Week 425: A few good moves

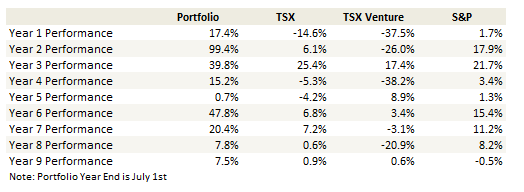

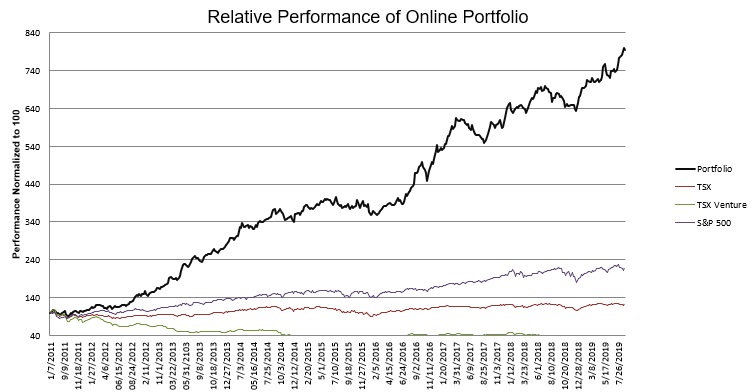

Portfolio Performance

Thoughts and Review

The last six weeks saw the sudden move up a number of stocks I own.

The biggest move was by Smith Micro, which went from $3.23 to over $6 on a great second quarter.

Then there was the near doubling of Moneygram which I bought at $3.06 and it has moved to almost $6 itself. There has also been a nice move in Evolus, though I’m not sure anything Evolus stock does matters until we get a resolution on the status of Passport.

There’s Overstock, as there is always Overstock. It moves up and down like a crazy Byrne but in the last 6 weeks it has been mostly up and who knows what the hell is going on there (by the way did you know that Marina Butina, who is Byrne mistress and the reason he stepped down as CEO is portrayed on an episode of the Family on Netflix-great show-for having been caught infiltrating the Christian prayer breakfasts in Washington. No joke, it gets weirder and weirder).

Gold stocks also moved up (though they gave up some of those gains these last couple of weeks and according to most of fintwit I would qualify as a “bagholder” now), as did, miraculously, oil (of which I am, of course, a bagholder).

All in all, it was a good 6 weeks for the portfolio. If I were to have a complaint it was that I continue to make too many mistakes and piss away dollars on stupid purchases, which have eaten into what should have been a better period of performance.

I’m going to use this update to talk about one of those losers that I own, Mynd Analytics, now Emmaus Pharmaceuticals, and one idea that I have been in and out of – the swine flu trade.

Emmaus Pharmaceuticals

This has been a bit of a bust, to say the least. The merger between Emmaus Pharmaceuticals and Mynd Analytics was completed in July. Though it was first announced in January, it seems as though both of these companies were completely unprepared for it.

I say that because as things stand now the old Mynd tele-psychiatry business remains unlisted and Emmaus is trading, but they received a ruling of delisting from the Nasdaq on Tuesday, which I doubt was part of the plan.

The stock price of Emmaus has been on a rollercoaster since taking over the Mynd listing and changing the symbol to EMMA. It started out trading as high as $11. In all honestly, I knew that was crazy high. But I was lulled into holding on the speculation that the stock might pop really high due to lack of float and lack of sellers. There’s some saying about pigs that applies here…

As a consequence I blew the chance to sell out my shares at a nice price – it would have meant a 15% gain on my Mynd purchase and I’d still have the free-bees of the standalone Mynd Analytics once (if?) it began trading gain.

Instead I watch Emmaus fall precipitously, all the way down to $2.50, where it was back to yesterday.

I wasn’t compelled to buy down there the first time, but I did this time, adding to my position on Tuesday. It remains quite a small position and this is a very speculative stock.

