Precision Therapeutics – Buying into the Sales Ramp

Precision Therapeutics (AIPT) is roughly a $12 million dollar market cap company. They have 11 million shares outstanding and no debt. After a January share and warrant capital raise (which I am including in my share count) they should have about $4 million of cash on hand. They also have a $1 million note receivable from joint venture partner Cytobioscience.

The recent share and warrant raise diluted shareholders significantly. The placement was for 2.9 million units, consisting of shares at $0.95 and 0.3 warrants prices at $1 per share. This was a $1.50 stock as recently as November.

Precision raised the cash because they are burning cash. I estimate cash burn per quarter is about $1 million per quarter. This will probably continue.

Those are the facts, most of them not pretty. So why did I take a position?

The STREAMWAY System

Precision markets a medical fluid waste disposal system called the Streamway System. The system is a wall mounted device located in the operating room. During procedures surgical waste fluid is continuously removed via suction, passed through proprietary filters, measured and recorded, and then passed directly into the building’s sanitary sewer.

This is very different than traditional waste handling during procedures. Competitive solutions use mobile carts and disposable cannisters that have to be replaced, often multiple times during the procedure, and in many cases treated with gels to minimize the chance of contamination. Even so, accidents occur and they are expensive. Hospitals spend $4,500 on average for a mishap.

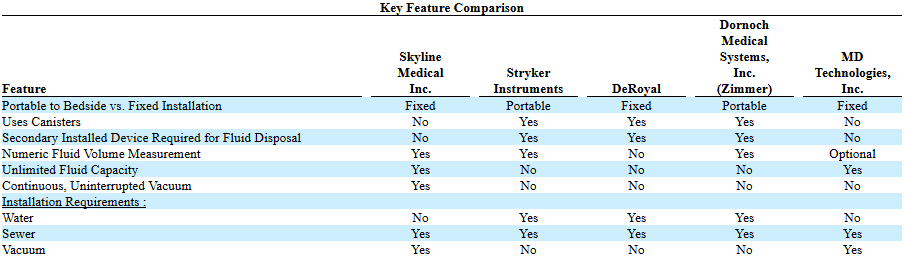

Here is a look at Streamway (Skyline is the former name of Precision) and its competition:

The Streamway system has a number of advantages over incumbent waste disposal options:

- Price: Cost of the unit is similar to slightly less than competition (Stryker system plus docking station costs $34,000 though I suspect they have been discounting to try to squeeze Streamway), but the disposable cost is 1/2 to 1/8 of the cost of replacing cannisters

- Safety: no chance to spill fluid or to have an accidental catheter removal during a cannister change

- Labour: cannisters have to be changed during a procedure anywhere between 2-10 times. This is entirely eliminated with Streamway

- Accuracy: can more accurately estimate volume extraction than the manual estimation using cannisters

- Ease of use: removal of clumsy cannisters, latching, and replaces with simple instrument panel with instructions

- Time: Procedures do not have to be stopped to replace cannisters which can result into 20-50% faster surgery

The primary negative with Streamway is installation. It has to be hooked up to the sewage line and therefore the operating room needs to be shut down and the wall cut open to complete the install. This has been a sticking point, particularly as hospitals are not unhappy with the mobile carts they’ve been using. Precision has taken to emphasizing the improved safety of using Streamway.

The cost advantage of Streamway is significant. This is from the last 10-K:

A study by the Lewin Group, prepared for the Health Industry Group Purchasing Association in April 2007, reports that infectious fluid waste accounts for more than 75% of U.S. hospitals biohazard disposal costs. The study also includes findings from a bulletin published by the University of Minnesota’s Technical Assistance Program. “A vacuum system that uses reusable canisters or empties directly into the sanitary sewer can help a facility cut its infectious waste volume, and save money on labor, disposal and canister purchase costs.” The Minnesota’s Technical Assistance Program bulletin also estimated that, in a typical hospital, “. . . $75,000 would be saved annually in suction canister purchase, management and disposal cost if a canister-free vacuum system was installed.”

A second study, by the Tucson Medical Center, found similarly significant savings. They estimated they would save $22,000 per year in a single operating room. Bottle costs for the mobile unit they had installed previously were $107 per procedure. The Streamway disposable cost brings that down to $24 per procedure.

In general, the $24 price tag is a favorable disposable expense compared to the costs of replacing cannisters, waste disposal, gel costs and labor for the competing Stryker and Zimmer systems. Those systems need to have cannisters replace anywhere between 2-10 times depending on the procedure. The material and waste disposal costs can be between $25 – $100 (or more) and on top of that there are labor costs and the time cost of having to pause the procedure to empty the cannister. You add to that the risk of a contamination event (which is going to be a $4,500 hit) and its easy to see how Streamway saves money.

Struggling Sales

So you can make the argument that Streamway is a superior system. Nevertheless the company has had a horrible time ramping sales. On the third quarter conference call the CEO Carl Schwartz, came clean about what had been happening:

When I took over as CEO in 2016 like many of you I thought the Streamway System was a slam dunk…Nothing could have been further from the truth. We had two very entrenched competitors, Stryker and Zimmer, who have their units at most hospital facilities in the country. In addition they were able to bundle their units in with other operating equipment, offering substantial discounts. Furthermore, it became increasingly evident that many institutional hospital customers would not allow us to connect to the hospital sewer system because they did not want us to open the operating room wall. Given these challenges and the fact that their unit and ours effectively removed fluids, what was our competitive advantage? After several months of effort we discovered that our most competitive advantage was our ability to avoid the spread of infection in the hospital by eliminating any contact between the infectious materials and the patients and staff and we have been hammering that home where ever we present the Streamway system and in newspaper articles all over the country. As you know it has been a slow going but we are making substantial progress.

In addition to pressure from the competition in the United States, the company has been slow getting regulatory approval in non-US districts. Up until this year their sales staff and list of distributors was sparse. It was a situation where you had a solid, superior product, but it was competing against well-funded incumbents, and marketing and sales dollars were not enough to mount an offensive.

