Catching the knife with Gran Colombia

This has been just a brutal week for my portfolio. I have been sliced and diced by the commodity bear market.

I was prudent enough to exit all of my base metal positions and that saved me through the early part of July. But this week oil stocks and gold stocks joined in the carnage and I was not well positioned for that.

I admitted defeat on a few of my oil stocks. I sold Zargon, reduced Gear Energy and reduced GeoPark. I don’t have the conviction. The second quarter has not shown the inventory draws that I had anticipated. I’m worried about what happens as inventory builds begin. What if Saudi Arabia decides to direct more oil towards the US? Even if overall supply remains constant, the market seems to react with blinders to the weekly US storage numbers.

On the other hand I have held onto my gold stocks. Until this week they had been holding up pretty well even as gold fell. I even had a big winner in Wesdome and a little winner in Golden Star Resources. But this week the bottom fell out of all of them, in particular Roxgold, Gran Colombia, Jaguar and Golden Star got creamed. I sold a bunch of Jaguar because it just isn’t operating well but have kept the rest.

The irony of Roxgold, Golden Star and Gran Colombia is that each released second quarter results and they were really quite good. But the market doesn’t care much about results when it is busy panicking.

I’m going to focus on Gran Colombia right now because that stock has gotten into the “this is pretty insane” territory in my opinion.

Gran Colombia Second Quarter

Gran Colombia released second quarter results on Tuesday. Since that time the stock has fallen almost 20%.

When a stock falls 20% in the days immediately following earnings you would expect to see an earnings miss, a reduction in guidance or an increase in costs. Here is what Gran Colombia gave us:

- Raised production guidance to above 200,000 ounces for the year from previous guidance of between 182,000 and 193,000 ounces.

- Produced 52,906 ounces of gold in the second quarter up 15% year over year

- Total cash costs and all-in sustaining averaged $696 per ounce and $913 per ounce, well below the company’s guidance of $735 per ounce and $950 per ounce

If there is a negative side to the results, its that costs were up a little over the first quarter and earnings were down a little, mainly because the price of gold was a bit lower. But the company’s measure of free cash flow was up to $11.4 million USD for the second quarter, up from a little over $2 million the previous quarter.

Anyways those are the results. Next let’s consider the valuation of Gran Colombia.

We can look at the stock two ways. Either using the current share count and debt levels, or assuming that the warrants get converted, increasing the share count but also increasing cash on hand. Because the current share price is below the warrant strike, I am not including the warrants in the calculations below.

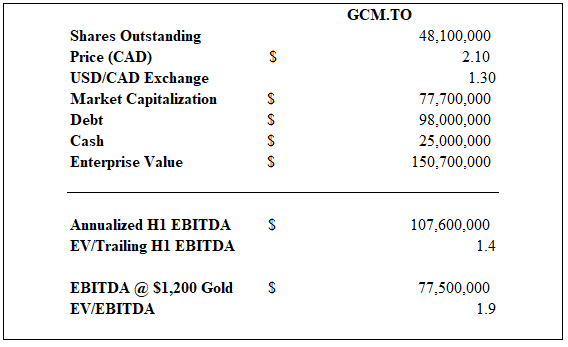

After full conversion of Gran Colombia’s 2018 debentures (which happened on August 13th), the company had 48.2 million shares outstanding. So at the current price the market capitalization is $100 million CDN or $78 million USD.

Gran Colombia has $98 million USD of senior Gold notes and $25 million USD of cash. Net debt is $73 million USD. EBITDA last quarter was $26.5 million. EBITDA in the first quarter was $27.3 million. Below is what the company is trading at currently if you annualize first half EBITDA as well as what it’s at based on my estimated EBITDA at $1,200 gold.