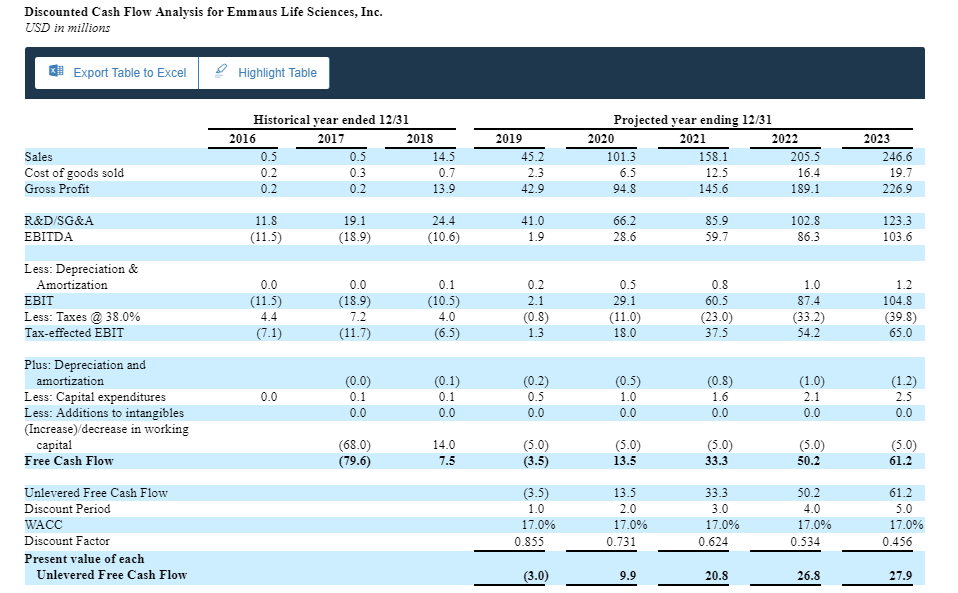

So why double down? Remembering back to my thesis on Mynd/Emmaus, the premise was that the growth from Endari, a sickle cell immunity drug that Emmaus is launching, could more than justify the share price of Mynd at the time.

Indeed, the SEC disclosures from Emmaus have put out some pretty stellar looking forecasts that back up the potential if this thesis plays out.

Clearly if Endari hits these sorts of numbers over the next few years, the stock is going to be worth more than what it is currently trading for.

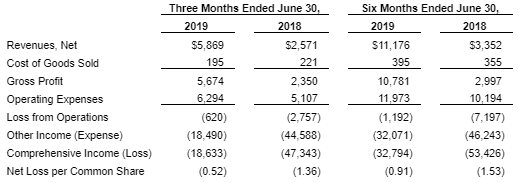

So far Endari has seen moderate results. I had hoped for more. Sales in the second quarter were only $500,000 higher than the first quarter, so 11% sequential growth.

The company forecast is predicting $45 million of revenue for 2019. I’m not sure that they can get there given the results through the first half.

But having said that, there are some positives. For one, Emmaus is getting close to cash flow neutral. The first half showed a moderate $2 million cash burn. There aren’t many pharmaceuticals in the middle of a launch that are that close to break-even.

Also, the company has $15 million of cash on the balance sheet. On top of that there is another $37 million in Telcon stock, a Korean company that is a supplier of L-glucosamine for Endari (this stock is pledged right now to the supplier but I think that is a technicality as long as Endari is a success)

At the current price of $3 the stock has a market capitalization of under $150 million, which mean a little less than $100 million for the Endari business.