In fact it seems like management had begun to give up themselves. There was a failed merger with Cytobioscience in the summer. There was a subsequent joint venture with Helomics and a proposed one with Cytobioscience. Indeed even the strategy for 2018 includes the following statement:

To expand Skyline’s business to take advantage of emerging areas of the dynamic healthcare market. To this end, management is implementing a Merger & Acquisition strategy focused on finding and acquiring high-growth companies that have established operations and the ability to drive both revenue and capital appreciation for the Company, or entering into strategic relationships with these companies.

Even if management was just being strategic with its new diversification approach, investors were frustrated. Listening to conference calls in 2017 is a painful exercise. Lots of frustrated investors, many of them long time investors, having been expecting a steep sales ramp, saw unit sales trickle in a 1 or 2 a quarter and the share price lag.

With cash levels dwindling, management had to raise capital with the dilutive raise I mentioned previously. That, along with the failed Cytobioscience merger, was likely the last straw for many investors.

As a consequence, the share price hasn’t done well. The one year chart illustrates the disappointment:

Things are turning

I’ve had Precision Therapeutics on my watchlist for the last 6 months. I can’t remember why I added it, I’m pretty sure it was mentioned by someone on twitter though I don’t remember who. When I looked at it a number of months ago I thought they had an interesting product but there was no indication that they were gaining any sales traction. So I passed.

However that appears to be changing. In early January the company announced that they had sold 5 Streamway systems in the fourth quarter. They sold another 6 systems in January alone. I wish I had been paying a bit closer attention to the company when this news release came out, as I would have probably started buying it back then.

I did pay attention to the second news release that came out last week. Precision projected 100 systems sold in 2018 from the United States alone. I caught the stock soon after it jumped on the news.

Precision sold 10 systems in 2017. This includes at least 1 system sold in Canada. So the projection for 2018 is for at least 10x 2017 sales.

While up until now sales have drifted aimlessly, the company has been doing a lot of work behind the scenes that has set themselves up for this type of increase. They have:

- Hired 4 regional sales managers and a VP sales in early 2017. Up until the end of 2017 they had a single regional sales manager and no VP Sales.

- Signed a contract with Vizient, which is a healthcare improvement company with a $100 billion in purchasing volume, in the summer

- Partnered with Intalere, a health care supply chain manager

- Signed a 3 year agreement with Alliant Health, a Service-Disabled Veteran-Owned Small Business that sells medical device products to the federal government, to sell STREAMWAY to into Federal Hospitals

And while early sales have been sporadic, they do mark first steps toward greater penetration, opening up the opportunity for more significant deployment once the systems benefits are experienced. Take for example, the two units sold in the third quarter. Both sales were to single operating rooms across much larger hospital networks, in one case a 6 facility network and in the other a 11 facility network. On the third quarter call Schwartz said they were in discussions to standardize waste management across each network.

Foreshadowing the increase in sales, Precision did 92 demos in the first three quarters and equaled that amount in the fourth quarter alone. They did 145 quotes in the first 3 quarters, and more than 75 in the fourth quarter.

International sales have been even slower to come then domestic, but in the last 6 months Precision has made some strides there as well. In June they got the CE mark for the system, which allows them to start selling the devices into Europe. Later in the year they partnered with Device Technologies, which will be selling Streamway in Australia, New Zealand, Fiji and the Pacific Islands (they seemed quite excited about the Australia opportunity on their third quarter conference call). They added a distributor in Canada as well as have been selling systems directly. They added another distributor selling into Switzerland in November and opened a European office a few days ago. Its worth pointing out that the 100 unit sales projection is not including any sales outside of North America.

One time and Recurring Revenue

Streamway systems retail for about $24,000 per unit. 100 units should equate to around $2.4 million in revenue.

That will be a big uptick from 2017 revenue. The company has been printing quarterly sales in the $100,000-$150,000 range for the last few years, so the 5 Streamway units sold in the fourth quarter and the 6 and January should provide a nice revenue ramp.

However maybe the more important consideration is that as more Streamways are installed into operating rooms, recurring revenue will scale as well.

Precision generates recurring revenue from the sales of disposable filters and cleaning fluid. According to the 10-K, the filter and fluid retail for $24. The company recommends changing the filter and cleaning the unit (with the fluid) after every procedure.

I think hospitals are doing this more like every 2-3 days. Nevertheless, Precision has been generating about $100,000 of revenue per quarter from the sales of the disposables. Given that there is about 100 units currently in operation, it works out to $1,000 of revenue /unit/quarter. While the company doesn’t provide margins from disposables, its pretty easy to estimate them. In the second quarter no Streamway units were sold, and the company generated $106,000 at 80% gross margins.

It looks like the average operating room performs 2-3 surgeries per day. If hospitals actually used the disposables after every surgery, I estimate revenue would be more like $4,300 to $6,500 per quarter per unit sold, or over 4-6x what I estimate it is now. That’s a lot of reason to promote proper usage.

Even at the current disposable usage rate, 100 extra units means $400,000 more high margin recurring revenue annually. Add that to existing consumable revenue, and add on the $2.4 million from unit sales, and I get annual revenue of about $3.2 million for 2018.

CRO Joint Ventures

Probably because Streamway sales have been slow, management has looked to alternative lines of business to boost interest in the stock. The initiatives kicked off in the summer with an announced merger with Cytobioscience, a contract research organization (CRO) that specializes in testing the cardiac safety of drug compounds. The merger was subsequently postponed in favor of a joint venture in November, and at the same time a second joint venture was announced with Helomics, another CRO company.

As it stands now, Precision has a 25% ownership stake in Helomics and a $1 million loan to Cytobioscience. The joint venture with Cytobioscience was supposed to close by year end but I haven’t seen anything to that effect. Listening to the last conference, it seems like even the merger with Cytobioscience may take place once audits and accounting work are completed (it was suggested that the merger didn’t transpire because of auditing required on Cytobioscience before it could be merged with a public company). On the other hand this article, which I can’t read in its entirety, says that Cytobioscience walked away from the merger, so who really knows.

I don’t know what to make of these two joint ventures and the move into CRO. It seems like the CRO business is growing. Whether these companies are at the forefront is anyone’s guess. Cytobioscience said on the second quarter call that they expected $700,000 of revenue a month by the first quarter of 2018. Helomics, which specializes in customizing cancer treatment based on finding patterns with their patient database, is in a growing field.

