Buying into US Cannabis legalization with C21 Investments

I missed out on the rise of Canadian cannabis stocks. It was my own fault. I didn’t do the research, didn’t really understand the valuations, and the stocks moved so fast that I was always scared I would be catching the top.

But it made me watchful. When I saw companies listing on the junior Canadian exchanges with expanding operations in the US I was immediately interested.

I was introduced to C21 Investments (CXXI) by a friend who mentioned it to me when it was doing a private placement back in March.

The stock started trading in June. I’ve been watching it since. It started off above $2 and traded almost to $3 at one point before recently collapsing back to a little over a $1. It’s been crazy volatile.

My guess is that the move down has been precipitated by anticipation and the subsequent end of the lock-up period of the March private placement, which ended on July 27th. There are also probably sellers from the reverse takeover shell (called Curlew Lake) that C21 inherited.

C21 raised $33 million in March through the issue of 33 million shares. The price was $1, which is not far off from where we are now. They raised another $5 million in July at much higher prices.

I’ve taken a position at this level.

Why am I buying?

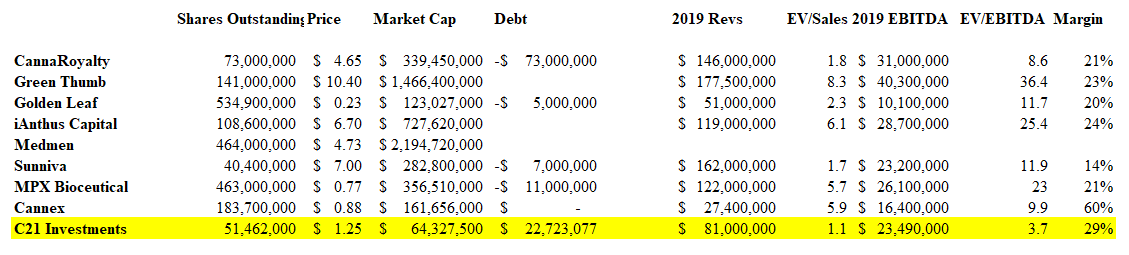

Well the first reason is that it looks pretty cheap compared to its peers.

Before I give that peer comparison, let me give this caveat. The one conclusion that I’ve drawn in researching the US cannabis sector that there are a lot of projections, but not a lot of operating history. This goes for C21 as well as every other cannabis company on my list. This is a reason to be at least somewhat cautious with all of these names.

There are two reasons for the lack of history:

- Apart from a few small states (Oregon, Washington and Colorado), recreational cannabis has only been legalized in most states recently

- Most these names have gone public in the last year to raise capital and consolidate existing, smaller businesses that were previously private and that therefore did not report publicly

C21 is no different. They have made 6 major acquisitions. All those acquisitions were done in the last 6 or so months. While the company has actually provided more trailing revenue numbers then most, a valuation still has to be based on their future projections for these businesses.

Below is a comparison using 2019 projections for each company. For the other companies in the list I’ve found brokerage coverage (in most cases Canaccord but also GMP and Beacon Securities) for the revenue and EBITDA estimates. C21 is my own estimate which is primarily based off of the company’s own projections.

I’ll get into how I came up with the market capitalization, enterprise value, revenue and EBITDA estimates for C21 shortly, but first let’s talk a bit about the US cannabis market.

US Cannabis Market

The US Cannabis business is a different beast than Canada. US cannabis is legal at the state level but not the federal level. This means that you can’t have an operation across multiple states or if you do, each needs to be separate, as cannabis cannot cross state lines.

It makes the business inefficient, but it also provides the opportunity for small players. The lack of federal legalization keeps larger players from entering the business. There is still the threat (though this might be receding with soon to come legislation) that company management could go to jail for selling something that is a crime federally.

Each state is an island, with their own laws, their own implementation and probably most importantly, their own licensing structure.

Therefore, it’s important to evaluate the specific states that a US cannabis company is operating in.

C21 is operating in two states: Nevada and Oregon.

These two markets could not be more different from each other.

