Clear as Mud

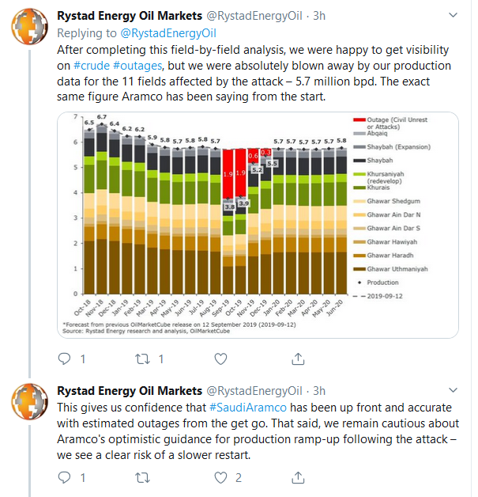

We are one week past the attack on Abqaiq and Khurais and there is still a lot of uncertainty (or disinformation) about what is really going on there. Take for example these two news stories.

The first is the from the Wall Street Journal, posted last night.

Many Aramco executives and board members, meanwhile, are privately expressing doubt that the company can meet its target of a three-week return. They estimate the production recovery will take twice as much time, according to people in touch with them.

Some “board members are horrified” that the company could communicate such optimistic assessments, said one of the people.

The second was posted this morning on Reuters.

Saudi Arabia has restored around 75% of crude output lost after attacks on its facilities and return to full volumes by early next week

I have been pondering all morning how both of these stories, from reputable news outlets, can be true.

The attack took offline 5 million bbl/d of throughput. According to the Reuters article, Aramco is already back to 4.3 mmbbl/d. So it is basically a non-issue.

But if that is the case then where is the WSJ getting their information from? Who are the board member and executives that are “expressing doubts”. How can they be expressing doubts about a situation that has already rectified itself.

Some are suggesting that the stories are talking about different things – that Reuters is talking about production and the WSJ is talking about capacity. But that is not what I read – the doubts being expressed are about the return of production.

I’m not the only one that is skeptical about the Saudi optimism.

My Way to Play it – Canadian Oil

Fortunately, I can hold the Canadian oil stocks I bought without having to worry too much about where the truth lies because they haven’t really been bid up very much any way. What’s more, most of them are starting to benefit from big stock buyback programs (Gear Energy just announced a 5% program today) and there are other non-Saudi positives that should play to their benefit as well.

What are those positives? We know that Alberta pipeline adds (optimization from Enbridge and TC) are 185,000 bbl per day in the fourth quarter. We also know that the Sturgeon refinery is likely to switch to bitumen feed-stock shortly. We also know that Jason Kenny said last week that he would lift the curtailment if you can ship your oil by rail.

Meanwhile heavy oil seems to be supported by the attacks in Saudi Arabia. I have to admit I don’t really get this part – it seems that it is light oil that the Saudi’s are hinting they might have trouble delivering, yet when you look at spreads it seems like heavy oil has been more of a beneficiary.

As I mentioned last week I made a bet on PBF Energy with the thesis that the pop in high sulphur fuel oil (HSFO) wouldn’t last. That has somewhat played out – HSFO did drop off its highs and the December contract is back to $36/bbl – it was $33/bbl before the attack. PBF Energy recovered as I expected. I unfortunately sold out a day too early, on Friday, while the stock has continued to pop today.

But I am still not sure where all this is going. Is there going to be less HSFO because the Saudi’s will use it to run their power plants (this is not good for the environment by the way) so they can ship more low-sulphur oil to their customers? Or will the Saudi’s ship high-sulphur crude abroad to refiners like PBF and they will make a killing on the collapsing differentials? It’s not at all clear.

Overstock – I Swear I’m Out for Good This Time

Another bit of news today is Overstock, which has become even more of a gong-show than even I thought possible. The CFO resigned and the company reduced guidance (which they had only just raised in July!).

I sold out of what remained of my position as fast as I could this morning. When a CFO leaves, particularly in the middle of tumult (as has been the case with Overstock), it is better to stand aside. I made some money on the way up, and gave some of that back on the way down. I do think this will be the last trip I have with the stock.

Mission Ready Conference Call

Last Thursday Mission Ready had a conference call with investors. I thought it was pretty positive. The company outlined the business in more detail than they have done before.

I learned that gross margins are in the 12% area right now and they’d like to see them up to 15%, but that they can’t go much higher without raising eyebrows at the Department of Defense.

I learned that the major impediment to growth right now is the small team and that they have plans to grow their sales staff significantly.

I learned the foreign military deal is indeed dead but that there are others they are in contract with.

