Week 354: Winners and Losers

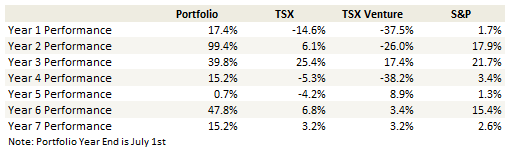

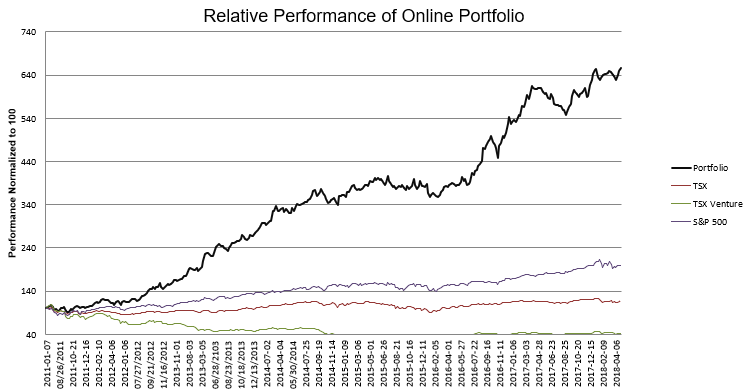

Portfolio Performance

Thoughts and Review

My method of investing generates a lot of losers. I think it’s a pretty good bet that over 50% of the stocks I pick for my portfolio lose money.

My performance is generated primarily by a few winners that end up being big winners. When I went through a slump in late 2015 – early 2016 I pointed out how few multi-baggers I had. I was generating lots of losers of course, but I didn’t see that as a problem. The problem was that the winners weren’t winning enough. For my method to work, I need at least 2-3 stocks a year that go up 2-5 times.

The math on that works in my favor. If I have 2 stocks a year that make up 4% of my portfolio each (I usually start out at 2-3% positions but add as they go up) and they go up 3x then my portfolio gains 24% from those positions. If they double then I gain 16%. If I can manage the rest of the portfolio to limit the damage; sell the losers before they get too destructive and have a few other smaller wins to help offset the losses, then overall I’ll do okay.

Anyways, that’s my plan. Its why I invest in a lot of businesses with high upside but questionable paths to achieve that upside. I’m fine with those that don’t pan out, as long as a few of them do.

Since last summer my big(gish) winners (this is off the top of my head) were: Combimatrix, R1 RCM, Gran Colombia, Aveda Transportation, Vicor, Helios and Matheson and Overstock.

Combimatrix was taken over and ended up being between a 2-3 bagger. R1 RCM was a triple. Gran Colombia is almost a double so far from my original purchase at $1.40. Aveda Transportation got taken over a couple weeks ago and was nearly a double. Helios and Matheson was a little less than a triple (I sold out well before the top, in the $9-$10 range) and Overstock was about a 70% gain.

Both Helios and Matheson and Overstock turned out to be flops in the end, but that’s okay too. A big part of my strategy is to know what I’m getting into, and not fall in love with it because there is a good chance it ends up going south. In both those cases I was pretty cognizant of the company’s faults, and I freely admitted there was a lot of uncertainty with both. As the faults materialized, or as too much optimism was priced in, I reduced my position in each and eventually sold out.

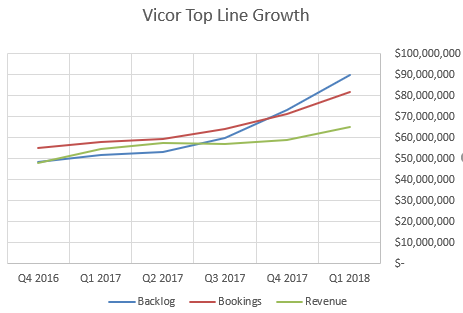

Vicor Results

I had been going through a drought in the new year before I finally got the move I had been waiting years (literally years!) for with Vicor. Finally the rest of the tech-world is catching up with Vicor’s 48V converter technology. Applications are popping up all over. There are the 48V servers, which were the original reason I got into the stock, but also low voltage GPUs (from Nvidia and AMD) requiring power on package, new areas like electric vehicles and AI, and most recently the evolution of a reverse 12V to 48V datacenter application. All these customers seem willing to pay for Vicor’s superior and patented technology.