C21 has made 6 investments in Oregon and another in Nevada. But the Nevada acquisition is larger then all the Oregon investments combined, and probably the bigger generator of value in the short term, so lets talk about that one first.

Cannabis in Nevada

Nevada passed the legalization of cannabis as part of a referendum on the 2016 election ballot. Recreational sales began in July 2017.

Nevada is not the largest state to legalize cannabis. That honor goes to California.

However, Nevada has a significant number of tourists visit the state. There are over 40 million tourists a year that come to Nevada. So, the market is much larger than the population implies.

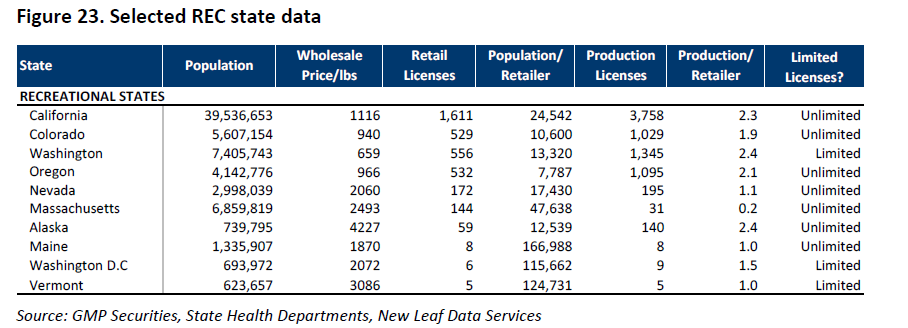

Nevada, like other states that have only recently legalized cannabis, has been more cautious in their licensing approach than earlier adopters such as Oregon, Washington and Colorado. These early adopting states flooded the market with licenses. The table below compares licenses per population for various states.

Nevada looks middle of the pack, but after considering the much high tourism, the licensing looks conservative. The consequence is that Nevada is considered by many to have one of the best potential cannabis markets.

The limited number of licenses have kept wholesale prices at reasonable level so far.

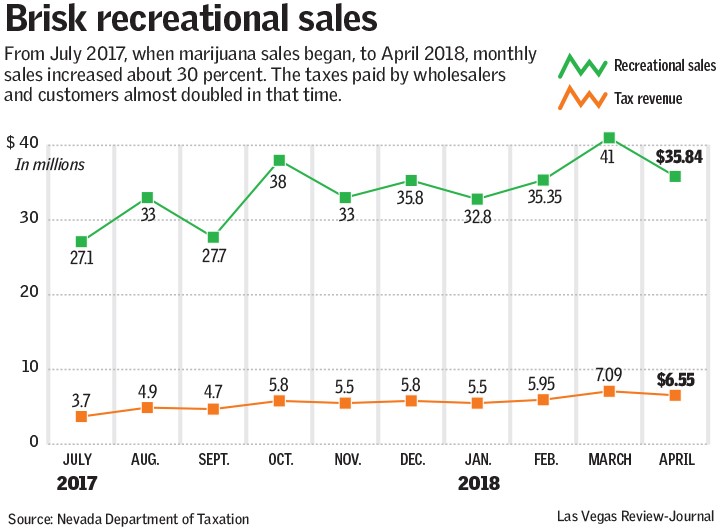

The Nevada market is growing. Total sales of recreational and medical cannabis in the first year were $500 million. Sales have been trending upward. The last available data point I see is for May, where sales were $48 million, which is up from the prior peak of $41 million in March.

Existing medical cannabis license holders have an advantage in the Nevada market. The state has limited new license applications to open to existing holders.

Nevada is in the process of accepting applications for another round of license approvals right now. Existing holders will be able to apply for licenses from a pool of 44 cultivation, 23 processing, three retail and one lab license.

Perhaps the only downside to Nevada is taxes. Cultivators pay a 15 percent excise tax on wholesale cannabis sales. Retail stores pay a 10 percent excise tax on each sale to a retail customer.

Silver State Relief Nevada Operations

C21 Investments added Nevada to their footprint with their purchase of Silver State Relief. The purchase price was $20 million USD of cash, $14 million USD of 3% interest bearing debentures convertible at $3.50 per share and 2 million shares.

