Week 412: Round Trip

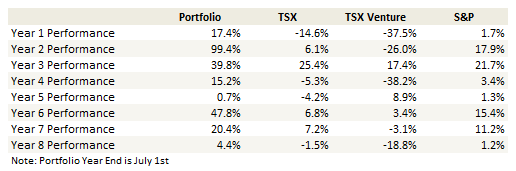

Portfolio Performance

Thoughts and Review

First and unfortunately I was stopped out of Intelligent Solutions this week. It was not a hard stop, but I had set in my mind that if the shorts continued to attack the name that I wouldn’t fight it. So when the second report came out on Thursday, I didn’t hesitate and sold.

That meant a full round trip on the name, which was painful. My reasoning had nothing to do with the content. In all honesty I didn’t even read the second report. The point here is the spirit; the intent is clearly to be sustained, and in the face of that pressure how can I own the stock?

The shorts always have uncertainty at their back. They always have the 5,000 other stocks out there that are relatively unblemished alternatives for investors. There is probably a level where I am willing to own Intelligent Systems again, but it is lower than $27, as the risk premium I would tag to this short attack is unusually large.

That is in part because of the shorts, which are very good at what they do, well known, and generally respected. Each report seems to carry weight and I’m not sure if the content is really that relevant to that.

In part it is because of Intelligent Systems. Look, I was naive. I knew about Parker Petite but I thought the business and the modeling I did of its prospects, mattered more than his likely limited role on the board. I knew about the related party transactions, I mean they are right there on the conference calls, but I didn’t think of them negatively because they seemed small and the company seemed up front about them. I actually thought the shorts would look at Intelligent Systems and think not to bother.

I see Intelligent Systems is fighting back with a conference call on Wednesday. I wish them well and, at the right price or if there is evidence the shorts are backing off, I will look at it again. But for now I simply don’t have the desire to wait and see if there is another shoe to drop.

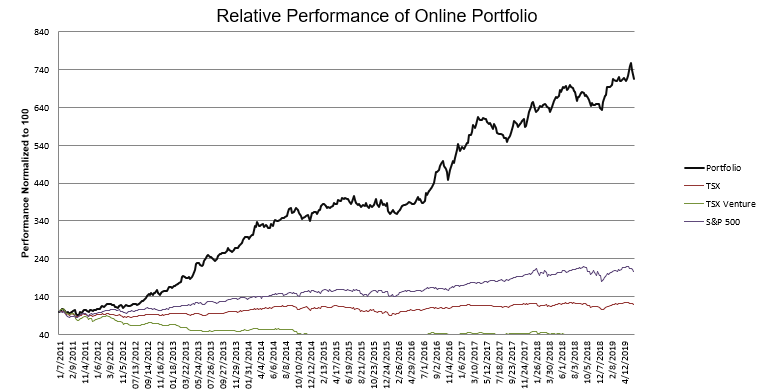

The round trip in the name meant a round trip in my portfolio. While I could cry over this spilled milk, a quick look at the chart of my portfolio reminds me this is just a blip. I used the example of Bellatrix when I wrote about Intelligent Systems a few weeks ago – that occurred in October 2014. You can see a similar blip with my portfolio then. But I didn’t let it derail me, and I kept on going then like I will again now.

Apart from that I’ve done okay, but my performance has again been skewed (positively) by the weak Canadian dollar. I mentioned this last update – again these last 8 weeks I gained a full 1% of performance from the Canadian dollar weakness. Unfortunately in my actual portfolio I am hedged on currency to a large degree so this is misleading.

My primary position changes apart from Intelligent Systems have been large index shorts (RWM, HIX, SH and such) including a short on the newly release marijuana ETF (I also remain short Canadian banks and a number of tech names), a few small long positions which I may or may not keep, a long product tanker trade and a long protein producer trade.

My tanker trade is expanding again to being long IMO 2020. I listened to Ardmore Shipping’s Investor Day. They had Andrew Lipow on as their expert. He painted a very interesting picture – one of increased refinery runs, expanding crack spreads, and large discounts for heavy oil. By coincidence I talked to an oil trader at a large refiner this weekend and he mostly agreed with the assessment.