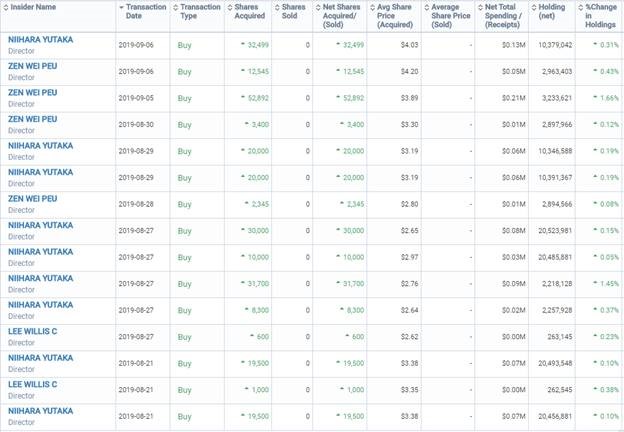

Second, when Emmaus stock collapsed the insiders really stepped up with their purchases. In fact there were shares bought the day before the delisting notice. There was another 20,000 share purchase yesterday that is not in the table. Oops!

At the very least, no one can say insiders are using the public listing as a way of unloading their shares.

The other part of the deal, the old Mynd Analytics tele-psychiatry business, is not trading yet. It has a symbol (PSYC) and the last quarter of financials show a bit of progress with revenue but still nothing to write home about. That business is what it is.

Anyway, I kinda like Emmaus. I get that Endari is nothing really that special, it is a medical grade version of an over-the-counter product. And doctors could decide to go with the cheaper, albeit less regulated and less convenient OTC option if they wanted. But I think this price is reasonable and I don’t believe the insiders are throwing good money after bad.

Swine Flu Trade

I stepped back into the swine flu trade by buying back BRF SA and adding a new position in Seaboard. Both of these positions are relatively small and to be honest I don’t know how long I will hold them.

At 30,000 feet the swine flu trade makes a lot of sense. The news from China just keeps getting worse. The disease has spread to Vietnam, Mongolia, Cambodia, Laos and North Korea. It was just reported in the Philippines a few days ago.

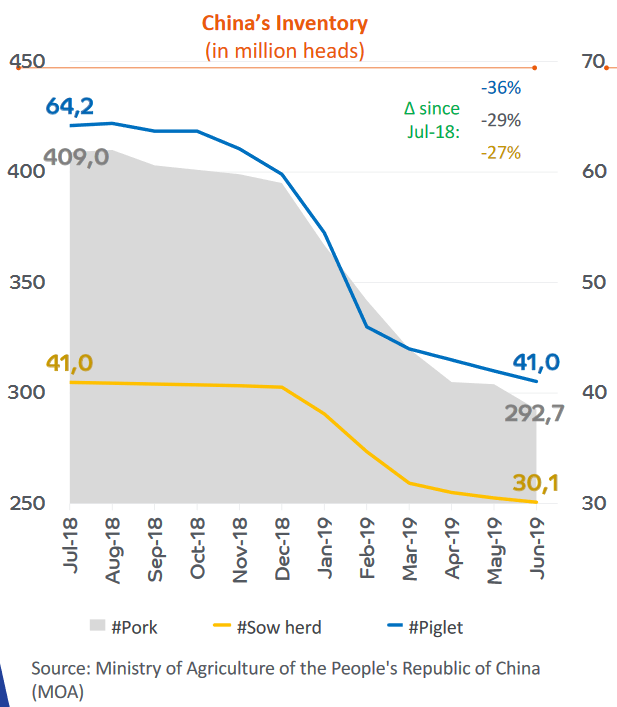

To recap, swine flu causes death to hogs within 10 days. It is highly contagious can be found in food and water. It has spread to every province in China, and they have slaughtered 35% of their hogs.

Those numbers may even be higher. As the NY Times points out:

Farmers and industry observers in China say that large numbers of African swine fever cases have gone unreported to the authorities, and that many infected pigs end up sold into the market as a result.

In a funny way, the disease kept a lid on pork prices until fairly recently. Because so many pigs were being infected, farmers in China were culling their herds early (and likely killing known diseased pigs that they could sneak into the supply before it became apparent). This surge in slaughter, as well as just the loss of pigs to the disease, led to a dramatic drop in Chinese inventory.

