to $10 – i outline reasons in article I published below.

View at Medium.com

Thanks, good article. What do you think the proof of stake change, when it is made, would mean for HIVE? I ask because it sounds like you understand this stuff better than I do.

Because Ethereum could switch to Proof of Stake in the next 1-to-5 years (the technology to build Proof of Stake is Sharding and it is not ready), the altcoin marketplace has several proof of work contenders. For example, Monero, ZCash, and a few others. Profitability is there at this stage for mining, and should Ethereum’s Proof of Stake disincentive take hold, the mining datacenters would immediately place their bets on the next coin/token.

https://www.neptunedash.com/blog/the-best-low-risk-big-upside-cryptocurrency-play-of-early-2018/

this will blow others away