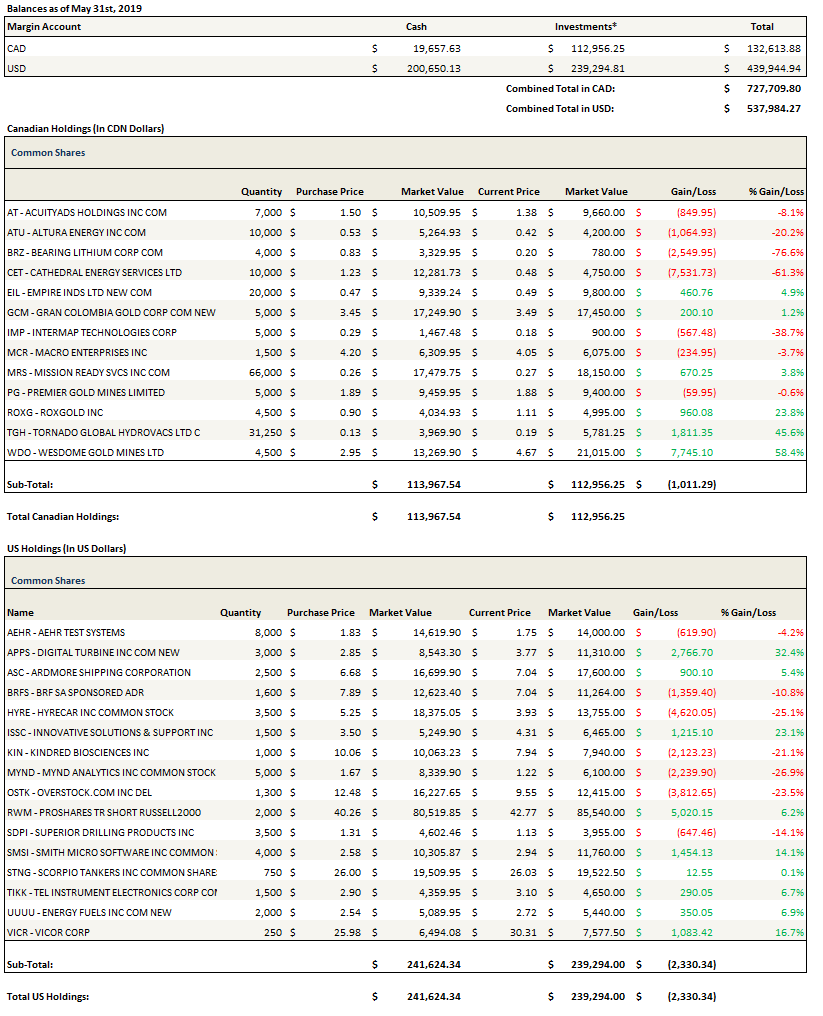

So while I didn’t have any refiners in my portfolio as of Friday (the snapshot I’ve included here), that changed Monday. The ideal refiner would have ready access to high sulphur fuel oil spreads, being able to run increasing heavy crude loads if prices dictate. I added Marathon Petroleum on Monday, which is not ideal but should benefit. I also added a second refiner, which is much closer to ideal, but which I am still adding to, so I won’t name that name yet.

The protein producer trade I’m still working on, and I’m not sure I’m right about it, but it seems like African Swine fever is going to eliminate a significant amount of China’s pork supply. While this should help all protein producers (Tyson and Sanderson Farms are two charts that have been very positive this year) – I think the one it could help the most is BRF SA. They are a maligned, restructuring producer in South America. As such the stock is still well off last year’s highs. But they are not in the middle of the trade war, which means they should benefit more than their American competition, and they seem to be turning their business around, though that might be too early to say. I bought the stock too high and it has come off, but I will give it room to work because I am of the mind this plays out positively in the next year or so.

Every so often I dedicate a post to some of the small-nano cap positions that I hold on my books. These positions are generally too small to hurt me much but likewise they are unlikely to help unless they become moonshots. Which is really why I keep them around. There have been some interesting developments with a few, so here it goes.

Empire Industries

I have no idea what is going on with Empire Industries.

To put it bluntly, the fourth quarter was a disaster. Here are some highlights:

- Lost $48 million in the fourth quarter

- Reported a whopping -50% gross margin on the quarter

- Posted -$15 million of EBITDA

It is really no exaggeration to call it a disaster. Keep in mind that Empire had a market capitalization of about $40 million at the time. They lost more than their market cap in a quarter!

The company did provide a reasonably positive update. But I can’t imagine that alone is moving the stock. The team here should have very little credibility after having said last year at this time that the losses from first-generation products were behind us.

Honestly, when I saw the results released over night I thought the stock was going to open sub-30c the next day. When it didn’t I was surprised but thought there had to be a delayed reaction coming. None did. Instead the stock steadily climbed higher.

Honestly, when I saw the results released over night I thought the stock was going to open sub-30c the next day. When it didn’t I was surprised but thought there had to be a delayed reaction coming. None did. Instead the stock steadily climbed higher.

I can think of one possible reason that the stock is climbing like this. And that has to do with the debt.

The Group just closed a $38.5 million debt financing with what they called “a wholly owned subsidiary of a Fortune 500 company”. The rate on the debt is prime plus 9.5%. It’s not free money.

I went through the Fortune 500 list of companies. This isn’t a big bank. If they were getting money from a big bank it would have come from Canada.