I’m also not entirely sure why these companies want to merge with Precision. The Streamway doesn’t really have a strong connection to the CRO businesses that they operate from what I can tell. Precision does have net operating losses of $11 million that could be utilized against future profits. So maybe that’s it?

Just last week the Economist dedicated an article (and a cover) to the emerging field of using data to provide better diagnosis and treatment. The article talks about using AI to better customize treatment to patients. That is essentially what Precision will be trying to do in their partnership with Helomics.

Summary

Cash on hand should be enough to get Precision through 2018, and maybe further depending on how these sales develop and how much they end up spending on partnerships. If I ignore cash, the price to sales (P/S) multiple that the company trades at is 3.5x. Including cash its more like 2.5x.

Given the growth (10x the revenue in 2017), the margins (gross margins of 80%), and momentum in engagements across the United States and internationally, this doesn’t seem out of line to me.

The stock is hated by investors because it has disappointed for so long. There is a long list of bashers I’ve seen on twitter and a few on SeekingAlpha. None of these bashers have brought up a point that has concerned me though. They are mostly just rehashing past price declines.

I think the stock moves higher. At the very least it should get back to its November levels, which were above $1.50. If there is evidence that the strengthening of sales of Streamway is sustainable over multiple years though, that should just be the beginning. The recurring nature of the disposable sales adds a lot of value as more systems are installed. Finally, if the Cytobioscience merger becomes a “go” again, that would be another catalyst to the stock.

So you have a beaten down stock, pretty clear indications of sales momentum, and the outside chance that something bigger is announced. All around it seems like a decent bet.

Note: I have been told there is a SeekingAlpha article by Jonathon Verenger on Precision that is quite good. I haven’t read it yet because I wanted to write up my own ideas first without influence.

The stars seem pretty much aligned on this one.

Do you have any new thoughts on you holdings Medicure and Radcom?

I’m quite excited about Radcom. I dont know if I was as diligent in my online portfolio but I had sold a lot of my RDCM a few months ago. However I’ve bought almost all of it back. I was going to write up something because of this recent article in light reading:

http://www.lightreading.com/testing/monitoring-and-assurance/how-radcoms-pricing-model-is-set-to-disrupt-the-market-/d/d-id/740395?_mc=RSS_LR_EDT

Mike Arnold wrote something up in SeekingAlpha which is good too. I think 4.5x TTM revenue given that their revenue stream is recurring (like the Light Reading points out its kinda like an unlimited use subscription to the software) is fairly cheap given the growth opp.

With Medicure we will just have to see what they do with the cash and how the new indications ramp. So the EV is about $55mm, they have $4/share in cash, and Aggrastat does about $7-$8mm of EBITDA. Its not expensive but Aggrastate probably doesnt have a big growth profile so they need growth from some of these new indications they are launching to get everyone excited. If the stock sold down to say $6 I would buy more but I doubt it does. It probably just sits here until there is more clarity about growth plans.

Thank you!

Medicure

I found it interesting that there was no reaction in the market at all, when Prexxartan was approved in December, whereas their financial results hammered them down.

Radcom

I saw the article as well. Quite encouraging. They will report on Tuesday, that will be interesting especially if there is some guidance.

Yeah exactly. I keep waffling on whether I should add to MPH. The thing holding me back is the price pressures on Aggrastat and whether in the short run that is more the focus on the market than Prexxartan launch – I mean in all likelihood we dont get significant numbers out of Prexxartan right away whereas another couple $7mm quarters from Aggrastat might not be received that well

I guess I wouldn’t average down, at least not now. I am not sure, how long it will take to ramp up sales for Prexxartan and it will probably only move the share price if they either give good guidance, or have good numbers already. On the other hand, it’s an oral solution (the only one available), which makes it easier to take for patients, to prescribe for doctors and likely increases compliance.

But they also have to pay 0.4M for approval, royalties and milestone payments from net revenues. I don’t like that.

What do you think of the other 3 indications they have coming?

Good question.

First of all it is good that the pipeline is full and near term. Since they are generics approval is probably safe but then they will certainly be no blockbusters. There is also a lot of competition in terms of acute care cardiovascular injectables for example. How much can they gain?

I don’t know to be honest.

I think it really comes down to growing revenues and especially earnings substantially to move the needle in the stock price. This is not exactly an exciting, wildly followed stock. There is 1 article on SA a year ago.

What do you think?

“net loss for the nine months ended September 30, 2017 of $8.0 million which includes a $10.2 million loss from the Apicore business ”

That won’t happen again because they sold it and receive 105M.

They have also paid back all their long term debt with 9.5% interest rate, which makes another 5-6M.

Management seems to be good, also BoD. I mean they were pretty successful at least from 2008 on. But they like to pay themselves richly, the options bug me abit.

SG&A to Revenue is 50% and they say it’s because they are building the business. There is some potential for reduction.

https://www.statista.com/statistics/266321/sganda-to-sales-rate-of-top-pharmaceutical-companies/

Seems like Radcom is pretty much fairly valued? Some of revenues are not recurring as well. If OPEX stays fixed, and they grow 25% in 2019 and 2020 from expected base of $46m in revenue in 2018, they will do about $25-26m in EBIT in 2020. A 20% tax rate and that is $20m. a 20x multiple on that gets me to only 70% upside over several years IF they grow 25% in 2019 and 2020 and if opex stays indeed fixed?

Also 4-5x revenue for a software company does not seem that cheap? And it seems the recurring part of the company is projects and warranty revenue? Since the products part has lower gross margins and is more choppy. In that case the multiple to recurring revenue is much higher? (closer to 10x).

I havent gone through using your numbers but they look right and I don’t disagree with them. My take is if that’s the growth rate in 2019 and 2020 then RDCM has failed, and thus in that scenario the stock is definitely overvalued at current levels.

The growth rate implies $8mm more revenue in 2018, $11mm in 2019, and $14mm in 2019.