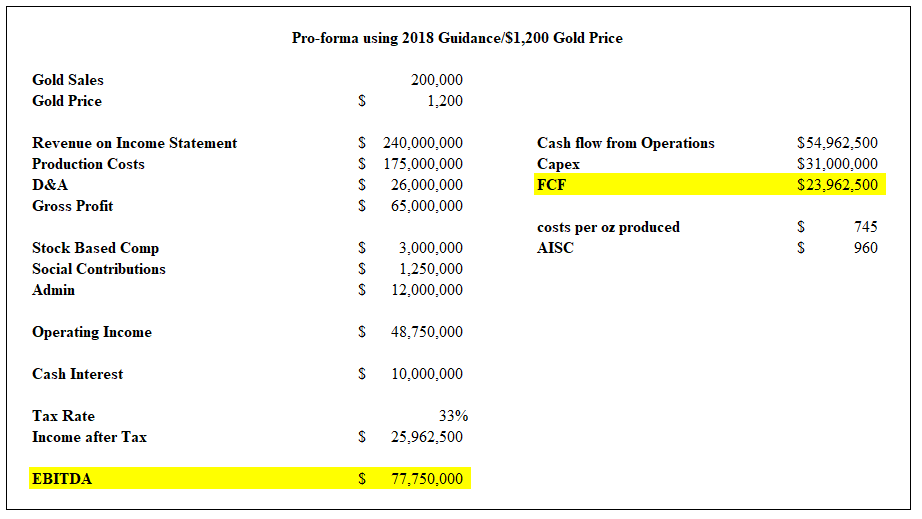

Below I have tried to work out a simple pro-forma model of what EBITDA and free cash look like at $1,200 gold. I’m using the company’s own production and cost guidance. They have been consistently beating the cost guidance and are trending above the new production guidance in the first half. I’m also assuming the tax rate for 2019.

So the stock is trading at a little over 3x free cash flow using the company’s own guidance. That seems a little crazy to me. I’ve added to my position here and am hoping the carnage ends soon.

It is crazy cheap, I own as well. Though what is the company worth? $4-5? Always struggle with that with miners.

Here is a good bearish piece on gold (his other posts are also worth reading imo):

https://lt3000.blogspot.com/2018/05/golds-hidden-risk.html?m=1

Thanks that’s an interesting perspective. But it does kind of feel like a spin. Cuz it’s essentially saying that if investors say that gold is worthless then gold is worthless right? It’s another way of framing the

Whoops got cut off – of framing the “gold is not a currency” argument I think. I mean if investors and central banks decide that gold is not a currency alternative then yeah, gold is probably worth a lot less.

I kind of feel the opposite. That we are entering a period with tariffs and protectionism that should lead to something like Rickards currency wars, at least in spirit if not in degree. And in that environment I’d think you’d see more demand for investment/central banks for gold, not less.

But it hasn’t worked that way yet and gold actually seems to be acting completely contrary to that right now which I don’t understand.

No I think it means that ratio of the amount of gold that is sitting there above ground vs annual gold demand is huge. So some variance in what investors decide to do could easily crater the gold market. There isn’t really any other major commodity that has this dynamic. If for various reasons a bunch of institutions and governments decide to lighten up on gold at the same time, it could send gold well below $1000 for several years.

But that logic works both ways of course. So I think all these stocks, no matter how cheap, should be seen as long term call options. That is why I struggle to come up with a fair value multiple for GCM.

Ok I see. I’ll have to think about it because something seems off about that idea to me. If that were really the right way to look at it then wouldn’t gold be way more volatile then other commodities? Like if you had even the smallest shift in investor perception working off such a large base then you should see a huge change in price right?

Yeah that is a good point. I suppose that is since governments rarely sell. So then the base is much smaller.

I think historically inflation was mostly created by debt creation, and not really by money printing by central banks. Japan has been a net seller of gold I think. When private debt reaches a certain % of GDP, and GDP growth is low, gold buying eases. But with China, India, Africa and Southeast Asia still booming and having low private debt to GDP, I would say that is not much of a risk either.

Hi Lane, we mirror each other so much it is uncanny. I added 35% to my GCM position is last week, and have sold over 50% of miners had in last 3 months.

Totally agree with your assessment, but good to see your number analysis from scratch. It’s about 1 x EBITDA right now, insane.