The purchase price was for the business and associated licenses of Silver State. There is a separate option to purchase the real estate (the cultivation land and Sparks, Nevada dispensary location) for an additional $14 million (payable in shares). There is a separate option to purchase the real estate of a Fernley dispensary for $750,000. I don’t believe that they have exercised these options.

Silver State Relief has been around in Nevada since the legalization of medical cannabis. They were one of the first two companies to receive licenses in Nevada and the first company to sell an ounce of cannabis in the state.

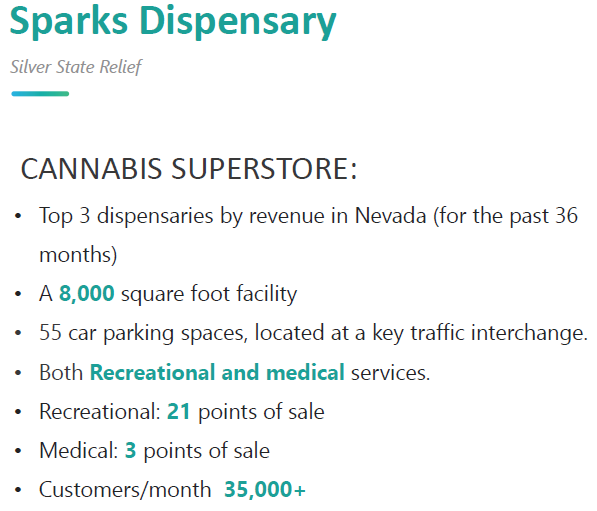

Silver State Relief owns and operates a 125,000 square feet cultivation and processing facility in Sparks Nevada, which is part of Reno. This facility, which is 20% utilized, is producing 5,500 lb/month of cannabis flower.

Silver State also owns a large dispensary in Sparks. They describe this facility as a cannabis superstore:

The second dispensary is in Fernley, about 30 miles east of Reno. It is under construction and scheduled to open later this year.

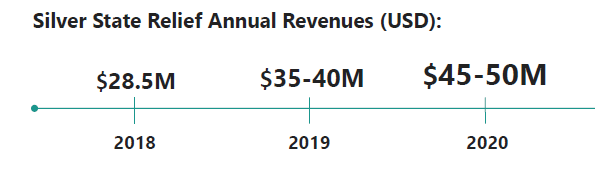

Here’s what gives me comfort with C21. The Nevada operations has tangible trailing revenue that allows some confidence in a valuation of C21. Silver State did $17 million of revenue in 2017 (in a half year of recreational sales) and is expected to do $28 million this year. This article says that sales in the first half of 2018 were $15 million.

Revenue is expected to jump again in 2019 once the Fernley location is open and further expansion is finished.

Silver State margins are quite good. In 2017 Silver State had $7 million of pre-tax profit, or about 40% operating margins. Assuming similar margins in 2018 Silver State pre-tax income should exceed $11 million in 2018 and $15 million in 2019.

We can’t be sure how the Nevada market will evolve. It’s possible more licenses will saturate the market. So far that hasn’t proved to be the case though I have read a few anecdotes that wholesale prices in Nevada are starting to fall. As I mentioned Nevada is opening additional licenses to existing holders only, so C21 and Silver State should be able to participate in that expansion.

Perhaps the biggest negative about Silver State is that, at least so far, they are not operating in Las Vegas. Nevertheless they have the 3rd biggest store in the state and Reno is a tourist destination in its own right.

I don’t think there is any doubt that Silver State Relief is the crown jewel of the portfolio so far. But C21 has made a number of other interesting acquisitions outside of Nevada as well.

Oregon Market

Oregon was one of the first states to legalize recreational cannabis in 2014.

As with other earlier implementers of recreational cannabis laws (Washington and Colorado are the others) Oregon flooded the market by giving out licenses to anyone with a dream, and is now experiencing an over-supply of product.

Oregon put very few limits on licenses when they legalized cannabis. It’s been easy to get a license and as a result far too many licenses have been granted. By some counts Oregon has over 2,000 producer licenses and 550 retail licenses (I believe the data from the GMP table I posted above is somewhat out of date and thus the higher numbers mentioned here).

