Radcom’s Growth is Lumpy (and that’s not a bad thing)

I had an interesting comment about Radcom the other day and given today’s release of fourth quarter earnings, it seemed like a good opportunity to expand on my reply.

First let’s talk about the fourth quarter results.

Revenue in the fourth quarter was $10.6 million. They turned a nice profit, about 17c per share. But the big news was announced on the conference call. A new Tier 1 one win:

We are very excited to share that one of these major NFV trials has come to fruition and resulted in RADCOM being selected by a Tier-1 multi-carrier operator. We expect this to result in a formal contract during the first half of 2018 and we’re making preparations for project execution.

Radcom also gave us some guidance for the first quarter and for 2018. They said first quarter revenues will be below the fourth quarter. And they said 2018 revenues will be $43 million to $47 million.

What to make of it?

Let’s go to the comment, which was made by Arf. Arf correctly pointed out that if Radcom grows by 25% in 2019 and 2020, after hitting the midpoint of guidance in 2018 ($45 million), then the upside is not as much as you’d think. He estimated the stock had maybe 70% upside if they got a 20x earnings multiple. This is in 2020 mind you. Given those assumptions, I think that’s probably fair.

So if that’s the upside, why bother with the stock?

My take is this. Because Radcom customers are large Tier 1 service providers, the deals are slow and sporadic but also unusually large compared to the existing revenue base. This combination makes it hard to anticipate the growth rate. Growth is going to be lumpy and its going to depend on the timing of when these deals are signed and when they begin to on-board.

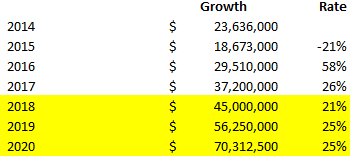

Let’s look at exactly what 25% growth rate is assuming:

So after growth of about $8 million in revenue in 2018, 25% growth adds another $11 million in 2019, and then $14 million in 2020.

That’s a possible outcome, but I don’t think it is an optimistic one. After the announcement today of the third Tier 1 win I would say it’s also less likely.

I’ve been looking at it like this. From the fourth quarter results released today, we know that total revenue for the year was $37.2 million and AT&T accounted for 60% of it. So the deal with AT&T was worth over $22 million in revenue in 2017.

I’ve always assumed that a full win on Tier 1 account should be for at least $15 million. Based on what we are seeing with AT&T, that assumption seems reasonable. It might even be low if Radcom can penetrate these other carriers to the same degree they have with AT&T (ie. sell them on the new visibility product that they will be unveiling at Mobile World Congress in a couple of weeks).

The Verizon foot in the door win was for $5 million. My bet is that eventually Verizon will grow to close the size of AT&T. Let’s say Verizon can be an $18 million win as the deal matures. Other large wins (with say a Telefonica or a Vodafone or a Bell Canada) should at least be $15 million.

With those numbers in mind consider this. A $19 million increase by 2019 ($8 million in 2018 and $11 million in 2019) is really saying that by 2019 Radcom will have successfully integrated Verizon to a similar level as AT&T and not much else. A $14 million increase in 2020 is saying that Radcom finally gets a single third carrier win by that point.

If it’s into 2020 and RDCM only has AT&T, Verizon and one more win, then something has gone horribly wrong with the thesis. Either NFV isn’t getting adopted or a competitor has caught up or something.

What do I want to see?

The difficulty this past year (and what led me to sell out of my position entirely for a couple of months) has been that the lumpiness of the wins has played against Radcom. They had no new wins that contributed to 2017 revenue. They were lucky to have a ramping business from AT&T that allowed for growth in the absence of new deals.

This handicap could become an asset over the next year. Because of the large, lumpy nature of their deals, even if Radcom gets just two wins per year for the next couple of years the company’s growth rate should go up substantially.

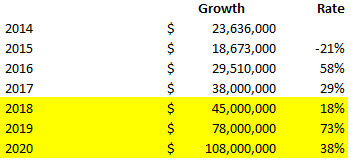

If I assume that Verizon is an $18 million deal in 2019, that the just announced Tier 1 is a $15 million deal in 2019 and that two more deals are announced in the next year and a half and begin to contribute meaningful revenue in 2020, I get a very different picture:

These numbers assume that by 2020 Radcom has 5 wins worth of revenue, ie. AT&T, Verizon, the announced win today and two others that will be announced in the next year and a half Its hardly more than one more win a year. In my opinion, this is not wildly optimistic.