JMHO is that people got used to the old price of a share when they had huge net debt and have not adjusted to the fact net debt is now good not terrible. Another thing like about GCM, their execution in last 3 years is amazing, best of any miner know of.

They could be paying a 20% div based on today price in 1-2 years. Cheers

What is normalized capex like when they stop growing (as much)? What are you taking for depreciation? And does the debt allow for stock buybacks?

Thanks for the question. My CAPEX estimate is embedded in the FCF number I provided. I am assuming $31mm annually, which is a little more than it has been TTM (I think it was a little over $30mm). You could argue I should use $36mm, which would be what it would be if you annualized the last couple of quarters, but reading through the CC it seems like a lot of expenditures in the first half were things that won’t have to be repeated. But I might be wrong.

If you go back to 2016-17 the capex is less than $5 million a quarter a lot of the time. So maybe the run rate is going to come down going forward? But hard to say without more guidance.

Depreciation isn’t included in any of my calcs because I am dealing with FCF and EBITDA. I don’t find depreciation all that useful for mining companies. Just in general, it doesn’t necessarily follows expenditures for most miners in the short run.

I had someone make a comment about using EBITDA so I want to expand on why I used that here. I used EBITDA and FCF. EBITDA because its A. simple, B. restricted to operating performance (but with the caveat that its not going to include capex) and C. easily found in the brokerage reports for comps. I could look at operating cash flow and at sometimes I do, but then I’m not necessarily getting a picture of the operating performance, I’m getting a picture of the operating performance as its impacted by the financial side (interest expense, taxes, changes in inventory).

FCF gets me further of course, takes into account the financial costs, taxes and capex. FCF is the best metric but it moves so wildly from quarter to quarter its not always easy to peg down so EBITDA gives a bit more normalized metric, which is especially useful for comps. EBITDA is also useful because all the brokerages I have access to use it so its easy to compare a company like GCM that isn’t covered with all the covered peers.

As for buybacks, that’s a good question. I don’t see anything in the terms that restricts buybacks but I can’t say for sure. I’ll maybe send the company an email and ask them.

thanks, wondering how you think about their reserves? I’m seeing 660k oz of proven & probable (and that’s like 90% “probable”) Given they’re producing 200k oz a year, that covers > 3 yrs of production, making <2x EBITDA cheap but not absurdly cheap (considering it's not "proven")

On the other hand if you use "measured and indicated" then you have over 5mm oz, making this dirt cheap.

Maybe. It is an underground mine though, and those often seem to have lower reserves because of the costs associated with delineated drilling before you’ve brought the ramp down close to that level. FWIW Segovia had 0oz of reserves in 2016. Those numbers you are quoting aren’t quite right I don’t think. The 660koz is but I think the resource for Segovia is 1.1moz M&I and 980moz inferred. That was when the study was done in Q2 2017.

thanks!

Maybe worth reviewing this for the discussion here

Click to access musing-080825-Reserves-and-Resources-A-Primer-for-the-Lay-Investor.pdf

What’s the deal with management at Gran Colombia? I read the PR about their recent equity issuance to satisfy the converts, and they sure don’t sound owner-minded (they say that the stock is undervalued, so they are happy to issue new shares and increase liquidity). Blech

I would recommend looking a bit more closely at what they did and what dilution would have been if all legacy debentures were converted. They created a simpler structure and the dilution is far less than it might have been.

I see, they were indeed digging themselves out of a deep hole. Seems interesting, I picked up a starter position this morning.

Yeah they were. The capital structure used to be extremely complicated, with 3 sets of debentures and two sets of conversion criteria. Now its pretty straight forward. You have the shares outstanding, the notes, and the warrants (which are out of the money right now).

What do you feel is a fair EV/EBITDA valuation? 4x?

Hang in there, got nicked in some small commodity names in Canada myself, not these but CMMC, CS, TKO and oil names. I enjoy your writing. Jonathan

Isn’t fully diluted shares outstanding more like 63 million when you include all warrants and options etc? Look at latest presentation.

Those warrants were out of the money when I wrote the article (still are sightly out of the money right now) so I didn’t include them or the cash they would bring in.