Compare that to Nevada, which about one-tenth of the production licenses with a larger population and way more tourism. You can imagine what transpired.

Last year Oregon consumed somewhere around 400,000-500,00 pounds of cannabis. By some estimates (here and here) Oregon has been 1 million and 1.4 million pounds of product stockpiled.

With such massive inventory it is not surprising that wholesale cannabis prices have tumbled. Last year cannabis was selling for more than $1,500 per pound. This year it’s closer to $400 per pound and there are some accounts of product being sold for as low as $200 per pound.

Those are prices that can only be profitable for the most efficient producers and those with a brand that gives them leverage to hold firm. The mom and pop businesses are failing en masse. I’ve seen estimates that up to 150 dispensaries could close in Oregon in the next year, and that 30-40% of cultivation acreage have gone unplanted this year.

So Oregon is not a great market for commodity unbranded cannabis.

C21’s strategy appears to be:

- picking up established brands in Oregon

- focusing on organic, indoor, high quality cannabis cultivation that receives a premium in the market and is not over-supplied

- acquiring operations that allow them to produce value-added products like vape, edibles, CBD products, etc.

- Creating a vertically integrated chain of production

In total C21 has made 5 investments in Oregon so far:

- Eco Firma Farms

- Phantom Farms

- Swell Companies

- Gron Chocolates

- 7 Leaf/Pure Green dispensaries

These investments are complimentary of one another. Phantom Farms and Eco Firma are well-known and high quality producers of flower and rolled products. Swell Companies is an extraction and processing company, producing oils and consumer packaged goods. Gron has a focus on chocolates, and with 80% of the edibles market in Oregon. And 7 Leaf/Pure Green give C21 their first 3 dispensaries.

Together the acquisitions represent the entire supply chain, from production to retail sales. They give C21 a suite of 50+ SKUs to offer dispensaries. I think the weakest link is on the dispensary side. I wouldn’t be surprised to see more dispensaries added in the near future.

Let’s dig into each acquisition a bit more.

Phantom Farms

C21 bought Phantom Farms for $15.5 million. As with most of the Oregon acquisitions C21 purchased the company using in large part a non-interest convertible notes that have a conversion at a much higher price ($3.50).

Just a quick thought about the convertible and the Oregon acquisitions. C21 has been using non-interest-bearing convertibles for their Oregon acquisitions. In recent cases the conversion price was $3.50, which is well above the current share price. In the case of their two biggest Oregon acquisitions, Phantom Farms and Swell Companies, the convertible is structured to have a cash value much lower than the share conversion value ($8 million for Phantom Farms and $5 million for Swell Companies). This seems like a smart way of providing upside to these companies but protecting their own investment at the same time.

Each of these Oregon acquisitions also has a fairly significant earn-out if they can hit targets on EBITDA. So the structure does mean there could be further dilution in the future, but only if the company is succeeding. I’m okay with that.

Anyways back to Phantom Farms. They have 80,000 sqft of outdoor cultivation and another 5,000 sqft indoor facility, including a lab and warehouse space. I believe they are adding indoor grow space this year. Phantom is producing 5,200 pounds of cannabis annually. They have historically sold cannabis flower and pre-rolls (apparently they have very good pre-rolls).

The Phantom Farms brand is well recognized and highly rated. They’ve been around for 10 years. They sell their pre-rolls and flower into 175 dispensaries. They expect to sell oils by the fourth quarter.

Revenue is expected to grow significantly next year as C21 adds an extraction facility and another 40,000 sqft of (indoor?) cultivation.

Swell Companies

Swell sells a number of processed THC and CBD brands into the Oregon market. They sell products via their Dab Society, Hood Oil, Quill and Swell brands.

Swell is extraction and processing company. While I believe they have some of their own growing capacity, the primary business is on processing THC and CBD extracts and manufacturing of the resulting oils into vape cartridges, capsules and tinctures. Their website gives some information about the specific products available in each brand.