There are a total of 4 companies that have some tie to the industry Empire is in: Disney, MGM, Discovery, and Wynn Resorts.

Of those 4, there is 1 that I could see moving the stock like this. Disney.

So that’s my guess. A total blind guess. But its the only thing that could explain the price action. Somebody found out that the lender is Disney. Which would mean Disney is willing to backstop the business. If that is the case, it’s a very big vote of confidence. But again, I’m guessing.

Empire has since then announced its first quarter results. They were better. Positive EBITDA at least. But nothing to write home about.

Yet the stock holds up. I have to think that something is going on.

Tornado Hydrovacs

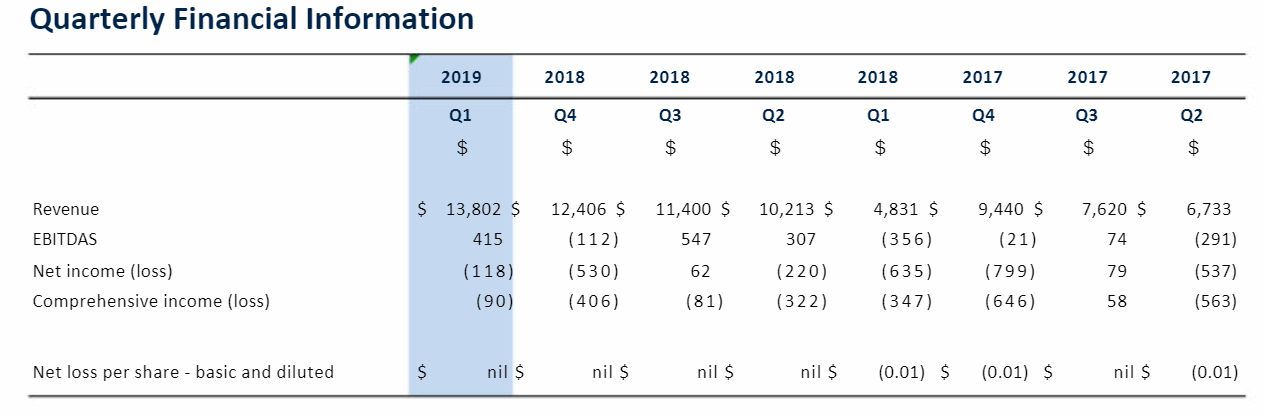

Tornado has been the much better performing sister company of Empire since they were spun out a couple of years ago. They announced their own first quarter results this last week and again they were very good.

Revenue has been flying at Tornado for the past year. Year over year it was up from $4.8 million to $13.8 million.

Its still a very low margin business though, which means even with the revenues they aren’t seeing a big return to the bottom line. Gross margins for the quarter were 14.4%, which is lower than the 16-18% margins they’ve had in the past. They attributed this to too much business – outsourcing some parts to other vendors that had to ramp their production to accommodate it. Tornado said this will come back down in the next few quarters.

The China business remains a work in progress. Tornado said they were still focused on “developing business” in China – rentals and educating market – which probably means that they don’t have a big sales pipeline yet.

Tornado generated nearly $1.5 million of cash from operations in the quarter. But $1.2 million of that came from working capital adjustments.

With 126 million shares outstanding, at 21c the market cap is around $25 million. That seems close to fair given where we are with the business but maybe cheap if China gets going. They need to put some more of that revenue onto the bottom line, and show some revenue from China, before the market is going to pay much more.

Cathedral Energy Services

I continue to be surprised by just how crappy this business is doing.

I know the oil services business is hard and how right now it is very hard. But I keep thinking that Cathedral will figure out a way to squeak in some profits here at some point. But that has yet to happen.

Revenue in the first quarter was okay – it came in at $37 million versus $40 million the previous year. But gross margins were not very good – 7% versus an already low 12% the year before.

The company blamed the poor results on the management of the US business and not a sector-wide slowdown. To that end they reorganized the US business and let go of the man in charge and replaced him with the former head of Canadian Operations – Clayton Lagore.

It does look like something was wrong on the US side – they noted in the MD&A that the average day rate was up from $11,662 per day to $12,969 per day year over year. You would think that with a little bit of pricing power that Cathedral would have been able to expand margins, not shrink them.

I’m sitting on this stock as dead money, just waiting for something to happen. While I clearly should have sold a year and some ago when the stock was $1.50, it seems too late to do that now. Tangible book value sits at $81 million while at 61 cents the market capitalization is around $30 million. Of course the argument can be made is that these are not terribly good earnings producing assets, which is a fair comment. Nevertheless it is a point of consideration that makes me willing to sit on my small position and wait.