Most importantly, I also learned that we should expect more extensions on the TLS contract rather than a new 10-year contract being awarded. As I wrote in this post, the TLS contract has 6 prime-vendors, with Mission Ready subsidiary Unifire being one of them. The largest of these 6 vendors is a company called ADS. ADS has volumes in the billions of dollars.

ADS is in trouble because they were stripped of their small-business designation and they had to pay a settlement associated with having fraudulently obtained some of the small-business set-asides from these contracts. This article from the Washington Post describes the situation.

The upshot of this is that ADS may get removed from the vendor list of the next TLS contract. What I learned from the call was that if they did, ADS would almost certainly protest the decision. If, on the other hand, they didn’t get removed, all the other vendors would protest.

The mess that this would entail makes it very likely that there will just be 6 month to 1 year extensions made to the existing contract.

This isn’t a bad thing for Mission Ready, as extensions mean there is no review of vendors, it gives them time to ramp Unifire as a vendor and prove themselves. If Mission Ready can continue to take contract wins at the rate they have over the last 6 months or so, I think the company is setting itself up quite well.

After the conference call Mission Ready announced another $15 million in wins the next day. They are up to $75 million to date.

Nuvectra Bonus

On Friday night Nuvectra filed their employment agreement with their new CFO, Jennifer Kosharek, As part of that employment agreement the filing stated that Ms. Kosharek and other executives are in line for a “transaction bonus”:

Transaction Bonus Plan

As previously disclosed, the Company is exploring potential strategic alternatives to enhance shareholder value and recently implemented a reduction in force. To incentivize and reward employees for their increased responsibilities in light of these events, on September 16, 2019, the Company’s Board of Directors, upon the recommendation of its Compensation Committee, approved a cash incentive plan to reward a broad base of employees in connection with a potential sale of the Company (the “Transaction Bonus Plan”). Under the Transaction Bonus Plan, cash payments would be made to eligible employees (1) 50% upon the signing of a definitive agreement for the sale of the Company and (2) provided that the definitive agreement remains in effect, 50% upon the earlier to occur of March 31, 2020 and the closing of the transaction. Participants must be employed by the Company at the time of payment. The total cost of the Transaction Bonus Plan, if fully implemented, will not exceed $1.6 million.

In general, executives do not decide institute a big incentive to be paid out in the case of a transaction unless they feel that transaction may occur.

Emmaus – Blah

I also sold most of my Emmaus on Friday (I should have sold it all, its down again today!). The stock is acting so bad and the company didn’t get approval of their appeal at the EU (they announced this Thursday). I can’t figure out why insiders were buying so much given that since they have bought there has been nothing but negative news. and am left to conclude that maybe they were just wrong. I have been too, and what is left of my position is pretty insignificant so I might just sell it and admit defeat on this one.

A Couple of General Comments

Overall I remain even more cautious than last week. In addition to my skepticism that oil prices will remain so sanguine, it occurs to me that if oil prices do continue to do nothing, it could be because the world economy continues to sputter. There seems to be more and more evidence that the global slowdown is getting worse, not better.

We are also entering a time where liquidity is unusually tight. We had the odd spike in repo rates last week that the stock market does not seem to care about but which nevertheless is just a little disconcerting. We are also in a period where a lot of US dollars are leaving the system all at the same time. This kind of liquidity squeeze is usually not good for the speculative sort of stocks that I like to hold.

This morning I received from a friend a PDF of the latest Macro Insights piece from the founders of Real Vision. In it they pointed out:

When you consider that with quantitative easing the Federal Reserve balance rose about $3 trillion over 6 years, it just seems like this one-time treasury issuance, which has the effect of the opposite, is not insignificant.

When you consider that with quantitative easing the Federal Reserve balance rose about $3 trillion over 6 years, it just seems like this one-time treasury issuance, which has the effect of the opposite, is not insignificant.

When you couple that with what seems to be real funding stress in the repo market, well, you just have to wonder where we are going.

Look, I don’t know this stuff inside out. I invest my money and write a little blog saying why I do what I do. This could be a whole lot of nothing. Probably is. But for me, I’m going to be even more cautious than usual. With that in mind I sold Scorpio Tankers (for now), sold Ardmore Shipping (for now), sold the rest of Moneygram and bought some more inverse ETF shares on the S&P.

Last point: Elizabeth Warren appears to be gaining momentum in the polls. I do not necessarily disagree with much of what Elizabeth Warren says, but I am pretty sure that if she gets elected and does what she says she is going to do, it is not going to be good for the stock market. The market obviously doesn’t care about this yet but at some point, if her strength continues, it will.