I looked at Vicor way back in March of last year and worked out the numbers on an optimistic trajectory for the company. At the time I pointed out that while the stock didn’t appear cheap on most metrics (it had no earnings and was at a fairly high P/S ratio given the lack of growth), if they could follow through on their growth plan, the earnings they could generate were pretty impressive.

I updated that model recently based on new projections and the fact that after the first $100 million of earnings Vicor is going to have to start paying taxes (they have about $34 million of valuation allowances right now).

It looks to me like a $450 million of revenue run rate gives Vicor about $2.10 EPS when fully taxed.

The first quarter numbers were strong. Bookings and backlog have been outgrowing revenue. Backlog grew 23% sequentially. Bookings grew 15% sequentially. Revenue grew 11% sequentially.

After the first quarter numbers its looking more like that first $450 million of revenue could happen sooner than you think. $450 million is roughly what Vicor can do in their current facility.

Vicor is expecting to double capacity with a second facility later this year. If you assume that Patrizio (Vicor’s CEO) hasn’t gone off the deep end and that they can fill that second facility, the earnings numbers get much higher. Given that right now they are growing at 10% sequentially and that is before the larger orders that are expected in the third quarter start hitting.

I am inclined to hold the stock with the view that we are just getting started.

What I did in the Last 5 weeks

As I said I will always have a lot of losers. An important part of the strategy is to sell that which I perceive as not working out.

In the last month I did more selling than buying. This is partly due to broken theses but also because I remain cautious about the market. But to be honest, this caution has hurt me more than it’s helped.

Much of my selling has been poorly timed. For example, I sold Largo Resources at 1.30, only a couple of days before the stock made a run up to $1.90. I’ve written about the Largo story before: Largo is a great theme play on vanadium but it has always been hard to make the stock look cheap by the numbers. That has nagged at me and it finally won out. I took a nice gain on Largo, having bought it at 80-90c, but it still hurt to watch the stock subsequently take off.

I also sold Aehr Test Systems shortly before it ran from $2.20 to $2.60. With Aehr I took a loss. I’m still not sure whether I did the right thing selling it. On the one hand it feels late in a semi-equipment cycle, and the company has had very few announcements of new contracts lately. On the other hand it appears their relationships with Intel and Apple are intact and so the next big deal could happen at any time. It’s a tough stock to judge.

I also had poor timing with Essential Energy, which I sold at 55c range after listening to their fourth quarter conference call. The call painted a depressing picture of drilling in Western Canada. I didn’t get the sense they had any pricing power and the year over year utilization rate appeared to be flat. Now maybe that has changed as oil has risen another $10 since I sold. As well, the lawsuit with Packers Plus is in appeal (so its still not settled), which means a takeover is unlikely. I decided to focus instead on US leaning servicing companies like Aveda Transportation (which subsequently got taken over for a double, though it was a modest position for me) and Cathedral Energy Services, which I continue to hold.

I had somewhat better timing with my exit of Sherritt International, as the stock sank after I sold. But even the jury is still out as the share price has come back with nickel skyrocketing.

I likewise sold my position in both Orocobre and Albemarle. This fits into the “loser thesis” even though I made small profit on Orocobre. My thesis was that the consensus for lithium had under-estimated demand and over-estimated supply. However, the more I’ve learned about the supply/demand dynamic the less sure I am. It’s not so much that I’m a believer in the coming lithium supply tsunami. It’s just that I’m unsure enough to not want to make the bet either way. I’ll revisit these names again, especially Orocobre, but I need to study lithium some more and make sure I’m not wrong about it.

I also exited my position in Foresight Autonomous. I mentioned the stock last month and its just not working. They are going to need capital at some point and the recent death that was at the hands of an autonomous car isn’t helping. But probably my biggest reason for the turnaround is that this just doesn’t seem like a good market to be holding many nano-caps in.