With those numbers in mind, I’ve been looking at it like this. We know the win with AT&T has become $18mm and I think should grow incrementally next year. The Verizon foot in the door win was $5mm and I think it fair to say (you can disagree) that Verizon will grow to close the size of AT&T if Radcom is successful in taking over the architecture the same way as they did with AT&T and more of VZ network migrates to 5G.

So I gauge that full wins on Tier 1s should be $15mm to $18mm, and hopefully even more as Radcom expands into adjacent areas.

If thats the case then the growth numbers you are using imply that in 2018 RDCM has integrated VZ and gotten a little more revenue from AT&T or some other smaller deal, then in 2019 essentially converted VZ to a full win, and then in 2020 it gets one more $15mm win. If its into 2020 and RDCM has AT&T, Verizon, and one more win, then something else has gone wrong with the thesis. Either NFV isn’t getting adopted or a competitor has caught up or something.

These negative scenarios are possible. I’m not saying that I think this is a slam dunk. I just dont think that growth rate represents the optimistic angle.

The nice thing about RDCM is b/c of contract size, even if they just get 2 wins instead of 1 per year those growth rates go up substantially. Add 1 $15mm win half way through each of 2018, 2019 and 2020 to the numbers. So that by 2020 they have 4.5 wins worth of revenue, ie. AT&T, VZ, 2 other full wins, and 1 onboarding. Its one win a year, which doesn’t seem like a lot to me. In that case we are at $109mm of revenue in 2020.

All of this incremental revenue, if the LightReading story is right, should be recurring.

My hope is that even that 1 win a year scenario is underestimating the ramp. I am hopeful that once the CSPs start migrating, there will be an onslaught of deals. There are a lot of telcos out there. My real blue sky upside is we see a year with 3 or 4 deals or more. But I am using the word “hope” intentionally. I don’t have evidence this will happen, other than the herd mentality we see occur when a new technology finally goes mainstream.

So the rebuttal you can give to me is – yeah but its been 2 years and all they have is AT&T and a slice of VZ. Thats totally fair. Thats why I sold the stock in the fall. But I’m back in partially b/c of level ($17 has been good support for a while) and partially b/c what I’m reading suggests that while I was too early last year and telcos move like dinosaurs to a new gen, the flow of deals might be about to pick up.

Thanks for detailed response.

If you like this one, you probably like Yangaroo as well. It has gone up a bit since I last mentioned it here, but still very attractive IMO. Software company trading at 2.5x revenue, 90%+ gross margins, with a competitor in advertising with 85% market share who has been slipping lately. Chairman has bought a ton of shares recently (who is pretty well connected in ad industry). Only trading at about 10x 2018 earnings as well (assuming they don’t grow much further). The award and music revenues are mostly recurring while advertising revenues are per video. Their tech is better than competitor (less downtime and lower cost to operate), and customers are looking to not have to use just one provider. They plan to take 10% of the ad market, which would amount to about $40 million in revenue just for ad side.

I looked at YOO and I put in a bid a 30c but didnt get it filled. Agree it looks ok.

If you want to read Mr. Verenger’s article about AIPT, do it quickly. Seeking Alpha just implemented a policy that puts articles more than ten days old behind a paywall.

Assuming they have a free cash flow loss now around $4.5M CAD and they have a (discounted) selling price around $20K CAD, they need to sell about 225 units per year to reach cash flow breakeven, which would be a key milestone. 100 units per year is significant relative to that, so this is really worth watching.

A small company like this should have been doing OEM deals earlier on in international markets. Sell OEM licenses to South America, Europe, Japan, Australia, and Asia, for example. Each of those licenses might have paid multi-millions up front fixed license fees and provided enough operating revenue to take the stress off liquidity. They need to be more realistic about how small of a company they actually are.

What you describe in terms of reorganization sounds perfect. They are focusing on sales organization, and the fact that this immediately produces such outsized results is very positive.

How big do you think their addressable market is in North America alone?

I tried to answer the addressable market in my other comment. As for units they need to sell, the way I think about it, and I didn’t say this in the post because i think it sounds sensational, but if they do 10x sales this year how many do they do next year? Is this year a total fluke and the growth rate drops to a double digit percent? Or is this an inflection, and maybe next year they do 3x or even 5x. In both cases they blow away cash flow breakeven before you even consider the disposables they start selling. Thats the opportunity here IMO. If this sales number is real and rooted in the realization of a true competitive advantage, then 2019 should be at least close to the same order of magnitude and that gives the stock real home run potential. On the other hand if this year is a fluke then it probably turns into a dud stock.

One thing I don’t like about Precision is the letter you shared with 2018 goals:

http://investors.skylinemedical.com/news-releases/news-release-details/skyline-medical-issues-letter-shareholders-0

This basically reads like a capitulation statement on their existing business and says they want to get into contract research. Contract research is a commodity business where they have no competitive advantage. That letter says they are doubling the share count pool so they can dilute further to buy a new company in this new line of business. I think this can only defocus them and it will act as a weight on the share price. You express similar doubts with a different focus in your article.

It’s quite bizarre that they defocus like this when they are starting to ramp sales on their primary product.

Have you found anything that says what is the total addressable market is for this system? They say in one document that 50 million canisters end up in landfills each year. If we knew the average number of canisters per room where they are used, we might have some idea of how many emergency/procedure rooms might be candidates to use these.

Thats true. You should also listen to the Q3 cc. Its even more depressing as they give all the details why they’ve failed to grow sales. Similarly, consider in the name change press release they didn’t even mention Streamway in the main text.

I don’t know specifics on size beyond what they have said in the 10K: We benefit by having our products address both the procedure market of nearly 51.6 million inpatient procedures (CDC, National Hospital Discharge Survey: 2010 table) as well as the hospital operating room market (approximately 40,000 operating rooms).

I havent seen a more specific TAM mentioned elsewhere.

Hi Lsigurd,

This one could have potential but what about competition?

MD Technology seems to be offering a similar solution (have been for years). I think the main argument here is: There is a market, but until recently, AIPT was not able to serve that market and because they now have their sales team in place, they will be able to ramp quickly. But this begs the question why MD Tech did not ramp in the last years, and if they did, why this would not hurt AIPT’s ramp.