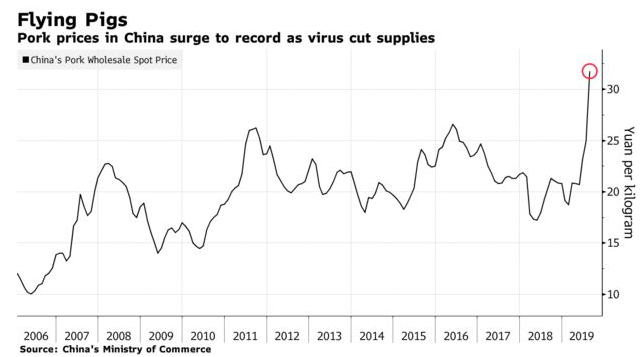

But prices could only be held down so long. In the last few months we are seeing skyrocketing pork prices in China.

The price of pork has been rising for months, and it is now nearly 50 percent higher than it was a year ago, data published on Tuesday showed.

With such a large drop in Chinese supply, China’s imports of pork, beef and chicken are rising.

These extra imports of pork should be beneficial to BRF SA, which is a Brazilian pork producer.

Consider this article, which is titled: “Will pork imports from Denmark and Brazil save China’s bacon after African swine fever hits supplies?”.

On Monday [September 10th], China added 25 Brazilian meat plants to its list of approved exporters, bringing the total to 89, according to Brazil’s Ministry of Agriculture.

Citi had a positive take on these additional export license grants:

BRF SA reported decent results in the second quarter. Revenue was up 7% to $2.13 billion. Gross margins were up 4.5% sequentially to 25%. Adjusted EBITDA was $317 million versus $104 million a year ago and $195 million in the first quarter.

With all this in mind, BRF SA is not a perfect vehicle for this trade. The company seems to perennially disappoint, it does have a lot of debt and so far in the first half of the year the company hasn’t done a very good job of converting EBITDA into cash.

BRF SA is fairly highly leveraged with Debt/EBITDA of 3.7x. What’s more the leverage is expensive, with an average interest rate of over 10%.

The second half should see better EBITDA than the first half as exports rise along with prices. Average estimates are for $1.04 billion of EBITDA. This would value BRF SA at a little over 10x EBITDA. That’s probably a fair valuation.

My hope here is that swine flu gives us another bottom-line boost in the second half that is not yet priced into the stock.

With that in mind I decided to take a second position in the swine fever trade with the purchase of Seaboard.

Seaboard is not the perfect vehicle either, but at least it diversifies my single company exposure a little. It should benefit from their pig business (about 9 million hogs) and their turkey business (they own 50% of butterball). The downside of Seaboard is that they own a bunch of other non-hog related businesses, many of which are in questionable countries (like Argentina) and they don’t really have a great record of generating cash.

Retailers Running

I took back a position in Big 5 Sports this week. I owned the stock a couple months ago (it was a stock in my last update) along with Dean Foods. I was waffling on the retailers at the time, even having looked at Francesca Holding which I held for all of one day. But I had no conviction in the idea and sold them all.

With the rotation we are seeing out of tech and into pretty much anything else that has been weak, retail plays like these are starting to make big moves.

Of course, I bought back Big 5 Sports so Dean Foods, not to mention Francesca, have went on a tear. Oh well. I like Big 5’s chances better in the long run.

Not that those chances are all that stellar. This is a beleaguered retailer without a doubt. Big 5 has a market capitalization of $50 million and even including debt the enterprise value is only $114 million.

For that price you are getting 433 store locations with an average size of 11,000 sq. ft.

Of course, you are also getting stagnant sales and precipitously falling EBITDA. Last year Big 5 did $20 million of EBITDA. The year before that they did $41 million. The year before that they did $50 million. Notice the trend…

There are plenty of negative articles on Big 5 on SeekingAlpha. This Detroit Bear guy does a good job of explaining the bear thesis, which is not without merit.

Yet the last quarter was not terrible. And when you have a $2 price tag on a stock that used to be well into the double digits, not terrible is not all that bad.

The company increased revenue marginally, dropped operating expense by a percentage and generated an extra million of cash flow before working capital. It’s moving in the right direction.

I have no grand plan thesis here. It’s simply that with the rotation going on, moving in the right direction might be enough.

