Golden Star Resources: Betting against a history of disappointment

I have been slow getting to this write-up. My plan was to write about how Golden Star had drilled a number of holes that extended the depth of their Wassa underground by 180 meters, that this would add a lot of resource to the mine, and that it was not priced into the stock.

But Golden Star beat me to the punch with this news release Friday. The company announced that they had doubled the inferred resource at Wassa, adding 3.1 million ounces for a total of 5.2 million ounces.

The next step will be further infill drilling to upgrade the resource to measured and indicated, and a preliminary economic assessment of the extensions.

So that took some of the wind out of my sails. The near-term story I was going to tell was kind-of squashed. Nevertheless the big picture story is by no means finished. In fact I think Golden Star is just getting started along a path to credibility. I’m hopeful that the destination is growth, and a valuation in-line with other gold stocks.

History of Disappointment

Golden Star Resources has always been a very cheap gold stock. The problem has been that this was well-deserved.

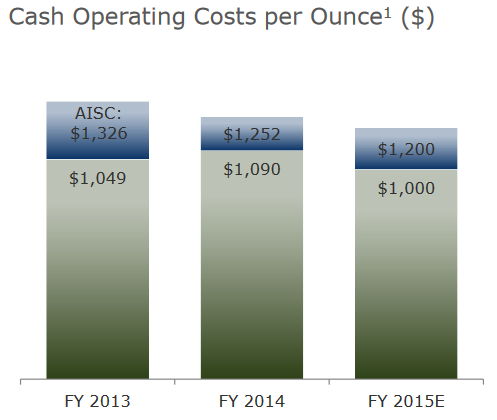

I’ve watched the company on and off for years. They have always been one of the highest cost producers. Cash costs typically exceeded $1,000/oz. This is what cash costs and all-in-sustaining costs (AISC) looked like from 2013 to 2015:

These kind of numbers made them bottom quartile in costs.

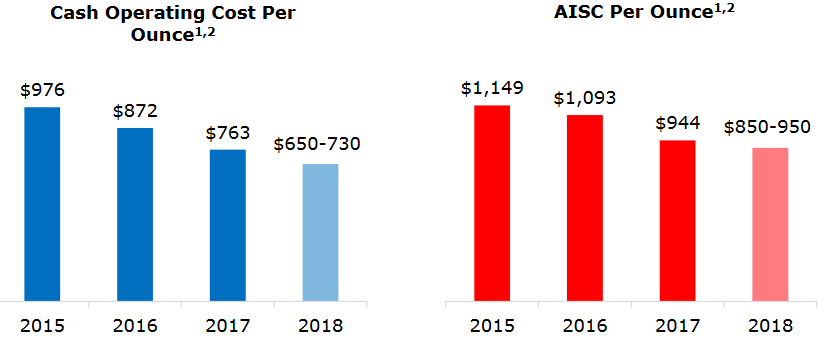

But that’s changing. In the last two years Golden Star has gotten their costs down. With the transition to underground operations at both of their mines (Wassa and Prestea), costs are expected to come down even more. ASIC in 2018 are expected to be between $850-$950/oz:

These new numbers don’t put Golden Star in the high cost bracket any more. They are in line with the majority of producers. Here is a brief list of other companies where estimates range from $850-$950/oz AISC or higher for 2018: Acacia Mining, Argonaut Gold , Detour Gold, Eldorado, IAMGold, Kirkland Lake, Klondex, Lea Gold, New Gold, OceanaGold, SEMAFO, Teranaga Gold, … you get the picture.

While costs are trending towards the average, the valuation has not. Golden Star trades at less than half the price to cash flow multiple as these other names. If you start to factor in the potential growth it looks even cheaper.

So why the disconnect?

I think its just years of disappointment. The market needs a lot of proof before they will re-rate the company.

Wassa and Prestea Underground

The bet here is that things are changing. Golden Star has two underground mines that are ramping up, a tonne of exploration prospects both within these mines and in the surrounding land base, and the capacity to grow production within their existing asset base using little additional capital.

Golden Star operates two mine complexes, Wassa and Prestea.

Both of these mines started off mainly mining open pit ore but are transitioning to underground. Wassa is ahead of Prestea, having begun underground production in early 2017. Wassa has been ramping up since and is performing well.

I think that one of the problems Golden Star has had is that reserves for both Wassa and Prestea underground are limited. Mineral reserves for Wassa are 742,000 ounces which they say is about a 5 year mine life. Similarly Prestea has reserves 463,000 ounces, which works out to a 5.5 year mine life.

I’m not sure why the reserves at these mines is so limited. Some of it is that underground mines often have smaller resources because drilling out too far ahead of the mining activities is expensive. Golden Star has been hanging on by a thread for years, so these were likely costs they chose to to incur. I also get the impression that there have been stability issues at Prestea that have only recently been corrected and allowed more drilling to take place.