Another thing is the proprietary nature of their product: To what extent can this be copied by the big players. It is stated that its patented, but MD technology has a pretty similar system if you ask me? Why wouldn’t Stryker be able to create a similar system, and push it to customers? (obviously FDA approvals required, but that is a hurdle that they should be able to take)

Sure. I looked at MD Technologies. Here’s what I thought. They have a similar product. Its not truly continuous suction so I would assume that means the procedures have to be interrupted to empty, though I don’t know for how long given that they have some sort of two cannister solution where you switch back and forth. That seems like a benefit of Streamline over the Zimmer and Stryker products. They are very small; their linkedin page says 2-10 employees and revenue looks like its just over $1mm for all their products. They’ve been around since 1992. It looks like their product has been around since at least 2013.

So my question is, what’s the thesis that this is company is significant competition? I mean look how hard it was for for Skyline to get any traction in Streamway. It just doesn’t seem like the issue here has been a competitively similar product. Its trying to get in the door against two very large, well funded and well established competitors, Stryker and Zimmer. Give me some evidence if you think I’m wrong but I don’t think MD’s product is going to be a limiting factor on the growth here.

As for Stryker and Zimmer, maybe its plausible that they develop their own products. It couldn’t be continuous suction b/c thats patented. But it could be like the DM6000 and be almost continuous. So that might happen. But why now? They didn’t jump at this new product before, the only thing that’s changed now is Streamline is showing momentum. If thats the element that’s changed, why not just buy Precision, or at least the Streamway segment? Zimmer and Stryker are competing against one another too; if one decides to build their own line, the other is probably going to catch up a lot faster and maybe get ahead of the game by buying Streamline.

So I don’t get it? Why the concern? I don’t understand why MD would suddenly turn into some huge competitive juggernaut when I see no evidence of the sort? They have a similar product but that was the same thing last year and the year before and it seems like both companies couldn’t sell much in the past (judging from their revenue). Is it just that if Streamline is having momentum then MD must too? Given the background that led to this surge, I’m not sure why that would be the case?

Anyways, those are my thoughts.

Ok, fair enough on Stryker and Zimmer.

I hope you don’t mind my ignorance on the other point about MD. Haven’t done a lot of in depth research, and I agree that if they employ 2-10 staff, they likely don;t have what it takes to penetrate.

I found these websites,which seems to suggest they have direct connection to the sewer just like streamline. This raised my questions about the strength of the patents in the first place, and caused the initial worry about a ‘similar’ product already on the market for years.

https://www.surgicalproductsmag.com/product-release/2013/04/environ-mate-dm6000-series

http://www.mdtechnologiesinc.com/dm6000series.html

Am I misunderstanding the information provided in the links above, or do they indeed have a sewer connected system which can handle unlimited volumke (the 2A version)?

JG

In the 10K it says all competitors have products with a connection to the sewer system.

In the 10K this is what it says about MDs product:

We believe that this continuous operation and unlimited capacity feature provides us with a significant competitive advantage, particularly on large fluid generating procedures. All competing products, except certain models of MD Technologies, have a finite fluid collection capacity necessitating that the device be emptied when capacity is reached during the surgical procedure. In the case of MD Technologies while some of their models may have an unlimited capacity their process is not continuous because it requires switching the vacuum containers when one becomes full. For example, when the first container becomes full, the vacuum is switched over to a second container to collect the fluid in the second container while the fluid in the first container is drained. When the second container becomes full, the vacuum is again switched back to the first container to collect fluid while the second container is drained, and so on. Even though the switching of the vacuum between containers is automated in certain MD Technology models, the automated switching results in brief interruptions or reductions in suction during the surgical procedure.

Ok, Thanks for the additional info. 10-K always helps out 🙂

I can imagine that surgeons prefer the Streamway system then. I certainly see potential here, and I might ask some questions on the next call. Would be mostly interested to hear how much of their projected sales volumes is based on discussions with existing clients vs extrapolations of recent sales to new customers.

Its not that one is better than the other but it provides more insight in upside. If most of these 100 unit sales are based on expectations rooted in sales to new customers in Q4/Q1 it shows that their sales organization is performing better and might be gaining traction. However, such sales have a higher degree of uncertainty imo than potential sales to existing customers (who supposedly are already happy with the system).

Those are good points. To me, the story is about the sales number they released. There are plenty of holes you can poke in the product and why it should or shouldn’t ramp, ie. the larger incumbants with more promotion, reluctance of hospitals to poke holes in wall during installation, whether the final product is worth the trouble of tossing the cart you are using and replacing it, etc. Those are all potentially valid points and I don’t know any more then anyone else. But when a company releases a projection like this I tend to believe it, so until they prove otherwise I’m willing to play this out and see what this year and next year bring.

Hi Lsigurd, Precision has me interested, thanks for article. My take is it is a financing issue. If they can get finance company behind them they can install these for free. The finance company buys it and pays for hole in wall., then finance company takes 50% of cost savings or maybe Precision and Finance take 50%. Free for hospital and they save money from day one. If you have their ear maybe mention this.

A company called Accuray (radiation treatment) used this method more or less and their sales jumped afterwards. I know 2 people in upper management of it in early years and they said it turned the company around.

I bot some today and this came out

March 29 (Reuters) – Precision Therapeutics Inc(AIPT):

* PRECISION THERAPEUTICS ANNOUNCES RECORD STREAMWAY® SYSTEM SALES IN THE FIRST THREE MONTHS OF 2018

* PRECISION THERAPEUTICS INC(AIPT) – SKYLINE MEDICAL SOLD 16 STREAMWAY SYSTEMS IN Q1 OF 2018

* PRECISION THERAPEUTICS INC(AIPT) – CO CONTINUES TO PROJECT A TOTAL OF 100 STREAMWAY SYSTEM SALES IN 2018 Source text for Eikon: Further company coverage:

Funny that they released all the sales data ahead of earnings. Also funny that they didn’t refer to Streamway when they described themselves in the PR announcing the earnings date. I really wonder if Streamway is getting sold off, it seems like they are more intent to build the precision medicine business.

I actually heard a similar idea from another investor. It makes sense if they view it as a true razor/razorblade model – why not get it in as many hospitals as possible as quickly as possible?

In video today, Carl specifically said they want to keep Streamway.