After all, look at FRAN.

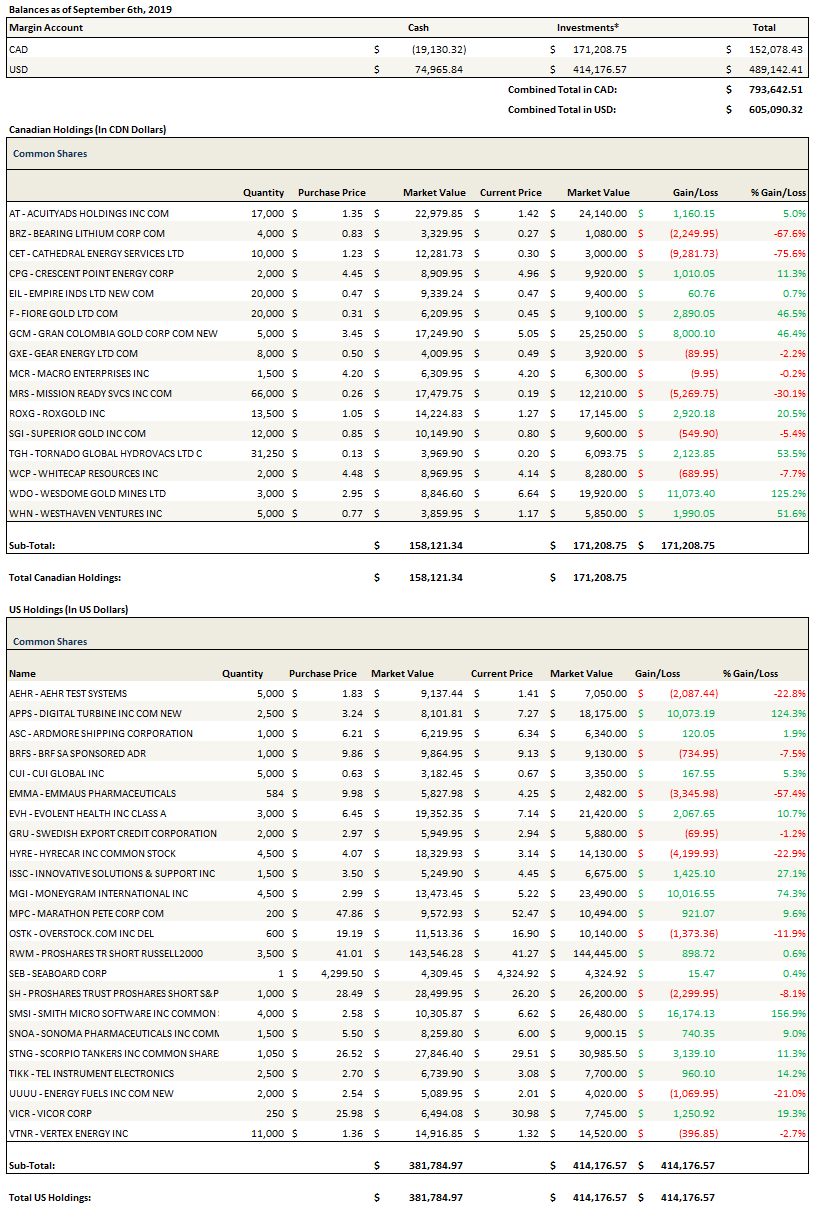

Portfolio Composition

Click here for the last six weeks of trades. Note that when I did this update I realized I hadn’t bought Nuvectra or sold Marathon Petroleum in the tracking portfolio. I have made both moves this week but they are not reflected below.

{kind=link}

New cost basis for EMMA?

I just transferred over my old cost basis from mynd to emma, i guess that i should be allocating something to the new mynd once it actually trades but i’ll deal with that when it happens

Bed Bath & Beyond Inc. (BBBY) could also be interesting…

https://seekingalpha.com/article/4289831-bed-bath-and-beyond-top-5-pick-activists-rescue

thanks