Innovative Solutions and Support

This is one of a couple of my most recent nano-cap pick-ups. I’ll try to get to a more full write-up, but just briefly here is the thrust of it (pun intended):

ISSC produces aviation products: Flight Management Systems, auto-throttles, cockpit displays and air data equipment.

The opportunity here is two-fold. ISSC is experiencing an up-tick in demand because their utility management system is being sole-sourced for the new PC-24 aircraft from Pilatus and increased demand for cockpit retrofits of 757 and 767 aircraft. B.

But its their ThrustSense Auto-throttle that is the big opportunity here. The auto-throttle provides engine safety and protection – it is intended to be an upgrade component on smaller aircraft like the twin-engine turbo-prop.

The market for this upgrade is extremely large. Management estimated that over 5,000 King-Air aircraft are addressable and that overall 10,000 aircraft are addressable. ISSC has received FAA Supplemental Type Certification for retrofit on the King Air aircraft and the PC-12 aircraft.

ThrustSense sells at ~$50,000 or it can be paired with a retrofit cockpit for $300,000.

That puts the TAM on the low-end at $500 million.

ISSC has a $60 million market cap with $20 million of cash.

I will write more later but that’s the punchline.

Mission Ready Services

Since the close of the Unifire deal Mission Ready has made two contract announcements (here and here). It’s not a bad start, and if it is representative of a typical month then we might actually be onto something.

The stock seems to have a huge overhang of shares however, which I don’t really understand. It is odd to me that there was far less selling and far less on the level 2 during months of uncertainty where we didn’t know if there would even be a business when it all was said and done. Now that Unifire is in the mix and contracts at the ready, the shares seem to have accumulated on the ask. Does that not seem a little bit odd?

At any rate it appears that Mission Ready will sit here at this level until we get a data point that compels some big bids to come in. What could that be? Well an investor presentation, one that actually gives some indication of the profitability of Unifire’s business, would be a start. And keep the monthly contract updates coming.

Overstock

Yeah okay so this isn’t a nano-cap or even really that small of a position for me at the moment. But I like to tuck it in here so I can talk about it without getting anonymous emails about the stock.

It’s a battleground.

Yeah so its true. I bought Overstock again. I think this is time #4? The first two worked, the first actually worked very well. The third, and most recent, worked not so great – I believe I sold it around $17 after buying it at $20.

So now we are on #4. This time I feel like I might stick around for the denouement. Unfortunately I bought some before Byrne disclosed that he sold shares. After he did, I doubled down in the $10’s and promised myself I wouldn’t buy it again!

So why buy Overstock? It was really all about the retail quarter for me. It looks like its turning around. The Google SEO results continue to improve and that is the driver – free customers. I think I said it in an earlier update – the fact that the e-comm business didn’t collapse even more given what was going on with their SEO customer acquisition is really quite something. I mean how can you lose all those free eye-balls and still make a go of it. I still think the whole growth initiative last year was a smokescreen to invest in figuring out SEO before the entire business became too far gone to repair.

So what did we get? Byrne sold shares. Then told off the shareholders for asking him why. What else is new? I’m not sure if anyone noticed but in his letter lambasting shareholders he did point out that there were comments of interest made at the General Meeting of Shareholders. I listened to that. It was worth the listen – though as with anything said by Patrick Byrne take it with salt.

I think its a pretty simple bet here. If e-comm isn’t on its way to oblivion then at some point the stock trades back to at least the high-teens. Maybe higher. The tZero business may be huge and may be nothing – its same as it ever was. This Medici Land Governance is landing some large deals (again listen to the Meeting of Shareholders for some more details on that) but who knows what those are worth.

One last consideration for me is that if e-comm is not hemorrhaging money any more (and as it has been quite rightly pointed out to me, we don’t actually know that this will be the case – it could be a lull in the downward spiral that is the Overstock e-commerce brand), then it should be a lot easier to sell the business. Again I think I pointed this out once or twice before – I can’t imagine Overstock was getting anything but low-balled at best, turned away at worst, when the e-comm business was losing $50 million a quarter and showing a precipitous decline in their free traffic. Who wants to buy into that? If the business is stable, maybe someone might actually be interested in it.

Anyway, its a little under $10. We’ll see.

Blog Update

I have locked my blog for the time being. It made me uncomfortable to find myself linked by a short report and see traffic from that short report clicking the link and visiting my blog. I don’t see a lot of good coming of that. So I prefer to limit the visitors for the time being.

Portfolio Composition

Click here for the last eight weeks of trades.

{kind=link}

Hi, long time lurker here, thanks for granting me access to the protected version of the blog. Reading this has been quite educational and I have you to thank for lots of ideas that worked out well – CMBX, VICR, AC, GCM, WLDN, to name a few, not to mention all the ones that I read about and kick myself for not pulling the trigger! Anyways, I’m sorry to hear about your woes with malicious readers and hope it all blows over soon.