Another way I’m Playing IMO 2020

I’ve spent a lot of time digging into IMO 2020 over the last couple weeks. This is on top of all the time I spent late last year and early this year. So sum total its been a lot of digging.

The conclusion I’ve come to is that its complicated. Its not really clear how many elements of the crude complex (a catch-all name for every producing, storage, transportation and refining piece that plays a part in getting crude and refined oil products to customers) are impacted.

The two things that seem most certain to me are:

- Heavy sulphur fuel oil spreads are going to widen

- Demand for distillates will increase

So how do you invest in those most likely outcomes? The best I can come up with is to A. buy product tankers that will ship the distillate from one place to another and B. buy refiners that can take high sulphur oil and convert it to light products like gasoline and diesel, and to.

I’ve talked about product tankers before. So let’s focus on the refiners.

I actually feel more confident that heavy sulphur fuel oil spreads will widen then any other outcome from IMO.

Why?

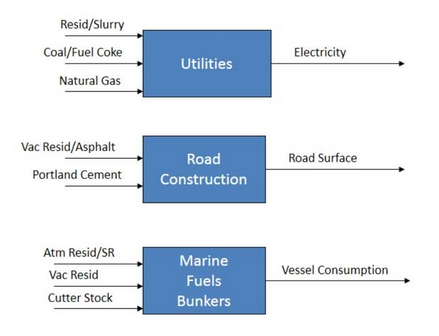

With IMO 2020 sulphur becomes the enemy. In the past, refiners would use high-sulphur fuel as feedstock, make money off the light products and sell the bottom of the tank high-sulphur dregs into the bunker market.

Apart from ships with scrubbers and some non-compliance that will no longer be the case. The only remaining markets are asphalt and low-end power generation. Those markets aren’t big enough to take over the nearly 1 million barrels a day of HSFO that will need to find a home.

The price just has to come down.

I’ve listened to a lot of conference calls from refiners. The most interesting comments came from PBF Energy CEO Tom Nimbley. He answered a number of questions on the topic on PBF’s fourth quarter call. I’ve put those comments together here to form the narrative.

First, he frames the issue at hand that we are all aware of. If a refiner doesn’t have complexity (cokers or hydro-crackers), they can’t turn HSFO into light products. Thus they are producing high-sulphur fuel as a product:

There’s over 4 million barrels a day of distillation capacity that has low complexity and significantly more than that doesn’t have coking capacity. So on paper, if you lose the outlet for your high sulfur fuel oil bunker market and that stream is still there…

The “…” is the trailing off of the thought “what happens to all that high sulphur product?”

Second he puts some numbers to the problem. HSFO prices are going to fall. Spreads will rise.

If indeed, you’re on the margin going to the power sector [because there is no bunker market], then you are going to end up with these $30, $40, $50 clean/dirty spreads, which will push coking economics to be very attractive

Third, he explains what refiners with complexity (ie. cokers and crackers), are going to do if spreads get to that point.

Personally I think you’re going to see an opportunity or a shift, a wave of perhaps going from a filling your cokers on the margin from crude to filling your cokers on the margin from somebody else’s stranded feed stream [HSFO].

we’ve got to be ready to be able to have the catcher’s mitt to take somebody stranded oil and not necessarily just fill the cokers with crude.

We are starting to see the market price in some, but not all, of this in the futures. HSFO futures are up to a $10 spread between now and January 2020. That is up about $3 from a few weeks ago.

The tough part with buying refiners here is that there are a lot of other variables that determine the share price. I’m still waffling because they are anything but recession proof. Crack spreads are volatile. This isn’t as clear cut as product tankers.

A weak economy is going to hurt them. Increased gasoline exports out of emerging markets are going to hurt them. Tight heavy oil supply out of Venezuela, Saudi Arabia, Iran and Alberta is going to hurt them.

These are all considerations that (I believe) are responsible for their dreadful performance this year. These stocks are way down even with the prospects of IMO on the horizon. It’s my (albeit tentative) conclusion that the downside risks are priced in whereas the upside one’s are not.

My biggest refiner position is Marathon Petroleum. It seems relatively safe because of its size. It has complex refineries that can take advantage of high sulphur crude, in fact it has the largest capacity of coking and hydro-cracking capacity of any independent refiner. It has two very large refineries in the Gulf and a bunch in the North that are destinations for Canadian heavy crude.