While reserves are small, there is a much larger inferred resource for both mines. With Friday’s press release, the Wassa inferred resource is up to 5.5 million ounces. Prestea has 800,000 of measured and indicated and 868,000 ounces of inferred.

The small reserves and large inferred resource present an opportunity.

When you look at analyst estimates they, quite rightly, are basing their net asset value calculations primarily on known feasibility studies and preliminary economic assessments.

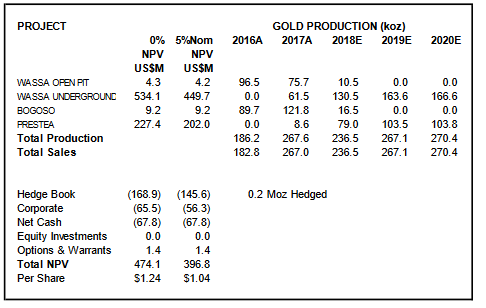

Take BMO for instance. They have an NAV5 for Golden Star of $1.04.

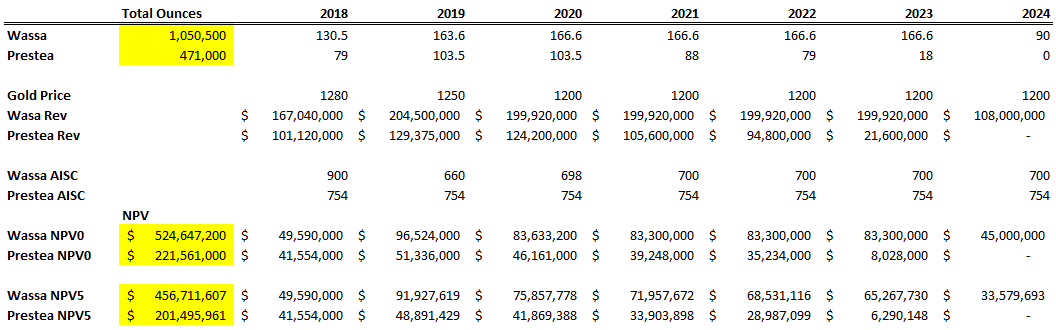

I can reverse engineer that number (like I’ve done below). To do so, I back-out total production from Wassa of a little over 1,000,000 ounces and 471,000 from Prestea (both the NAV0 and NAV5 match reasonably well, so I think I’m on the right track with these numbers).

Wassa has 5,000,000 inferred ounces. Prestea has 1,600,000 measured, indicated and inferred ounces. Very few (in the case of Wassa) to none (in the case of Prestea) of these ounces are included in the net asset value. The inclusion of these ounces, if the company can successfully prove them up, represents a lot of upside for the stock.

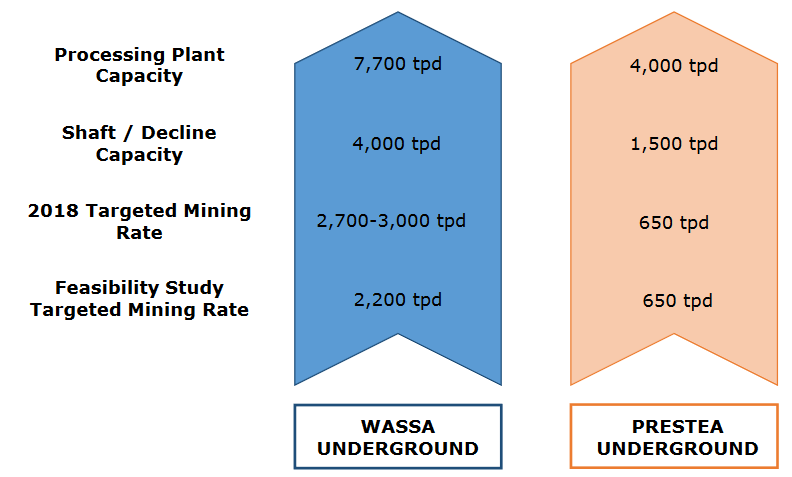

What’s more is that Golden Star can add significant production within its existing mining infrastructure. They have built their mine and milling capacity with expansion in mind. The mine at Wassa has capacity for 4,000 tpd while the mill can handle up to 7,000 tpd. At Prestea its even higher, with the mine at 1,500 tpd and the mill at 4,000 tpd.

Wassa could easily expand its mine rate by 30% before having to expand the shaft and decline. Prestea could more than double production before having to do so.

What this means is that if Golden Star is successful in turning inferred ounces into reserves, the cost of bringing those into production will be minimal. They should be able to ramp to double their current production without having to put out a lot of capital.