Finally I reduced my DropCar position (which is heavily in the red) by about 20%. I probably should have reduced this stock earlier, but it was a tiny position to begin with (~1%) and so I’ve been more willing than maybe I should have been to give it some leeway. I still think they could pull off some big growth but the revisions of their option strikes, the share offerings and the lack of news has worn me down. Being down 40% on the position means at this point it so small that its a bit of a lottery ticket. Which is really what it always was.

Gold and Oil

What’s been working for me are my gold and energy stocks. Those that follow the blog know that I’ve been holding a number of gold and energy stocks for months now and that number has been increasing. Up until recently they have done nothing.

I wrote up my reasons for owning Golden Star Resources a few weeks ago.

I also continue to hold Gran Colombia Gold. I admit that I am a little nervous about selling pressure in the near term. I don’t totally understand what the short term outcome of the 2018 debenture conversions will be and whether sellers of those debentures will pressure the stock over the next while. Nevertheless, I think the company is on track for a re-rating at some point and I’m happy to wait out the weakness.

I also have positions in Jaguar Mining, RoxGold and Wesdome.

The idea with these stocks isn’t really about gold prices. I don’t feel like I am making a bet on whether gold will imminently go through the roof. I feel like I’m just buying stocks that are really cheap.

All the miners I mentioned above have EV/EBITDA ratio of between 2x and 5x. Those multiples are trailing ratios that are based on lower gold prices then what we have now. Each of the miners has good growth prospects and an exploration upside if drilling comes up positive. Apart from Gran Colombia, they are all well off their 52 weeks highs.

I also recently took a small position in Asanko Gold. The stock has been written up a number of times on the IKN blog. Gold Fields recently did a deal with Asanko, taking 50% of their property in return for enough cash to pay out their debt. Otto Rock, who writes on IKN, thinks Asanko should trade back to at least 1x book value now that Gold Fields is available to provide their expertise and hopefully right the ship at the Asanko Gold mine.

So if the gold price breaks out, that’s an added bonus. But these stocks are more of a play on sentiment. I think all I really need on the commodity side is for gold not to crash.

I don’t really have a crystal ball with what gold will do. I will note that the chorus of the gold bears on twitter seems very loud right now. “It didn’t go up with North Korea”, “It can’t break $1,360”, “It’s setting up a technically bearish formation (a compound fulcrum top?)”, “The Australian dollar, the Canadian dollar are canaries in the coal mine that the rally isn’t real”, and so on.

Who knows? Maybe they will be right this time.

I have been reading about the 70s, and in particular what Nixon did that led up to the Smithsonian agreement. The circumstances today are different of course, but not so different, and I was surprised how much of what Nixon did rang true to what Trump is doing now.

Nevertheless, I own tiny companies that are not in the GDX or GDXJ, typically don’t follow gold prices all that closely (Golden Star went down nearly 40% during the last gold rally!), and have unique attributes that I believe will lead to price appreciation. Gran Colombia, which is up 90% since I bought it last summer, is the poster child for this.

On the oil side I have all my old names: Gear Energy, Spartan Oil and Gas (which got taken over so now I effectively hold Vermillion shares), Zargon Oil and Gas, and InPlay Oil and Gas. I also bought WhiteCap as another way to play the run.

On the US side I continue to hold SilverBow and Blue Ridge Mountain. I also added Extraction Oil and Gas, which looks to be generating a lot of free cash in the coming years at these prices. I’ll write something up on them shortly.

The summary of what I have read on oil is that things are potentially tighter than we realize, that they are getting tighter, and that relying on a small patch of west Texas to supply the world’s growth is likely not the best strategy.

I’ve been surprised by the strength in the oil stocks. They seem to go up every day, and a lot of days they start down big and recover throughout the day. It’s hard to see that as bearish. I’ve read about the big net long positions, and I suppose that means we get a correction here at some point soon. But I’ve held these stocks for this long, I might as well see it through.

New Purchase: Ideal Power

The one stock I bought that I will mention in some detail is Ideal Power. This is the perfect example of a high risk, tiny little micro-cap that has a chance (maybe not a big chance but a chance) of being a 5-10 bagger.