So what’s with Guidance?

Any astute bear on Radcom is going to focus on the guidance. At first I was surprised it was as low as it was, given the Verizon win and the newly announced Tier 1. They did $37 million in 2017. The midpoint of guidance is $8 million higher.

But after thinking about it more, it makes some sense. We know the first phase of the Verizon deal is $5 million. We know this new Tier 1 deal is only getting signed in the first half, and even then in all likelihood it will be phased in similarly to the way Verizon was. So $2-3 million in the second half from the new Tier 1 is probably about right.

In other words, it looks to me like Radcom is guiding to known revenue only. They aren’t assuming anything incremental from AT&T. They are assuming no further expansion from Verizon this year. And they are assuming a slow ramp of the new Tier 1 in the second half.

I think they are setting themselves up for raises later in the year.

But I might be wrong. The other possibility is that guidance reflects an expected slow ramp of the NFV business for Verizon and other Tier 1. Given how slow it’s been for deals to materialize, this wouldn’t be that surprising.

It doesn’t matter (in my opinion)

Nevertheless, I don’t think it matters if this is a slow ramp or if it’s sandbagging. The only thing that matters here is whether I am wrong about these deals ramping to $15 million or more on an annual basis.

In fact with this latest Tier 1 win, deal size is the last leg for bears to stand on. They need to focus on the $5 million Verizon deal, assume that the deal won’t grow much more, and extrapolate that size to the other service provider trials.

Indeed if I am wrong and Verizon maxes out at $6 million or $8 million or this other Tier 1 maxes out at $5 million, then Radcom is going to struggle. But if these are $15 million plus deals, and because there is every indication that there will be more to come, then it’s just a matter of waiting until it plays out.

I just don’t buy the former scenario. It doesn’t make sense to me. These are large service providers. They are in the ballpark of AT&T and so the size of the deals should be in that ballpark when they are rolled out across the network.

What’s more, the revenue is recurring. A recent article in Light Reading clarified this for me. In particular:

Essentially, Radcom’s customers pay a constant, recurring and regular fee to use the vendor’s software, no matter how many instances they deploy and how many customers they are supporting with the software. So whether an operator is deploying Radcom’s probes in one market or ten, and supporting 50,000 customers or 5 million, the fee remains the same — the cost to the operator does not scale as it uses the software more. The traditional model of linking technology payments to boxes or instances or customer metrics doesn’t apply with Radcom.

I know I’ve been talking the Radcom story forever and I’ve been both very right and very wrong about it at various times. But unless someone can tell me why Verizon or Telefonica or Bell or any other Tier 1 wouldn’t have a deal size roughly comparable to AT&T, then I am going to say that right now things look as strong as I’ve seen them.

Therefore I am pretty excited about where Radcom is going. It’s my largest position right now. It’ll probably continue to be painfully slow, but the end goal seems clearer than ever.

Here are a few quotes from their annual report, which I found quite useful.

“Generally, the cost of the extended warranty is an annual

maintenance fee based on a percentage of the overall cost of the product.

Consequently, our first quarter orders are usually lower compared to the last quarter of the previous year, and often are the lowest of the year.

To protect our rights to our intellectual property, we rely upon a combination of trademarks, contractual rights, trade secret law, copyrights, non-disclosure agreements and technical measures…

we usually enter into non-disclosure and confidentiality agreements with our

employees, distributors, sales representatives and with suppliers and sub-contractors who have access to sensitive information”

Funnily, they also warn against the risk of being forced into the Israeli military.

thanks

Conceptually you could see this being a 1 or 2b company. High upside.

Do you have any idea about the pricing?

Like what differentiates a customer like AT&T from a small player? Is it really actually they same they charge? In the 10K they just mention, they sell fixed price contracts.

Pricing on the NFV product MaverIQ is not very well known. You can glean a few things from teh conference calls, like what Mike Arnold pointed out in a tweet to me earlier this week, and from the lightreading article. I suspect most of the info from the 20F is describing the pricing of the legacy product (name escapes me right now). When that 20F was released the only customer they had for MaverIQ was AT&T and even then I think the pricing model was pretty proprietary so I dont think much of the info in the 20F would apply to it. Just my thoughts.

Makes sense, what you say. I guess it comes down to how well they negotiate and I suspect there is something that scales with the network nodes or something like that.