First Quarter Results

Golden Star provided first quarter production numbers on Wednesday night. Wassa exceeded the expectations of most analysts, producing 35,506 ounces at 4.54g/t grade. Grade had been an issue during the ramp of the underground at Wassa. In the third quarter grade averaged 2.6g/t, well below the 4g/t feasibility grade. The fourth quarter improvement to 4.04g/t, followed by this latest news is evidence that Wassa is on track.

The Prestea underground is earlier in the ramp. The mine just reached commercial production (defined as 60% of capacity) in February. They are having problems typical to a new start. In the first quarter they were only producing from a single stope, and the models of that stope were a little off the mark, which led to more dilution (lower grade). They say they’ve reviewed the stope model, figured out what was wrong with it, and expect better grades when they start mining a second stope in mid-April.

The second and third quarter numbers will have to be watched carefully for progress from Prestea.

Exploration

Apart from getting Prestea up to plan, the big news will be exploration results. The company is spending $6.6 million in 2018, split between Wassa, Prestea and new targets around the Prestea and Wassa complexes.

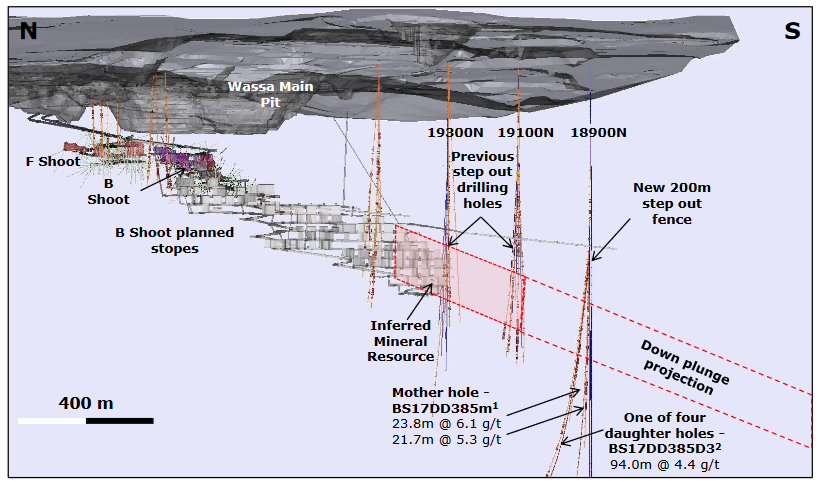

The drilling at Wassa will be focused on filling in the areas between existing drill holes. In the section below the pink area represents the original 2,000,000 ounce inferred resource. The step out to 18900N is where they drilled the extension that added another 3,000,000 ounces. You can see the large gaps that need to be filled to clean up the resource. Doing so will upgrade the inferred resource to measured and indicated and to reserves.

To facilitate drilling they have created an exploration drift extending from the mine to facilitate the drilling. I believe this is the line extending from the mine to the north just above the pink inferred resource box in the map above. Therefore the drilling meters planned at Wassa are a little deceiving, because they can drill a lot more holes from closer to the ore from this drift, so I expect them to accomplish a lot in those 11,000m they have planned.

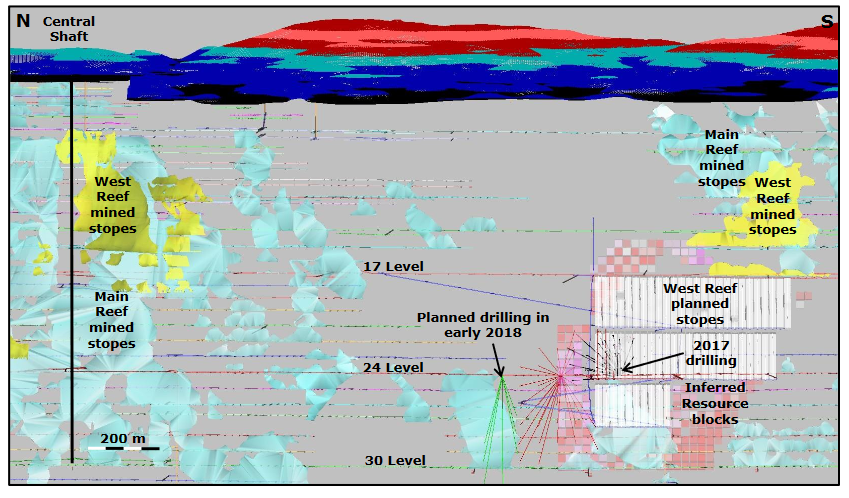

The opportunity at Prestea is a little less clear. Prestea is about a year behind and so the company is just now starting to evaluate how they might expand production in the coming years. Drilling this year will infill the existing inferred resource and more importantly focus down plunge on the West Reef (the green lines are the drill holes). Good results there will add new resource that could expand operations at the mine. Prestea is very high grade (14g/t or so) and the mill only operates at 600 tpd, so it doesn’t take a lot of new ore to add significantly to the mine.