Ideal Power sells inverters into the solar industry. One of their inverter products, called the Sundial, has been built into a Flex solar plus storage offering called NX Flow. NX Flow, interestingly enough, uses a vanadium battery.

Flex initially had huge expectations for NX Flow. Leading up to the product launch in December, Flex was saying they could sell 15MW per week of their product.

Now if you do the math on 15 MW per week, considering that Ideal Power sells their Sundial for about $10,000 per unit, that there is one Sundial per 30 KW capacity, you get a very, very big revenue number.

The reason the stock is at a buck and change is that those sales forecasts haven’t materialized. Maybe they never will. Flex is trying to “educate” their customers on the vanadium battery. The real benefit of a vanadium battery compared to its lithium-ion competitor is that the vanadium battery doesn’t degrade over time. The life span can be significantly longer and performance doesn’t suffer. The problem is that customers are used to buying a battery strictly on a per MW basis. On that metric alone the vanadium alternative appears more expensive.

Nevertheless Flex is a big company and I don’t believe they just pulled these numbers out of their ass. I feel like it’s worth a bet that the NX Flow begins to get some traction.

The stock has one other lottery ticket in its back pocket. Ideal Power has developed an alternative switch for converting between DC and AC power called a B-Tran device. Pretty much every inverter out there has some combination of IGBTs, MOSFETs and diodes that let you switch power back and forth from AC to DC and vice versa. The B-Tran can do this too, and it can do it while reducing losses to 1/10th of what an existing IGBT solution will have. The double-sided nature of the device means that you can replace two IGBT’s or MOSFETs, and two diodes with a single B-Tran. So there is a cost savings.

The company just finished prototyping the device using their anticipated manufacturing process and it appears to work as advertised. The power semi-conductor market is $10 billion and the company has said that if all goes well B-Tran could address 50% of that.

Look I have no idea if this concept flies. It seems to have some merit based on what I’ve read from various electrical sites and papers but its very technical, there is incumbency at play, lots of factors will determine the success. My main point is if you are going to throw a hail Mary you might as well go for the end zone and that is exactly what this is.

The stock has a $20 million market cap and $12 million of cash, which they are burning as we speak. I could easily see myself selling this stock at 80c in 6 months time. In fact, that’s probably the base case. But the bull case is so big that I believe its worth the risk.