Swell delivers 50 distinct SKUs and has products available 275 retail locations. They shipped 500,000 product units into the market in 2017.

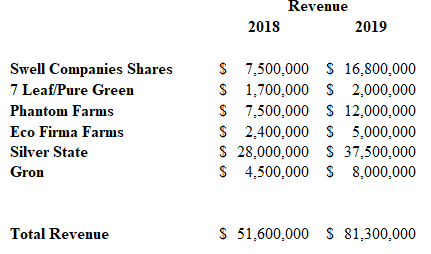

According to C21’s presentation Swell had $6.5 million of sales in 6 months of operation in 2017. C21 says monthly revenue from Swell is $1 million.

While it’s impossible to know the composition of their sales, I did dig a little into what some of the more popular product lines sell for. Dab Society products go for $25 to $50 per gram. Hood Oil sells for $20 per gram.

Those are interesting price points because they illustrate the value add of branding and processing. I mentioned earlier that commodity flower is $200-$400/lb. The processed products from Swell sell at an order of magnitude higher price.

Eco Firma Farms

The first acquisition made by C21, which coincided with the reverse takeover and initial stock offering, was Eco Firma Farms. They purchased Eco Firma Farms for a little over $4 million, again payable via convertibles.

Eco Firma produces about 2,500 lb of cannabis per year from 23,000 sq ft of grow and processing space in Canby Oregon. I believe much if not all of this space is indoor.

If you google Eco Firma and their owner Jesse Peters you will find a lot of articles, videos and interviews with the company. They are well-known in Oregon for their organic and environmental production practices.

They are also one of the lowest cost producers in the state. According to this article “it costs Eco Firma $189 to produce one pound of cannabis. (That comes out to $11.81 per ounce, or $0.43 per gram.)”

Eco Firma sells the flower and a rolled cigar-like smoke that they call Pachecos. They list 41 dispensaries across Oregon on their website and have been selling the 19 strains they grow since 2012. Eco Firma has won a number of awards for their strains:

Part of the acquisition stipulated a $5 million investment in Eco Firma. So there are significant expansion plans.

Like Phantom Farms and Swell, Eco Firma products appear to command a premium price. Here are a couple of sales ads I found for Eco Firma product.

Even on sale, we are looking at prices that translate to $1,300-$3,200 per lb. Much higher than the commodity wholesale prices quoted in the articles I’ve read.

C21 is projecting $12-$16 million of revenue from Eco Firma in 2019. This is probably the revenue estimate that I find most uncertain. I’m not entirely sure how they get to such a big number. In the presentation they point to the $5 million investment in retail and indoor grow operations. So there is a lot of growth expected.

Nevertheless, it seems that in the past Eco Firma had relatively modest revenue. So I’m taking their estimates with a grain of salt for now.

Gron Chocolates

Gron Chocolates was the latest acquisition of C21, being acquired a little over a week ago. The purchase price was $6.8 million with an additional $4.4 million potential earn-out. The price was paid via cash and convertible but I’m not sure about the weighting of each.

There wasn’t a lot of information available about Gron so I called the company and asked a few questions. Gron has 80% of the edibles market in Oregon and, according to the website, are in 400 dispensaries in Oregon (there are ~500 dispensaries in total in Oregon). They are expected to deliver $4-$5 million in revenue this year, and that is expected to increase to $8 million in 2019. In 2019 they will be expanding the brand to Nevada, where it presumably be available in the Silver State dispensaries.

One other point is that Gron makes both THC and CBD products. The CBD products are interesting because they are considered “non-hemp” and do not have the same state constrained laws. A Gron CBD chocolate can be sold nationally, which gives it more potential. I don’t totally understand how big this opportunity is but it is interesting. When I talked to the company they seemed to be pretty excited about the CBD angle. So we’ll see.

Capitalization

C21 has about 51 million shares outstanding. I say about because there are so many transactions and so many convertibles that it’s a bit of a rat’s nest to come up with the final tally.