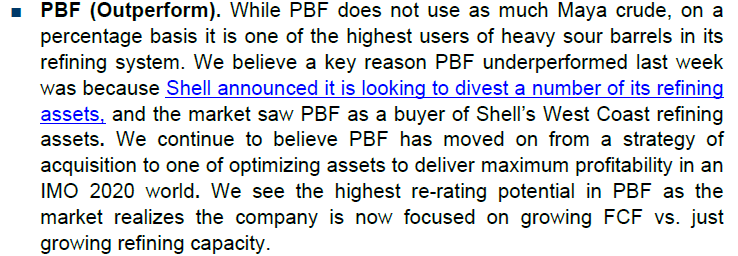

The second position I’ve taken is PBF Energy. I bought a little of this one a week ago but added to it after the stock swooned on news of an acquisition.

PBF announced on Tuesday that they were buying the Martinez refinery from Shell. I guess the stock slid because of worries about debt. Some analysts were also taken by surprise, having not expected PBF to make an acquisition. Consider this piece from Credit Suisse a few weeks prior:

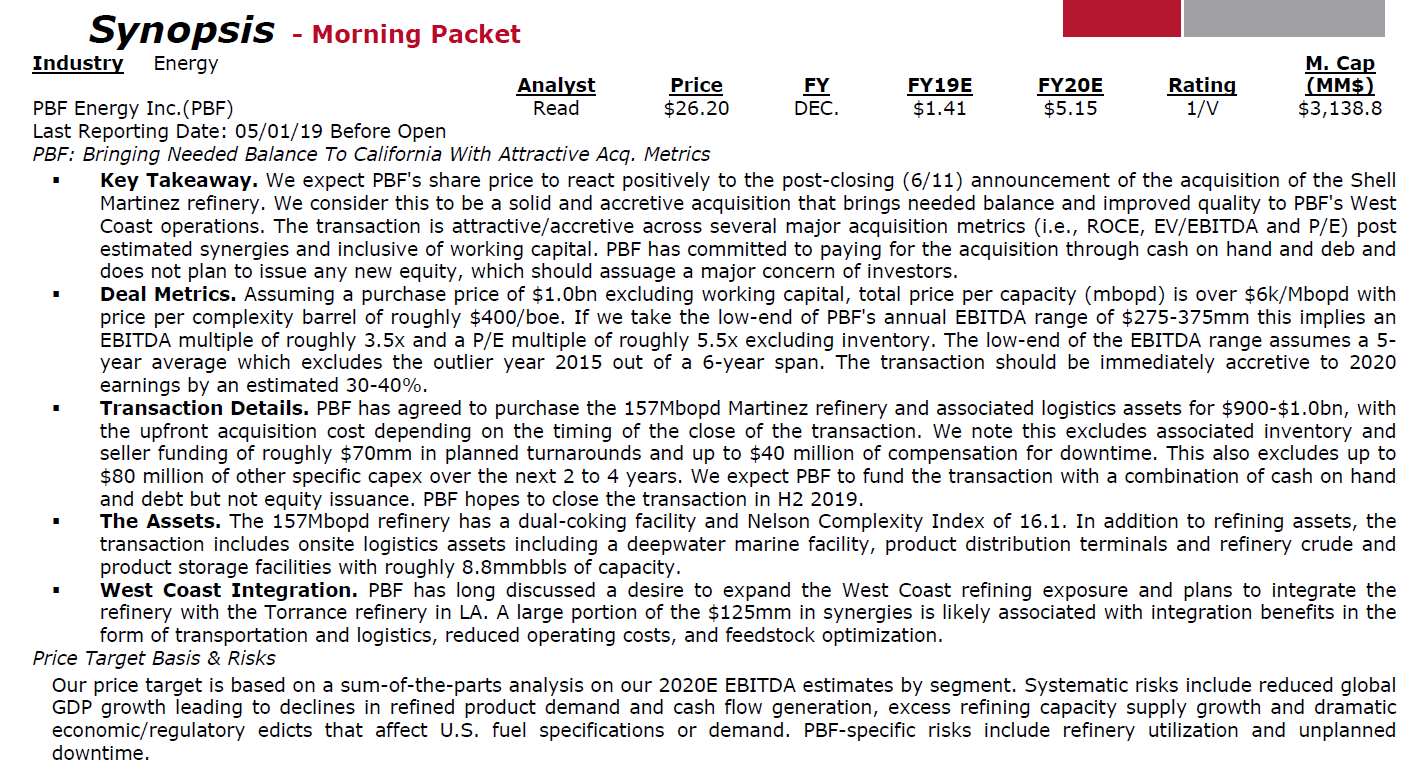

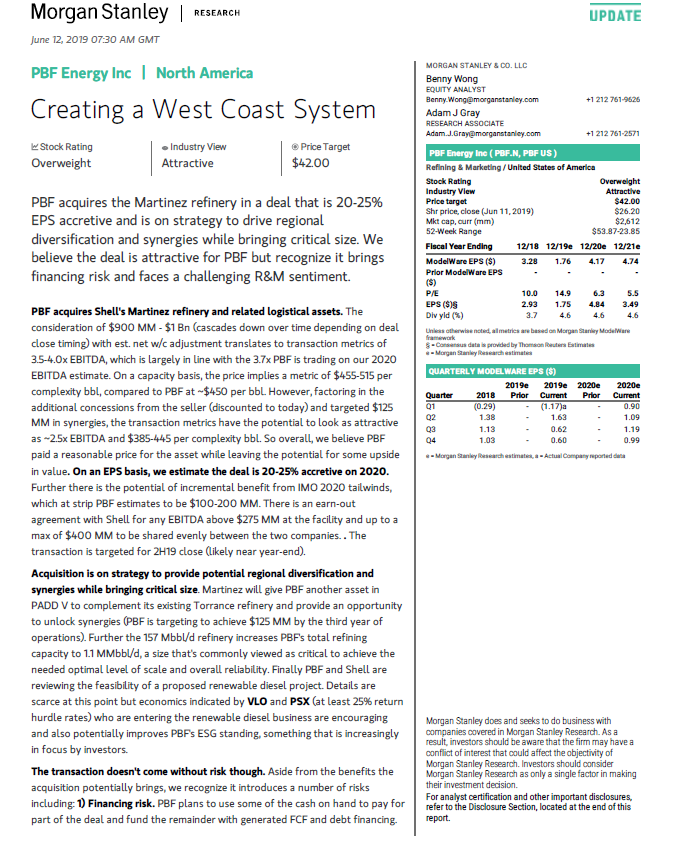

I believe that PBF got a fair deal and the upside from IMO 2020 is significant (I have pieces on the deal from Wells Fargo and Morgan Stanley). On the call the analysts seemed to want to discount the IMO upside. In an RBC note they said that their discussions with long investors gave “feedback on PBF’s Martinez acquisition [that] was exclusively negative.”

That’s fine. If I’m right then it will be an upside surprise.

PBF Energy has some of the most complex refineries in North America. They will benefit if HSFO spreads rise significantly. As I quoted above, Tom Nimbley, their CEO, is ready to switch their cokers to HSFO if prices dictate the move.

But PBF is also one of, if not the, most levered refiners to spreads and that goes for the downside as well. I have to be careful with this position. A recession will send the stock tumbling.

The third position I’ve taken is a much smaller refiner called Vertex Energy. Vertex has some hair. They have debt that needs to be refinanced. They have a messy share structure with convertible preferreds.

But they are perfectly positioned for IMO. Vertex runs odd little refineries that take in used motor oil (UMO) as feedstock. It just so happens that UMO is benchmarked off of HSFO prices (#6 fuel oil). The discount for UMO is typically between 70% and 90% of HSFO.

Vertex laid out the scenario in this white paper last summer. The numbers seem legit to me. For every $10 move in HSFO, all else being equal, Vertex adds around $12 million of EBITDA.

Vertex is a play that things get silly on the HSFO side of things. The $10 drop we see in the curve is nice, and it will help Vertex, but it isn’t what I’m looking for.

I think there is a chance where there is simply too much HSFO and no where for it to go. In that case the price change is more like the chart in the white paper. Or better.

In addition to its existing capacity, Vertex is expected to re-open their TCEP refinery in anticipation of IMO. The company said they have been working on developing products from their TCEP refinery that will be blend stocks for IMO compliant fuels. The Marrero refinery, which is operating, already produces a compliant low-sulphur (~0.1%) fuel.

The product slate from these refineries means there is some chance of upside pricing on that end as well. But we’ll see. I’m less certain that there is a significant pricing change on the low-sulphur fuels. It’s the drop in high-sulphur fuel that seems most likely.

{kind=link}

{kind=link}