FWIW I watched that video last week. Its not new.

Thanks Lsigurd for answers! BTW just looked at your long term record again, highly impressive.

I was on CC yesterday. They sold 10 in 2017 and 10 in March, that is 1100% run rate growth. They project 100 this year and in CC said breakeven is 200-250 units and they expect that in 2019, so indeed I would want them to hold onto Streamway. 2018 think they will have 55% consumables rev, enticing mix.

The Precision stuff does look worthwhile. Someone in Feb on Seeking Alpha said he thinks roughly $150 million is worth of just AIPT stake in Helios if have spelling right. Do you have any opinion on that?

I have bot about $30k of the stock and was surprised by 25% selloff today after results. Do you have any thoughts on selloff?

I can only guess there is a dilution fear due to current negative cashflow.

Its gotta be the dilution comments. They didn’t handle that question very well. I still think its a good idea even though I’m well underwater now. That $3.5mm to $4mm is right inline with what I’d hope for and that comment, in response to your question I think, that they’d see 50%+ revenue from disposables is pretty significant too. If thats the case and with sales ramping like they are its really only worth 2x sales or so? That doesnt seem right to me. I added here at 85c, so we’ll see how that works.

Thanks again for answering ?s I was the one that asked dilution question, so maybe the bad guy 😉

Yes on the face of it seems very cheap to just Streamway, ignoring precision stuff which I am not ignoring. This is a company that research time by investor is productive on, it could be 10-20 bagger on the face of it. I am not up on conv debt effect if all converted, maybe that is it. But it seems Carl has been truly in charge for 2 years and results are radically better.

Everything is going the right direction except dilution prospects, which are going to continue to be a cloud over the stock after the 10K comments. Neverthless I’m holding. $3.5mm-$4mm of revenue, half of that recurring should get 4x, 5x sales IMO,probably more if they can show the growth is real and 2019 can be 200+ units.

Maybe the only other thing that made me scratch my head on that call was the 50%+ revenue from disposables. That would kinda suggest that they are going to get $1.75mm to $2mm from the Streamways, which would mean they are selling those Streamways at a discount to the $24,900 they say in their 10K. Maybe thats the financing you asked about? I’m not sure, but I couldnt quite reconcile the disposable sales % they said.

Forgot, asked them about financing Streamways and they said they do that already.

The comment about them doing more acquisitions was also a negative in my world. Just focus on the tasks at hand, its not like they have the money to start ‘consolidating’ smaller players.

Combined with their boilerplate style of communicating the numbers about their sales beforehand, makes me believe they might have something planned sooner rather then later.

I also wonder how SG&A will develop now that they ramped their sales organization. I guess we will have a better understanding in Q1. Should also tell us something about the revenue amount they will generate from their acquisition. Also looking for more information on that 2019 Break-even target. I can make those numbers work, but it would require reaching their sales target, followed by >100% 2019 growth (keeping disposables constant for now) while growing SG&A only modestly.

They said something in the 10K about burning cash at a $380k per month rate which give you an idea of SG&A right now

JG, I agree, there is no need to acquire more companies unless it helps same precision endeavor. The CEO does have a history of growing a big company in plastics industry.

In 1988 Dr. Schwartz joined a family business, becoming chief executive officer of Plastics Research Corporation, a Flint, Mich. manufacturer of structural foam molding, a low pressure injection molding process. While there, he led its growth from $2 million in revenues and 20 employees, to its becoming the largest manufacturer of structural foam molding products under one roof in the U.S. with more than $60 million in revenues and 300 employees when he retired in 2001.

He retired, and being born in 1941 that means he is about 77 now. Looked good in video today https://www.youtube.com/watch?time_continue=6&v=zeyZY4c0sw4 o That video seems to have caused a 50% rise after yesterdays 25% crash, this wildness seems unwarranted. Any thoughts?

I bot more at about .80 and then blinked a few times when saw 1.20 shortly there after, so sold some of that. In an IRA maybe will trigger something bad but 50% in less than an hour maybe worth it. Bot some more in another acct at .97 after that. If I knew all the facts and things are as seem, might make it my #1 position.

Yeah I pretty much followed that pattern as well.

Hi Lsigurd, Looking at stock chat boards there are a lot of posters (maybe shorts) that think management are crooks at AIPT and will dilute. Any thoughts on that?

We overlap on many stocks, I have bot AIPT and SNOA based on your research, but independently we have about 5 other stocks in common.

Two other stocks with near zero following that may be of interest to you are ESOA and GFG.v On GFG.v same team that I made last 20+ bagger on (CLGRF). They seem to have two big projects in pipeline and were very successful at Claude. On ESOA .07 x Sales and profitable. One more, Tim Saboz on SA has written article on SHOS that got my attention and have bot some, bounced big today on no news, you might also find of interest.

All ears on what you think of all three.

Cheers

So I’ve never talked with the management team and so I really can’t speak to much about them, but from what I’ve gathered on CCs they’ve always seemed fair to me. I think they had a tough sell with streamway and its been a slog but I dont know if that is necessarily on them.

But I also dont really get the precision medicine angle, it had nothing to do with why I got in the stock and while I see that there could be tremendous upside if they become the next FMC or whatnot, I worry about what they are doing going off in this direction when they seem to finally have found their feet with streamway. It seems pretty likely that they are going to takeover helomics and so there is going to be stock with that. I’ve assumed that the stock will be in return for the helomics business, so hopefully the upside from acquiring that business into the fold makes up for the issuance. I’d be pretty annoyed if they actually went to the market to raise cash to purchase helomics, especially at 90c.

You know I actually own ESOA. Small world. I just don’t talk about them because they are so illiquid and tiny and so what’s the point? But I like the stock here; its been decimated, the industry is turning the corner, if they can get even the slightest bit of pricing on their next string of contracts then they could make some money and hopefully the stock could get back to where it was even last summer. I’ll have to check out the other two, never heard of them. Thanks!

It is a small world, you are the only other ESOA investor I know. They did get a huge contract (over $40 million think in April) and it will be over in less than a year so a nearby rev thing. IR is terrible, I have called 3 times and have not got a call back, maybe they are afraid of being yelled at, which I do not do.