Here is how I came up with it. As of the date of the July 10th MD&A there were 42.8 million shares outstanding. There are another 4 million shares issuable to Eco Firma as part of that acquisition that are part of in the money convertibles (these are in-the-money), and another 2 million issuable to Silver State. Another 2.1 million shares were offered as part of the July capital raise. There may be shares issuable to Gron but I don’t know if they are priced in-the-money or at a higher price so I just included that $6.8 million purchase price as additional debt.

There is about $33.7 million of debt if I add up the cash redemption value of all of the convertible debentures and the Gron acquisition on top of that. Like I said earlier the cash value of the debentures issued to Phantom Farms and Swell Companies is less than the share conversion value. Only if the share price gets above $3.50 do I need to consider dilution of the convertible from these acquisitions.

I think there is also roughly $5 million USD of cash remaining on the balance sheet. The cash number is also tricky to estimate, but I know that they had $27 million CAD of cash at the end of April and that their acquisitions (Silver State Relief) included a $20 million USD cash payment. They received $4 million USD from the July raise. So that’s how I’m coming up with the $5 million number for cash and as a result the $29 million of net debt (all in the form of the convertibles).

Conclusion

Below are the combined 2018 and 2019 projections for each of the acquired companies.

Apart from the dispensary revenue from 7 Leaf and Pure Green and the Eco Firma revenue, all of the estimates I used are from the company’s own presentation.

In the case of the 3 dispensaries, I used the purchase price of each and assumed a 1x revenue multiple (this is about the going rate of a dispensary acquisition in Oregon) to come up with a revenue estimate.

For Eco Firma, I wasn’t sure how the revenue estimates from the company could be so high, so I took them down to be conservative. I took the latest production estimate (2,400 lb per year) and assumed they can sell that for on average $1,000 per pound. Maybe I am being too conservative but I need more information to be comfortable with the Eco Firma projections. For 2018 I doubled revenue to $5 million, which is far less than the $12-$16 million the company has pegged in the presentation.

EBITDA Margins are tougher to peg. I know that Silver State operating margins have been in the 40% range. I don’t know what the margins on any of the Oregon operations should look like. I basically made a simple guess – I used 40% EBITDA margin for Silver State and 20% for each of the Oregon operations (20% is on the low side of what Canaccord and GMP have been using for the companies they cover), which gives the blended 29% margin that I showed in my original comp table.

Getting back to the comp table, if the numbers and my assumptions are okay, its clear that C21 Investments is at a pretty significant discount to the other companies in the list.

Why is that? Honestly my best guess is that each of the other companies is covered by Canaccord, GMP and/or some other brokerage. I think that investors are familiar with these other names but not C21.

Its also possible that some discount could be attributable to having some of the operations in Oregon. But both Golden Leaf and Cannex are in Oregon so that doesn’t totally ring true.

At any rate, from what I can tell C21 has acquired a good operation in Nevada and some pretty solid brands in Oregon that should be able to survive the headwinds and likely come out the other end stronger. What’s more, they’ve put together a very complimentary suite of assets that allows them to produce, process, and manufacture a wide range of THC and CBD products. Some of these brands can be expanded into Nevada, which you are already seeing with both Phantom Farms and Gron.

Anyways, based on my research so far I don’t see anything wrong with the businesses acquired. I think its more likely a supply/demand problem with the shares. You take the lack of promotion and exposure, you add to it holders from the original shell that are probably happy to get out at this price and maybe some holders from the original private placement that don’t like the price action so far.

If I’m right, maybe the biggest negative with the stock is how long this overhang lasts.

The other possibility is that I am missing something here. Which can never be ruled out.

Another risk has got to be further dilution. I suspect that C21 isn’t done with the acquisitions. At the very least it would make sense to add more dispensaries in Oregon to fill out the vertical chain. How this plays out and whether stock is offered at these lower prices is a fair question.

Nevertheless, if my numbers are accurate then the stock is reasonable at these levels. I’m used to waiting for something to work. So I’ll be patient. I’m keeping my position on the smaller side simply because, as I mentioned earlier, everything right now is a projection and so this feels like a risky position even for me. But as we get firmer numbers and especially if the stock starts to work, I won’t hesitate to add.

