Nuvectra

I am going to start this post with all the reasons I can think of to not buy Nuvectra.

That list has to start with the chart. This was a $20 stock less than 12 months ago. Now its barely $2 and only a few weeks ago it flirted with $1.

The collapse of the stock coincided with the resignation of most of the C-suite that had run the company since going public. The CEO Scott Dree resigned in January. This was followed up by the departure of the COO/CFO in May.

The collapse has also coincided with the demise of the Nuvectra growth story. Prior guidance of $57 – $62 million was reduced to $50 – $55 million in August.

In the second quarter year-over-year revenue growth fell to 7%. This is way down from 80% growth average in 2018 at odds with the increasing salesforce that the company has put in place.

In fact, Nuvectra has long said that they believe their salespeople can generate $1 million to $1.5 million of sales. The current 60 person sales team should be able to achieve $60 million to $90 million of revenue. Yet the company recently reduced guidance to a range of $50 million to $55 million.

Even more disturbing, Nuvectra is having trouble keeping their salesforce. On the last couple of calls they have mentioned sales attrition as a factor limiting growth a number of times.

The sales attrition could be due to the fact that the salespeople aren’t selling. On the last quarterly call new CEO Frank Parks admitted that in some cases as much as 75% of the salespersons time is spent non-selling.

One flaw in the product that has come to the attention of management is the charging process.

In part, selling (inaudible) have been impeded by some reports of patient frustration with the Algovita charging process.

Our core technology continues to function as designed and labeled, repeating, our core technology continues to function as designed and labeled, but we believe the ergonomics of the charging process sometimes creates frustration amongst patients.

The slowdown is not just a company specific hiccup. The industry that Nuvectra is in (sacral nerve stimulation or SCS) appears to be slowing as a whole. Competitor Nevro has seen revenue decline over the first 6 months of the year. Boston Scientific said this on their second quarter call:

In SCS, we continue to see some softness in the overall market, and we face tough comps as mentioned due to our WaveWriter spinal cord stim system launch in the U.S. early last year. While we continue to be optimistic about the long-term 7% to 10% growth potential of this market, we do expect some continued softness in 2019 given the 21% second half comp.

What makes the growth situation more dire is that the company is burning cash. Nuvectra has burned on average $11 million of cash per quarter for the last 6 quarters. There is very little in the trend to suggest it is coming down. Cash levels sit at $69 million at the end of the second quarter.

Last week the company announced that they would be “implementing a force reduction plan” that will “result in the termination of approximately 20% to 25% of the Company’s employees during the third quarter of 2019”.

While the cuts will reduce cash burn by $5.8 million in 2020, they aren’t going to do much for guidance or employee moral.

Finally, Nuvectra’s second product, the Virtis system, which is a neuromodulation system intended to address the sacral nerve stimulation (SNS) market, has been held up by FDA requests. The FDA has asked for additional supplementary data on Virtis leads with chemical composition and biocompatibility studies. This has pushed out Virtis approval until mid-2020.

So there you have it. Cash burn, slowing growth, terrible chart.

Yet as far as I can tell, Nuvectra has a real product. Their Algovita system, which is approved for SCS by the FDA, is a legitimate alternative to competitive products from Nevro, Boston Scientific and Medtronics.

The competition trades at a significant premium to Nuvectra. Nevro, which is the only pure play competitor, trades at nearly 7x 2019 sales and that is on declining revenue. Boston Scientific and Medtronic, which are much larger multi-product companies with competitive SCS offerings, trade at 6.2x and 5.1x revenue respectively. Nuvectra trades at under 1x revenue based on their market cap and well under 1x if you include their net cash position.

The slip in Algovita sales is fairly recent. Up until the last quarter sales of Algovita had been growing at a rapid clip with expected 2019 growth of 29%.

The product has been available for 3 years now. It would seem to me that if it was truly not competitive, we would have seen an indication before this.

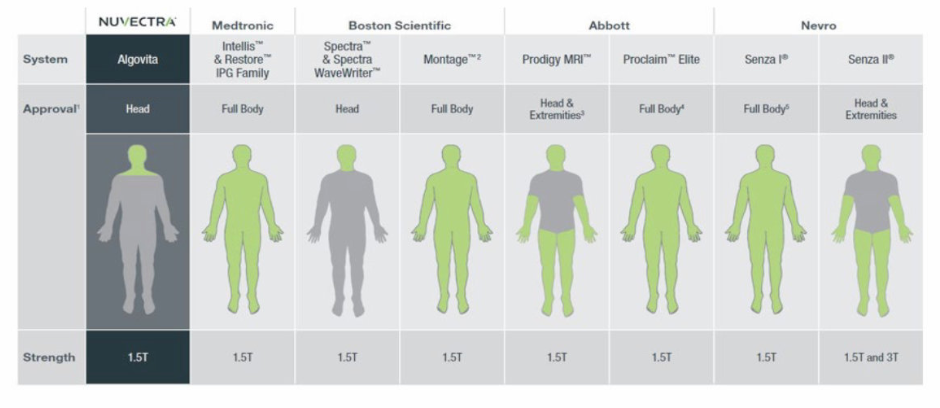

Algovita has a small slice of the SCS market. This is in part because of its relatively recent release. It is also in part because the product only has approval for head-only MR. This limits the market compared to the competition.

The company has completed regulatory submission for full-body MR which will strengthen the products competitive position. The approval, which is expected to come in the fourth quarter, would be a catalyst for the stock.

At the same time that Dree resigned the company named Chris Chavez to the board of directors. From everything I have read Chavez has a very strong background, is a pioneer in the neuromodulation industry and that he would put his reputation on the line again with Nuvectra is a vote of confidence for the company.

He served as President, Chief Executive Officer and Chairman of TriVascular Technologies, Inc. from April 2012 through its merger with Endologix, Inc. in February 2016. Following the merger, he served as an Endologix Director from February 2016 through June 2018. Mr. Chavez also served as President of the Neuromodulation Division (NMD) of St. Jude Medical Inc. from 2005 through 2011 following the acquisition of Advanced Neuromodulation Systems Inc. by St. Jude Medical in 2005. Prior, he served as CEO, President and Director of ANSI from 1998 through 2005 and led ANSI/NMD through 14 years of profitable growth and innovation. In 1997, Mr. Chavez served as Vice President, Worldwide Marketing & Strategic Planning for the Health Imaging Division of the Eastman Kodak Company.

Finally, Nuvectra has formally announced a strategic review.

The combination of a management team overhaul, an interim CEO, the addition of Chavez as a board member and the reduction in staff all suggest to me that the company is on the block and ready for sale.

It seems to me that in a sale the combination of cash, Agovita revenue and growth and Virtis potential should be worth more than $12 million.

Anyway, that is my contrarian thesis in the face of an admittedly long list of negatives.

To be honest from my point of view, your approach is excelent, and altough I am not really familiarized with the business, I see a good potential here in terms of future growth, change of dynamics and a catalyst on the full body approval. However my question would be exactly about this last topic. Do you know what would be the “barriers” that could block a possible full body approval? What kind of “insecurities” lies on this barriers?

Thank you for always sharing your views and your analysis! really appreciate them

No I don’t know the probability of that going through or not, sorry.