Thanks yeah I saw the contract, its promising but man those margins are frustrating. They had previously implied they’d get it together this year but not so much in Q2. I’m holding but I’m not going to add till they can show some ability to get some margin in their jobs.

Btw – what were the boards you saw this on?

Hi Lane, it was iHub. I listened to the CC yesterday, was amazed. The CEO said Helomics will be breakeven by 3Q, they will grow tumors by 4Q. Also they said Helomics spent $180 million to build database, yet AIPT bot them for $5 million roughly. 18 headcount at Helomics.

I was more excited about Streamways until the CC, now think Helomics/Tumor Genesis side alone can 10 to 100 bag AIPT.

here is transcript of CC, well worthwhile to read. https://seekingalpha.com/article/4174452-precision-therapeutics-aipt-ceo-carl-schwartz-q1-2018-results-earnings-call-transcript

I listened to the call as well. Its was positive. I am hopeful that Helomics will indeed be CF neutral by Q3. I was disappointed in the Streamway sales. The fact that they wouldnt give a number for how many so far this quarter (only saying they expect 16 in Q2 as a whole) makes me think its probably low.

I see from your portfolio Lane that you sold AIPT. After reading the CC think you may be interested. Let us know.

No I haven’t sold AIPT. If you look at the portfolio its still there. 11,000 shares just like the month before. I briefly added more shares before I thought against it but I’ve held those 11,000 shares throughout.

Thanks for answers Lane. I must have misread report, glad to hear you are still in it.

I have about 40,000 now. Have call into them, still have lots of questions now that am so interested. The idea that Helomics will be breakeven this year is so much better than guessed. They could easily have 100-200 million mkt cap today. Plenty of companies with less going for them do. And they have proven business leader at helm. Took a family biz over at $2 million and took it to $60 million.

Thanks, thats interesting. I didn’t know that about the Helomics management. I’m hopeful they can turn all that R&D into stock value. I’m also curious to see what happens when the merger is finalized. It may just be another day on the market, but sometimes when you get the firm news on a little stock like this it really brings in the money. I know at times I’ve been surprised with the big moves a micro-cap can have after previously known news becomes finalized.

Today I talked with the CFO Bob. Very pleasant fellow, seemed rational and on top of the company. BTW the rational thing is not to be taken for granted. Musk has people wondering on that aspect after his CC.

And on your point Lane, a finalized deal not LOI, that could be major factor, although being they are in CC calls together have to think its 80% plus.

I was looking for what am missing how can this be this low now? Could find nothing. Its cleaner than guessed. No debt, no conv bonds for dilution. It is extra clean and simple for a $15 million mkt cap company that has lost money in the past. What you see in financials seems to be it. It really is a $15 million mkt cap company. I found out not only did Dr. Carl take a plastics biz from $2 to $60 million, before that he grew his dental practice to over 10 locations. That is quite the biz record, and sales are way up since he took over. Bob has a high opinion of him.

I told the CFO it is one of the most undervalued companies have ever seen and he had trouble arguing with me.

Voice tone is a big thing, why I listen to CC calls and call companies. You can gauge confidence in future or fear of it in calls. Example SAEX was very nervous in last years CC, well got out and its down 65% since. You can flat out make money off of voice tone.

JMHO the team in CC and Bob today really think the future is bright for AIPT.

Another investor has put the audio up on YouTube which found. For those that missed it suggest listening. Think this thing can 5 bag in one year and maybe 30 bag long term.

See over 60 people have listened https://www.youtube.com/watch?v=JQnw5xNfzHo

So what is the potential? FMI would be a competitor, $3 billion market cap, 16X Sales and losing a lot of money. AIPT (for precision segment) is tiny but may be making money in 6 months and may in their niche be better technology than FMI. Dr. Carl (first name) said in call over $500 in rev for AIPT is not crazy, FMI has 180 million now and 3 Billion mkt cap.

One of the most exciting stocks have ever seen for risk/reward. Mentioned you to Bob and he invites you to call if you wish.

Whoops, meant $500 million in rev not $500

Wow thats great info thanks. I have seen that comparison to FMI and it looks pretty exciting, though I still feel like I dont really understand the space well enough to be able to really compare AIPT and FMI with confidence.

Research on Helomics and field of Precision Medicine. Both ended up better than guessed. Check out this video tour of Helomics headquarters where they explain what they do for revenue and them doing it, quite good.

Here is a brand new Harvard article on the field of precision medicine for cancer, good results, fascinating.

https://harvardmagazine.com/2018/05/precision-medicine-cancer

Thanks, I’ll check them out.

Thanks Lane for your replies. Next step is Helomics deal closing, then guessing they will release news as to how they will pull off 3Q positive cashflow. Guessing That will be CRO contracts.

You bet. I hope it works out as well!

up 17% today, looks like a short squeeze? New website too http://www.precisiontherapeutics.com/

Yeah great day. I hope its more than a squeeze as the stock tends to come straight back down on spikes otherwise.

it held rally nicely and is going up again today.

Cheers

Well after running over 1.30 it pulled back to a buck and now 1.12, might be nervousness on merger deal, it has been longer than what they projected, May.

Any new insights? A Helomics like company was just bot for $5 billion, AIPT tweeted that yesterday, which is deal was falling apart they likely would not mention.

No new insights. Just waiting on the merger. FMI got bought I see.

Thanks! If I call will post what find out.

That John Dunfee guy tweeted that the deal is done. Any evidence that is true?

June 28 (Reuters) – Precision Therapeutics Inc(AIPT):

* PRECISION THERAPEUTICS SIGNS DEFINITIVE MERGER AGREEMENT WITH HELOMICS HOLDING CORPORATION

* PRECISION THERAPEUTICS SIGNS DEFINITIVE MERGER AGREEMENT WITH HELOMICS HOLDING CORPORATION

* PRECISION WILL INCREASE ITS EQUITY STAKE IN HELOMICS FROM 25% TO 100%

* PRECISION THERAPEUTICS(AIPT) – SHARES OF HELOMICS STOCK NOT HELD BY CO TO BE CONVERTED INTO RIGHT TO RECEIVE PROPORTIONATE SHARE OF 7.5 MILLION SHARES OF CO STOCK

* PRECISION THERAPEUTICS(AIPT) -DEAL CONDITIONED ON AT LEAST 75% OF HELOMICS’ $7.6 MILLION IN NOTES EXCHANGED FOR ADDITIONAL SHARES OF CO STOCK AT $1 PER SHARE

Bot a bunch more today only 15% above original buy point, what a steal.