Thanks for this write up!

Where did you get the ebitda margin for Cannex?

They delayed latest financials and I can’t seem to find a number for this year…

Yeah I didn’t have a great source for Cannex. This Cantech letter pegged it from Beacon Securities. It seems unreasonably high?

https://www.cantechletter.com/2018/06/cannex-holdings-has-82-upside-beacon-securities/

Thanks. Yeah seems too high, I guess it is more or less, what you adjust for?

Have you looked at The Green Organic Dutchman (TGOD)?

I know a little about them but haven’t looked closely. what are your thoughts?

This got me interested

https://geckoresearch.com/tgod-short-squeeze-of-the-century-explained/

Haven’t researched too deep, but I like what they do overall so far.

To me also, it looks a very good choice, with a lot of potential. Bu nobody seems to care about it (-10% today ..). Wait and see…

Yeah its really under pressure. Have to wonder if there is a financing coming or something?

I speak about C21, of course!

What broker are you using to trade this stock? My understanding is that it’s not available on Interactive Brokers because it’s not DTC eligible.

That could be. I’m Canadian and from what I can see all the Canadian brokers, BMO, TD, RBC etc trade it.

@Ren. I use Keytrade (Belgian bank) and I could buy C21 Investments on their platform.

This is definitely interesting, particularly if the underlying companies can show operating profits at an early stage.

One concern I have is whether the principals of C21 are capable of managing so many operating companies. Or is C21 primarily an M&A group and operations will suffer because no one is managing the group of companies well.

Another concern I have is doing a deal in Ukraine, as a gateway to the European Union. Are they not aware that Ukraine is the crime capital of Eastern Europe and that if they did have any kind of operating profit they would immediately be surrounded by the Russian/Ukrainian mafia and corrupt politicians? That seems like a huge error to deal with such an unstable country. What is the strategy there?

The one thing about this that I didn’t realize is that the Silver State deal isn’t closed yet. They need to get the capital raise done so they can close this deal and then the outlook would be more certain.

Now that the stock has tanked, maybe it is time to load (in order to get a medium buying price). I bought some at 1.10.

Yeah I don’t know. See my other comment. Until we see the financing close I think I have to be skeptical. I was stopped out of some of my position earlier this week. I still hold some but we are 7 days past the financing deadline and haven’t heard anything.

How much of the convertible financing they recently did was actually received? It’s problematic to start a new financing now with the stock down so much.

Its the same financing. They haven’t closed the convertible yet, or at least they haven’t announced that it’s closed. Until we get an update on the status its pretty tough to know whats going on. I figured if they can close even $20mm of the convertible that would be enough to close Silver State and the stock would seem very cheap right here. But until we hear something its a shot in the dark where we are at.

They closed their convertible, closed Silver State, the Oregon production operation, and the Oregon retail dispensary.

This is starting to look real.

Having just looked at their convertible, I wish I had tried to get in on that. Those people made a killing, getting a convertible at a good price and getting a warrant with that convertible that lets them double up the investment with a two-year optionality.

It is. I need to figure out the fully diluted share count again after the financing, do you have that off-hand? Btw part of the move this week was probably because of this: https://nam06.safelinks.protection.outlook.com/?url=http%3A%2F%2Fwww.bnnbloomberg.ca%2Fbruce-campbell-s-top-picks-jan-30-2019-1.1206537&data=02%7C01%7C%7Ca684da4064a041d60b3f08d6873c9384%7C84df9e7fe9f640afb435aaaaaaaaaaaa%7C1%7C0%7C636845091568496516&sdata=0RuO%2FTY06iGUN2x8m70fYqXNvlc5UKo7oNpEDX0VeoY%3D&reserved=0

The share count from the financing appears to be:

* Just short of 15K $1000 convertible notes each convertible at 80 cents per share. So let’s call that $15M cash in and 18.75M shares.

* Each of the 15K convertible notes includes a warrant to buy an additional $1000 debenture but at a conversion price of 90 cents per share. So that represents an additional $15M in but at a dilution of 16.67M shares.

I guess none of this is in the reported numbers on Yahoo?