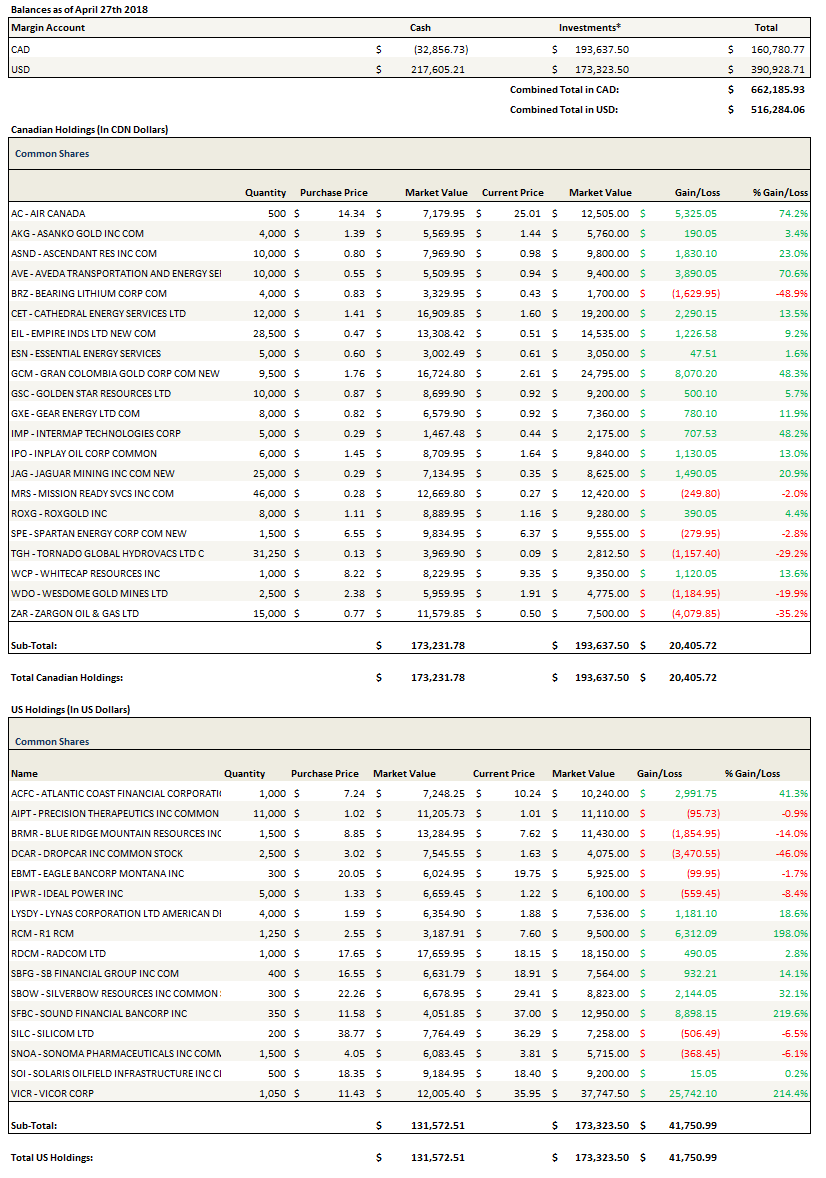

Portfolio Composition

Click here for the last five weeks of trades.

{kind=link}

I liked this short write up on lithium:

https://www.valueinvestorsclub.com/idea/SOC_QUIMICA_Y_MINERA_DE_CHI/141796

With regards to Gran colombia, it seems Lloyd miller has passed away earlier this year, and they are liquidating all his holdings, so that might be an overhang? I have seen this with a few other Lloyd miller holdings as well.

Thanks, I didn’t know that about Lloyd Miller. I dont have a membership to VIC so I can’t access that unfortunately.

You can sign up a free account and then you can read ideas posted 45 days ago. Otherwhise only ideas posted 90 days ago or more.

Lloyd Miller only owned the GCM.DB.V so his estate will be cashed out on May 14 when the remaining GCM.DB.V and GCM.DB.X are redeemed.

Hi,

Iâve been reading your post for some time now and would like to have an opportunity to connect with you to discuss the two companies I run:

Kintavar Exploration â KTR.V â a recent major copper discovery in Quebec. Stratiform copper deposit. We are doing a $15M financing at the moment with a large portion coming from the Quebec institutional side.

Geomega Resources â GMA.V â a rare earth exploration company that I converted into a technology company working on recycling with the magnet industry before we apply our tech to the mining industry. Safer approach than running through the mine first.

What would be the best way to connect with you for a call.

Regards,

Kiril Mugerman

President and CEO

75 Boulevard de Mortagne

Boucherville, QC, J4B 6Y4

T. +1 450-641-5119 #5653

âThis email may contain forward-looking statements which are based on various assumptions and estimates and involves a number of risks and uncertainties. Readers should not place undue reliance on forward-looking statements. The company expressly disclaims any obligation to update any forward- looking statements, except as required by applicable securities laws.â

What is your take on tear up of Iran deal? In my opinion, conflict increasing in the middle east seems extremely likely. And several 100k barrels of oil supply dissappearing as well.

This makes it much more likely that Iran can only be stopped from getting a nuke by using military force, as a new deal is extremely unlikely now.

It seems the oil market full priced this in already. I was expecting oil to jump at least $2-3 after this news. Time to load up on more levered oil stocks? But maybe I am missing something here.

I have to do some more reading on Iran. I’m not sure what is priced into oil here. There are still a lot of bears out there saying this is all geopolitical but with the lack of investment, difficulty getting pipelines built, gassier permian, etc I really don’t know, I prefer to err on the side that says oil goes higher than expectations. But I’m an eternal oil bull so take it with a grain of salt.