I’m hopeful. I still would like to see some numbers on what Helomics is going to bring in revenues. I’m a little worried there is going to be another cash raise now that its closed and if so what price that gets done at.

Thanks Lane,

On money for Helomics: PRECISION THERAPEUTICS(AIPT) -DEAL CONDITIONED ON AT LEAST 75% OF HELOMICS’ $7.6 MILLION IN NOTES EXCHANGED FOR ADDITIONAL SHARES OF CO STOCK AT $1 PER SHARE

That indicates that another 5 million shares will be generated. And is maybe the one danger it will not happen, note holders will have to agree.

That said, they said on tape Helomics will be cashflow positive in 3Q, which starts Monday, rather mind boggling to me. Some people think Helomics already has $7-10 million rev rate. So $180 million invested in it, AIPT gets 75% (total 100%) for About 10 million shares, will have negligible debt afterwards and a $12, 15, 20?? million rev rate and cash flow positive in first new Q,

Then in 2019 Streamways goes cashflow positive with massive growth of about 1,000% per year on 2018. We get both of them for $20 million mkt cap and then throw in tumor growing sub and a company in super hot precision medicine sector with billion dollar+ buyouts of companies that are losing money.

That is why bot about 25,000 shares yesterday.

They now have 80 page report, great research, learned a lot from it. For one Streamways is a big money saver after 1st year, huge savings. Here is the report https://cdn2.hubspot.net/hubfs/150154/Presicion-Therapeutics-Executive-Informational-Overview%2007-09-18.pdf?__hssc=75734090.2.1531877212413&__hstc=75734090.72c69320b9deb0a85e65087ff7f3c1dd.1531877212413.1531877212413.1531877212413.1&__hsfp=613330879&hsCtaTracking=18cb02dd-2973-4026-b206-501fb097e460%7Cefe9ce5a-d162-4835-80f8-105cd52f9a83

Also in interview this week, CEO says likely news coming on multiple deals for Helomics, which is exactly what am expecting. How can they get Helomics positive cashflow this Q (they have said that) without some big deals. Looking great here.

Lane have you looked at ADMP?, they got their big partner, Novartis, for Epipen like product they have. Have bot in last week.

Cheers

AIPT in CC again said that in 3Q Helomics will cashflow. Guessing that might be $10 million annualized rev, they have fairly large staff. And they said 30-60 days likely for completion of deal.

Lane have you looked at ADMP? Like GCM have bot the falling knife in last week. They do have a deal with Novartis on their Epipen rival product.

Yeah I saw that we finally got a number for helomics – I think it was $3.5mm of revenues though I wondered if that was post-acquisition, or for the full year? Either way that helps. I might be wrong, but if I were to guess the lack of interest in the stock is just wariness of the deal closing (because of their history with getting the final deal done), and maybe a little disappointment about streamway sales. But I am hoping when the final deal is announced we get a big pop.

Has any body a rough idea how much dilution there will be?

They have a proxy with up to 50M.

Wrt the helomics merger I thought it said back in that June press release. It was like 19-20mm shares including the warrants if I am remembering right. Or are you talking about something else.

Ah, okay. So I read it correctly with 7.5M shares and 12.2M warrants.

Just wanted to make sure.

You know you’ll have to look at the 10Q – there is some numbers in there wrt the merger that don’t line up to me with the original PR. Appreciate your thoughts.

I think roughly Helomics deal will double pre Helomics share count, fully diluted 20 million. JMHO that is nothing in mkt cap for potential it has. If this company post Helomics deal was IPOed what would it go for ? $200 million mkt cap?

You know I honestly don’t the answer to that. What is Helomics worth? Is the market just discounting because they want to see the deal done? Are we all overestimating what Helomics is worth? It will sure be interesting to see how AIPT trades if/when they close the deal.

Yes, I expect a big bump and presume they will have a bunch of news at same time. In the last 2 Q CCs they have said Helomics cashflows positive is 3Q. Well it takes a bunch of news to make that happen, deals etc. So the quiet period will end and we will find out a lot more about Helomics, JMHO

My fingers are crossed for the same.

Still waiting for Helomics deal but have sold none of my AIPT.

In meantime got lucky on another, RNKLF RNX.TO, had some, then they found biggest nuggets in history, I tripled down at higher prices. It has 5 bagged in 2 weeks, and at my avg price have a 3 bagger already. Like AIPT think it can 50 bag.

Now 24,000oz in 10 days, richer than Comstock first bonanza.

I actually bought a little RNX too, after reviewing your comments on SeekingAlpha (I think it was you at least). Thanks for that!

Did you notice that in the 10Q for AIPT there is a paragraph about the Helomics transaction, and it seems to read as though there is more dilution because of the debt conversion than they had said in the earlier press release? I’m not sure what to make of it, because it also isn’t written very specifically and almost feels like it could be a typo. I tried to email management about it but didn’t get a response.

Thanks Lane, yes that would be me on SA, now my biggest position(RNKLF). Nothing but good news up to this point, it is making my whole year, which is not all that rare, 1 stock has done that before.

The AIPT merger is dragging out longer than expected, if you find out anything do let us know. They did get their first European sale on Streamways.

Just what I mentioned in an earlier comment about the share count.

Some good news, company emailed a shareholder than merger is doing fine, just paperwork holding it up, should be soon.

thanks for the update!

ceo carl keeps buying stock, any thoughts at this point?

I have seen that. When I read through the final merger documents back a couples months ago (??-I think) I remember being a little underwhelmed by helomics revenue and I still couldnt quite figure out how long before this is a sustainable cash generating business. Now that the market has turned maybe that isn’t as big of a deal as they can raise capital. I’m sure you know more than me about Helomics – what do you think? is the opportunity still there? Isn’t that CSBR a comp for them?