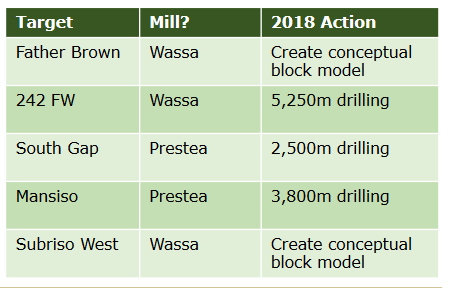

There are a few other exploration prospects that Golden Star will spend about $1.4 million on in 2018:

There are a few other exploration prospects that Golden Star will spend about $1.4 million on in 2018:

All of these are quite early stage and I don’t know much about them yet. The most advanced appear to be Father Brown and Subriso West, which have a combined inferred resource of 476,000 ounces. Father Brown has an underground grade of 6g/t which sounds promising.

Conclusion

Friday’s price action not withstanding, I’m not expecting an overnight success with Golden Star. It is more likely to be months of positive results that slowly build back the company’s reputation.

But I think that the outcome will be worth it. Especially if gold prices can stick to the current $1,300 level or move higher.

The BMO estimate I pointed to has an NPV5 of $1.04 USD on the stock. Even after Friday’s move, that’s a significant discount to the current price of 66c. That estimate is done at 2018 gold averaging $1,280, dropping to $1,200 in the long term. It includes minimal tonnage from Wassa and Prestea exploration. It includes no ramp of production to 4,000 tpd at Wassa or 1,500 tpd at Prestea. So there are lots of ways that number can move higher.

It’s a simple play. Cheap on comps, cheap on net asset value, a good chance to ramp significant growth over the next couple of years, and in a commodity environment that, in my opinion, is more likely to go up than down.

Interesting spec idea. Do you have time to talk tomorrow?

[cid:macnicol_a1f240f1-e259-41f9-a59f-5cbc1b6d3734.jpg]

David MacNicol President, Portfolio Manager MacNicol & Associates Asset Management Inc.

145 Adelaide Street West 3rd Floor Toronto, ON M5H 4E5 phone: (416) 367-3040 x 222 toll: (866)367-3040 fax: (877)215-4044 david.macnicol@macnicolasset.com http://www.macnicolasset.com

Hi – Thanks for the note, I sent you an email.

Nice write up again. What % of your portfolio is this stock?

And it seems your style is not betting on high conviction stocks, and selling as soon as the sky gets cloudy. Since you are pretty heavily in commodities, at what point would you start selling? Would you start lightening up on oil stocks let’s say 10-20% if oil would go down $10?

A lot of these commodity stocks look very cheap now, and the overall environment for commodity prices look good, but I am a bit scared of putting more than 10-15% of my portfolio in them.

I typically don’t put more than 3% in any of my positions to begin with. If they start working I might add. GSS is around 2%.

The one upside for Prestea is the massive tax loss carryfowards on this mine (my understanding around 500 million). Any further production will generate tax free income as far as the eye can see. Wassau on the other hand should start paying income taxes in 2019. Ghana mining tax law state that tax losses can only be used on each mine nor on a total company basis.

With regards to Largo resources, isn’t most of the upside priced in already? If we assume $20 Vanadium prices for the next 3 years (currently almost $16), with $5.5 pre tax and pre interest costs per pound (given that cash costs are about $4). And 12k tons production per year. And $1 goes to Glencore. and a 1.27x exchange rate.

That would be CAD$316m in after tax profit with a 30% tax rate. But with marginal cost producers at $12, it seems that this is not something that will last long? Given that IRR’s must be huge for everyone at $20 vanadium prices? So a 2-4 year period with $20 average Vanadium seems like a reasonable estimate? Given that historically prices that far above marginal costs trigger a wave of new supply that takes several years to come online.

Then I model a $15 Vanadium price for another year, and an average of $12 for the 6 years after that.

If I add it up over 10 years, I get a little under $2 billion Canadian undiscounted. With a discount rate of about 12%, there isn’t that much upside to be had here (unless you do technical analysis, or something like that). Given that the market cap fully diluted is about $1.2 billion.

Don’t want to sound like a sourpuss hating on your stock picks btw, I made a neat profit here thanks to you 🙂 . Just seems like selling is usually a more tricky decision than buying.

I sold LGO, I tweeted about that a while ago.

Did you sell Aveda after the merge with Daseke?

No I’m holding it because of the contingent value